On November 10, 2013, I wrote a note on McDonald's called “McDonald's Obsession with Starbucks” My bearish thesis on MCD revolved around my “espresso-based conspiracy theory.” As hard as McDonald's management tried, MCD will never be what Starbucks is: a leading destination for espresso-based beverages. In the process of trying to be SBUX, MCD was hurting the core business of selling food!

Fast forward to today and MCD is now focusing on the core business of selling food again. What interested me the most about the McDonald’s analyst day was not what was said, but what was left unsaid. The biggest operational change appears to be a gradual shift away from beverages. The word McCafe was never mentioned by, Steve Easterbrook, President, Chief Executive Officer & Director, McDonald's Corp., Pete Bensen, Chief Administrative Officer, McDonald's Corp., or Mike Andres President, McDonald's USA, McDonald's.

The first mention of McCafe came from Kevin Ozan, Chief Financial Officer & Executive Vice President, McDonald’s Corp: “We seek to balance new store investment, where we have historically earned higher rates of return, with investments in existing restaurants that has included reimaging, initiatives such as the expansion of our beverage business and McCafe, and general maintenance CapEx.”

At the 2013, analyst meeting “McCafe” or “coffee” was mentioned 92 times! Do you think there has been a shift in strategy? I place significant weight on this because I have contended since 2012 that McDonald’s, shift to over emphasizing beverages was a key contributor to poor instore execution and the biggest contributor to significantly slower drive-thru times.

Correcting the mistakes of the past will be the biggest contributor to fixing the performance inside the four walls and improving same-store sales. When I pressed this question to senior management the response I received was “Mike (Andres) is a food guy”

These comments from Mike’s presentation say it best, “We are a restaurant company. We must and will win with our food. Our customers tell us that they want our food to taste great and they want to feel good about eating it. They want to know what's in their food. Where it comes from and how it's made. While we are very proud of the quality of the food that we serve today, we know we can do better. We have a committed attitude around real and fresh, specifically around the ingredients and the evolution of the menu.”

The rollout of McCafe was the most expensive project the company has ever undertaken! The McCafe brand has some goodwill with customers, but the company will never be successful selling espresso based drinks. Therefore the unwinding of the McCafe strategy is a slow process that will happen quietly.

It looks like MCD has set reasonable goals for 2016. The company is looking for constant currency financial targets of system-wide sales growth of 3% to 5%, (adjusted) operating income growth of 5% to 7%, and one year return on incremental invested capital in the high-teens. When the company announces its longer-term targets in 2Q16, I suspect it will be close to the 2016 targets.

OTHER IMPORTANT TAKEAWAYS

G&A SAVINGS

As expected MCD is now reducing G&A by $500 billion compared to the $300 million target announced in May the vast majority of which they expect to realize by the end of 2017. Expectations going forward are for system sales to grow faster than G&A. The incremental savings are primarily derived from savings coming from a more heavily franchised and less G&A intensive structure; streamlining of corporate and former Area of the World organizations and realizing greater efficiencies through the global business services platform. The G&A savings represent roughly a 20% reduction off of the G&A 2015 base of $2.6 billion.

It was interesting to note that MCD management did say, “…we analyze our G&A spend and resulting profitability on a per restaurant basis. McDonald's G&A per restaurant is currently about twice that of our QSR competitors on average. However, our profitability as measured by EBITDA per restaurant is about four times our competitor's average. Our business model, geographic diversification, franchising strategy and overall support model are some of the reasons that our restaurant averages differ from our QSR competitors. We expect to significantly reduce our G&A per restaurant as a result of our efforts.”

REFRANCHISING

Another big shift is that MCD is now aiming to refranchise 4,000 restaurants by the end of 2018, with mostly all of them to take place in the high-growth and foundational segments. The refranchising target of 4,000 restaurants by 2018 implies approximately 1,000 restaurants per year and will move MCD from 81% franchise today to about 93% franchise globally. Putting MCD well on their way to the longer term target of 95%. The refranchising strategy will help to improve MCD’s relative multiple versus its peer group.

- Accretive to the company-operated margins

- Refranchising activity will also positively impact the franchise margin

- The decline in operating income will be modest when factoring in the G&A savings

- Refranchising will be accretive to FCF due to lower capital expenditure requirements.

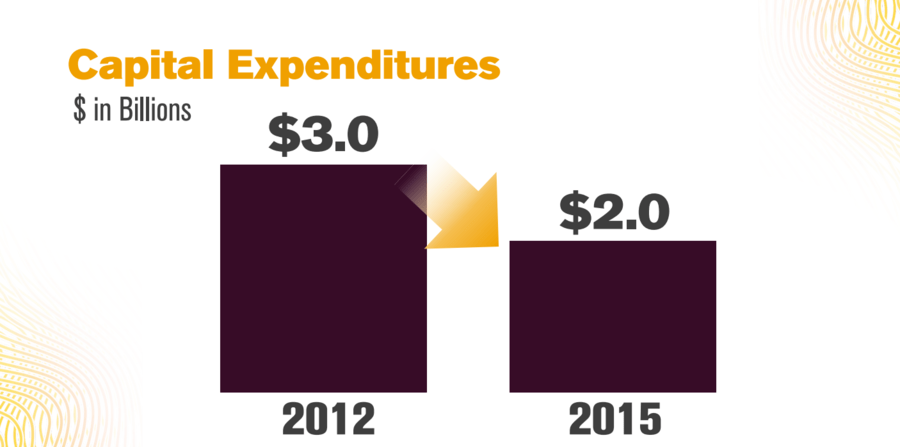

DECLINING CAPITAL SPENDING

A small part of the MCD growth story will be expanding the global footprint and reinvestment into existing restaurants. This includes the “Experience of the Future” as well as the reimaging of about half of the store base over the next several years.

Capital expenditures are expected to remain at about $2 billion, split evenly between new stores and investing in existing restaurants. As the business model evolves to a more heavily franchised structure, capital expenditures should decline over time.

CASH

MCD significantly increased the cash return target for the three year period ending in 2016 to about $30 billion. This aggressive move is further proof in the new management teams willingness to change the MCD business model and make the appropriate adjustments when needed. The $30 billion figure represents a $10 billion increase versus expectations. The company will use incremental debt to fund the vast majority of this increase. The $30 billion cash return target will be nearly double the $16.4 billion for the three-year period ending 2013.

Importantly, MCD will now manage to rating of BBB+ at S&P and Baa1 at Moody's credit ratings. Going forward (beyond 2016) , MCD intends to return all free cash flow to shareholders over the long-term through a combination of dividends and share repurchases.

MCD USA NOTES

MCD USA

- Represents approximately 30% of McDonald's global revenue and 40% of consolidated operating income

- More than 14,000 restaurants

- 90% owned and operated by more than 3,100 franchisees.

- Traditional free-standing restaurants have AUV’s of $2.5 million and cash flow of approximately $315,000.

All Day Breakfast

- All-Day Breakfast has continued to exceed managements launch volume expectations.

- We are currently seeing more than 15% of food purchases outside the breakfast daypart that include an All-Day Breakfast menu item.

- The lunch daypart is providing the largest impact to the All-Day Breakfast with promising results also during dinner.

- Rest of the day average check is higher among those purchasing an All Day Breakfast entrée.

- All Day Breakfast has helped with McDonald's brand perceptions. According to a recent YouGov survey, which indicated that MCD’s perception score stood at 17 points since the beginning of August?

- Improving the in-store execution and success of ADB many markets have removed one or more of the McWraps, Bacon Clubhouse, Quarter Pounder Deluxe and/or Snack Wraps. In addition the menu went from 16 extra value items to nine.

- In addition, In July, the company rolled out the Drive-Thru Express menu board, this move took the total price point from 130 to less than half of that which of course simplifies the customer ordering process.

Looking forward to the next 12-18 months

- Deploying indoor digital menu boards in all U.S. restaurants by fourth quarter of next year.

- Automate the ways they promote their food to consumers inside of our restaurants.

- Will install a robust content management system that will engage the customers with food show quality moving pictures, enhanced capabilities that will adjust the menu board based on time of day and product mix movement.

- Based on the results in Canada the new digital menu boards and content management system will generate higher average checks and incremental sales in in-restaurant transactions.

- Currently MCD has about 130 restaurants that are presenting the Experience of the Future in the U.S. and advertised sales tests are scheduled to go live in six markets by the end of the year.

- Roughly 25% of customer visits are motivated by value.

- Offering a consistent, predictable and compelling national value platform is a critical component to our combined solutions plan.

- The MCD digital platform is evolving.

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst