RECENT NOTES

11/12/2015 JACK | THE SHARKS ARE CIRCLING

11/05/2015 HABT | DEFYING GRAVITY

11/04/2015 DRI | ARE OLIVE GARDEN EXPECTATIONS TOO HIGH?

11/03/2015 BLMN | CAN YOU TEACH AN OLD DOG NEW TRICKS

RECENT NEWS FLOW

Thursday, November 12

YUM | Yum! Brands China division reported October same-store sales growth of 5%, comparable to the divisions 6% growth in September. October results consist of 10% growth at KFC and a 9% decline at Pizza Hut. China division same-store sales growth guidance for the fourth quarter was reiterated at 0% to 4%. (ARTICLE HERE)

JMBA | Is becoming the latest company to launch a Mobile Order app, their app will be launching in mid-November in 600 stores across the United States (ARTICLE HERE)

DPZ | Opened its first store in Belarus, the sixth new market opened in 2015 (ARTICLE HERE)

Monday, November 9

DNKN | Dunkin’ Donuts franchisee signs agreement to build 25 restaurants in Mexico (ARTICLE HERE)

SECTOR PERFORMANCE

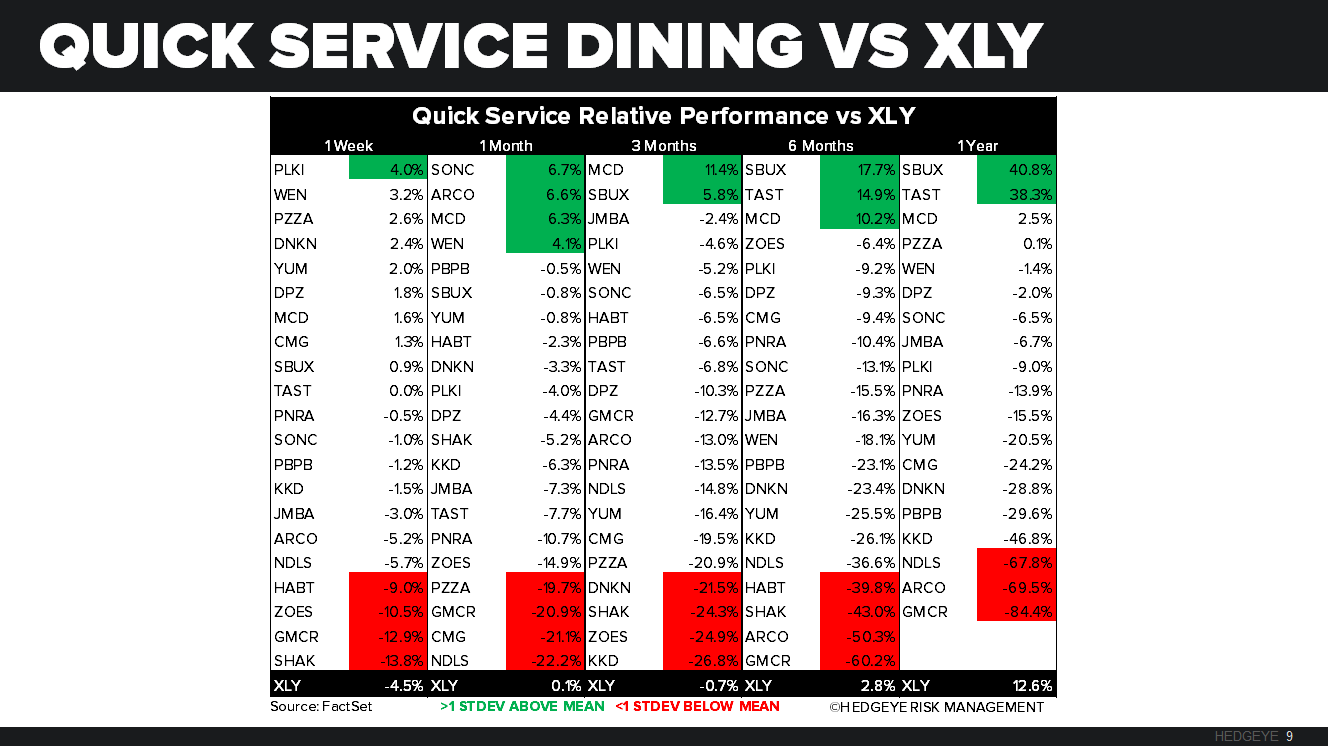

Casual Dining and Quick Service stocks that we follow had a mixed week last week, with casual dining companies outperforming the XLY, while quick service companies underperformed. The XLY was down -4.5%, top performers on a relative basis from casual dining were RT and TXRH posting increases of +6.0% and +4.9%, respectively, while PLKI and WEN led the quick service group this week up +4.0% and +3.2%, respectively.

XLY VERSUS THE MARKET

QUANTITATIVE SETUP

From a quantitative perspective, the XLY looks BEARISH in the TRADE duration but BULLISH from a TREND perspective, TREND support is 77.55.

CASUAL DINING RESTAURANTS

QUICK SERVICE RESTAURANTS

Keith’s Three Morning Bullets

Both US and European Equity Beta signaled immediate-term oversold into Friday’s close:

- EURO – down another -0.4% vs. USD at $1.07 this morning with the more important line of support being the YTD low of $1.05. While Dudley’s latest comments on “inflation continues to run well below the Fed’s target” are new/dovish this am, the FX market is obviously focused on the tragic events in France

- KOSPI – last week was ugly for everything Global Growth Expectations and KOSPI continued to break-down overnight down another -1%, taking it’s month-over-month decline from OCT’s counter TREND bounce to -4.3%

- COPPER – fresh new lows (again) this morning as Copper’s #Deflation Crash continues, -1.1% to $2.12/lb – the 6 month crash in Copper is -26% vs. WTI Oil’s at -35% - the Fed would have to back off the DEC hike to arrest the #Deflation

SPX immediate-term risk range = 1; UST 10yr Yield 2.15-2.36%

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst