In what we view to be one of the most ridiculous “strategic” moves by a retailer in over 20 years, Urban Outfitters (URBN) has announced the acquisition of the Vetri Family group, which owns a handful of Italian food restaurants. The deal was justifiably lampooned in the media as an odd departure for a retailer, known primarily for pandering to the young, hipster crowd.

After looking at Urban Outfitters’ horrible third quarter earnings, the rationale became a bit clearer. Management is at the end of its rope and looking for ways to improve its core (slowing) business.

Investors aren’t pleased.

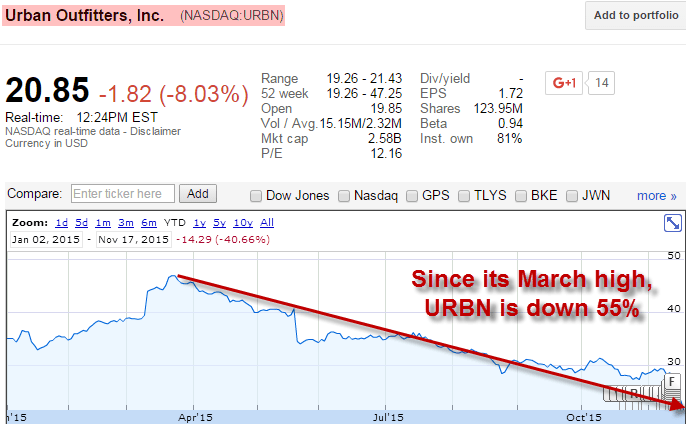

Urban Outfitters’ stock is getting crushed this week, falling 20%. It’s clear to us, if Urban is looking for a panacea to unlock future growth, this clearly isn’t it.

Here’s why.

This is an extremely small deal. Vetri owns just nine Italian food restaurants located primarily in southern Philadelphia. That could help explain why Wall Street analysts didn’t even question the deal. Of the twenty-six questions asked during the third quarter earnings call, not one of the 11 participating analysts asked about the Vetri transaction.

That’s troubling, though, given the significant slowdown in Urban’s business. The company has now missed sales expectations for the third quarter in a row. So, with the Vetri acquisition, Urban is obviously stretching for growth opportunities.

The slowdown in shopper traffic has hurt other retailers too. In the past week, Macy’s (M), Kohl’s (KSS) and Nordstrom (JMN) all saw their stocks slide between 4% and 24% on lackluster retail sales data. It’s perhaps the clearest indication yet of a #LateCycle slowdown in consumer spending.

That said, Urban Outfitters has fallen harder. And faster. The stock is down 55% from its March high. Make no mistake. Even with the drawdown, the stock still isn’t a bargain and we still have lots of questions.

What's the real addressable market for each concept? How has the competitive landscape changed? And how much capital is needed to capture that growth? All in, there's no reason to think that those high-teens EBIT margins of old are 'owed' to URBN.

This might be the new normal. At least, that's what we're going with until our research changes.

But let’s parse the new Vetri “opportunity” a bit. Yes, Urban Outfitters’ target demographic might be a 25-year old consumer. Yes, 25-year old consumers might like pizza. But that doesn’t mean that URBN has earned the right to get into the pizza business.

Consider the pure logistical aspect of pivoting from owning pure retail stores to some retail-restaurant hybrid. We’re talking about a completely different level of operating scrutiny in the restaurant business, with food preparation, employee training, and FDA oversight. For starters, Urban Outfitters currently doesn’t have to monitor whether or not its employees wash their hands after leaving the restroom. Simply put, this is a fundamentally different model than anything URBN operates today.

There’s also a problem with searching for growth in an industry that is clearly declining. On the third quarter conference call, we found this comment from Urban Outfitters CEO Richard Hayne particularly odd:

“Spending on casual dining is expanding rapidly, and thus, we believe there is tremendous opportunity to expand the Pizzeria Vetri concept.”

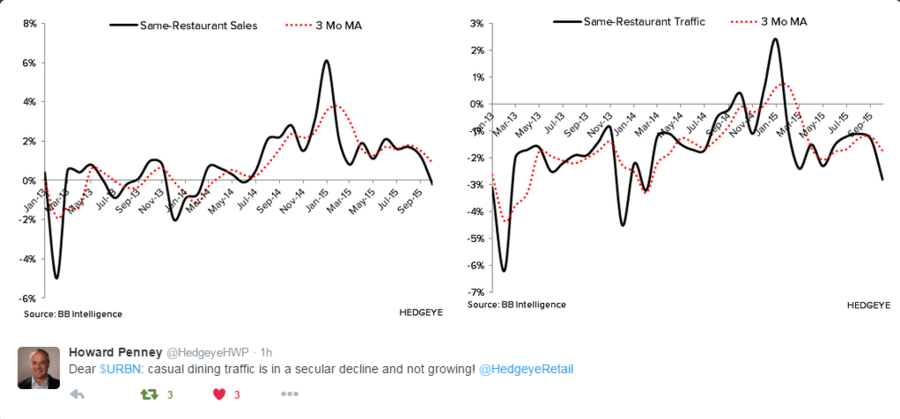

As our Restaurants analyst Howard Penney pointed out, following the Vetri acquisition news, casual dining traffic and sales are “in a secular decline and not growing.”

click the image below to enlarge.

Are we making a mountain out of a molehill? We don’t think so. The mountain is already there, and it’s causing what has been a very well-managed company to look far outside its core.