“The Dollar is money, money is value, value is trust, trust is a contract – and the contract is debt.”

-Jim Rickards

Who do you trust? Government monetary policy makers, markets – both? Or neither?

Have you been of the view that the money that was printed was going to create a “velocity” of money or behavioral distrust? If the short-term policy was to create the illusion of growth (inflation expectations), isn’t the long-term risk a #Deflation of those expectations?

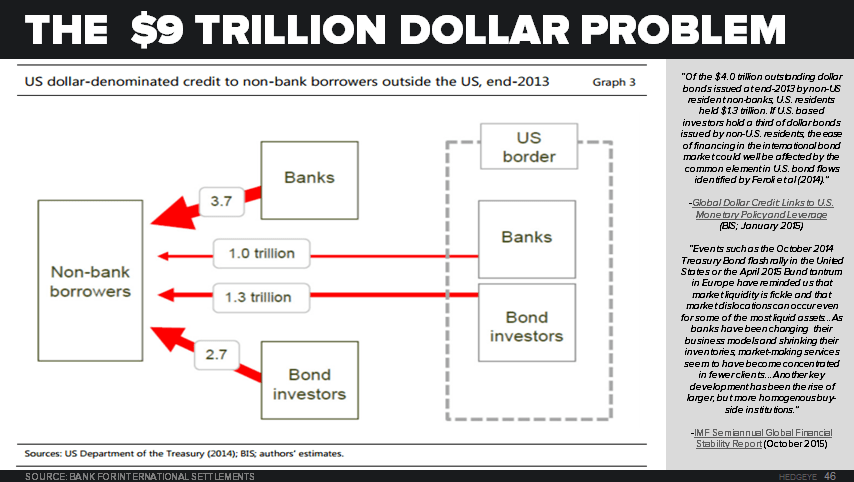

How about the $9 Trillion Dollar Problem (see Chart of The Day) that is US Dollar-denominated credit to non-bank borrowers outside of the US? That’s a massive contract. Does it have risks? As the economic cycle slows, in debt linked to inflation expectations do you trust?

Back to the Global Macro Grind…

The aforementioned quote comes from the original author of Currency Wars, Jim Rickards. I’m honored that he’ll be kicking things off at Macrocosm this afternoon in Stamford, CT alongside Jurrien Timmer, Director of Global Macro and Investment Research at Fidelity.

I think you’d guess that I don’t trust governments – certainly not on monetary policy matters. The idea that an un-elected human being whose economic forecasts are wrong 70% of the time can smooth and bend economic gravity is a little too much for me.

Not everyone at our inaugural macro conference is as bearish on the Central Planning of markets as I am, but that’s what makes a market. And I’m really looking forward to this afternoon’s Dock Debates – Macrocosm 2015.

On the heels of China’s Premier Li reminding the world that the Chinese economy has “relatively large downward pressure” overnight:

- Centrally planned Chinese stocks in Shanghai fell -1.0%

- The Hang Seng in Hong Kong dropped another -0.3%, taking its decline in the last month to -3.8%

- Emerging Asian Equities (Thailand down another -1.1%) resumed their bearish TREND @Hedgeye

This all came after another ugly session for those long “reflation” and “green shoots”:

- CRB Commodities Index dropped another -0.9% yesterday making lower-lows vs. its AUG crash lows (-20% YTD)

- Copper remained no bid, all-day yesterday, taking its lower-lows beyond the summer-time lows to $2.09/lb

- Both Oil (WTIC) -1.5% and Oil & Gas Equities (XOP) -1.9% led losers in yesterday’s Global Macro trading session

Combined with the reluctant confirmation of demand slowing from the Chinese, these appear to be red shoots to me.

US stocks tried to have their 2nd up day in a row and closed down for the 8th day in the last 10, instead:

- Big Cap Energy Stocks (XLE) showed no follow-through from the day prior, closing -1.1% at -14.8% YTD

- Financials (XLF), which are supposed to go up on a “rate” hike, dropped to -2.3% YTD

- Small Caps (Russell 2000) underperformed the SP500 (again), moving back to -4.4% YTD

Yep. Ex-Energy, Small Cap Domestic Growth, Financials, and most of US Retail (XRT -10.7% YTD), everything is fine YTD.

For those of you who have real-time quotes and an account with real-money in it, you’ll note that an -11% draw-down in the Russell 2000 (and/or US Retailers YTD) from its all-time #Bubble high in July is a problem. (hint: you need to be up +12.4%, from here, to break-even)

And it’s an even bigger credibility problem that the people who are still looking for 3-4% GDP and +8-10% “Earnings Growth” in 2015 are seeing Q3 Earnings Season wind down with the following reality:

- 468 of 500 S&P 500 companies have reported

- Aggregate Q3 Sales Growth is down -4.3% year-over-year

- Aggregate Q3 EPS Growth is down -4.6% year-over-year

I know. I know. If I back out Energy, Industrials, Retailers, etc. I still see the Financials with a -7.6% year-over-year earnings recession for Q3, so we should definitely raise rates so that Jaime Dimon can fix his NIM (net interest margin) pressure and get back to paying bonuses.

With Industrial Production Growth (IP) for October slowing to its lowest rate of change of the year at 0.3%, as the US industrial/cyclical economy enters a recession, what Dimon really needs to do is ignore that and cheer-lead some non-data-dependence @FederalReserve.

With all this politicization, it’s no wonder why Janet is having a fit about this proposed “FORM Act” (Fed Oversight Modernization Reform Act) suggesting to Congress that it would “undermine the Fed’s ability to implement policies that are in the best interest of Americans”…

On the other hand, US Presidential candidate Marco Rubio says he wants Janet Yellen out of her un-elected seat because the “Fed often times ends up making policies that dramatically alter the economy in very negative ways”…

This is still America where the Dollar is the hard-earned money of The People. The Dollar is our money, not theirs. Trust in USD policy isn’t allocated to Mr. Bernanke or Mrs. Yellen - it’s earned. Transparency and accountability is trust – and the contract is free-market liberty.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.17-2.30%

SPX 2016-2068

RUT 1134--1172

VIX 16.77-20.98

USD 98.20-100.13

Copper 2.07-2.18

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer