Here's a look at key financial metrics for the four department stores that reported earnings this week. There are some really interesting takeaways. We all know sales are weak and inventories are high. By our math those two metrics are about 500bp out of whack. Our sense is that if retail CEOs could pick any two-week period of the entire year where the industry does not have excess inventories, they'd universally pick the two leading up to Thanksgiving/Black Friday. Unfortunately, the ball is not in their court.

Expectations for 4Q, as outlined below, still look too high. For the most part, expectations are for better-trending comps, without a meaningful hit to margins. There's very little chance that this comes to fruition. Base case is that we see a slowdown in sales OR in margins (negative earnings event). Worst case is erosion in comps AND margins.

The point is that there's a better chance than not that we see another round of downward earnings revisions. Either way it's reason for the group to test lower multiples.

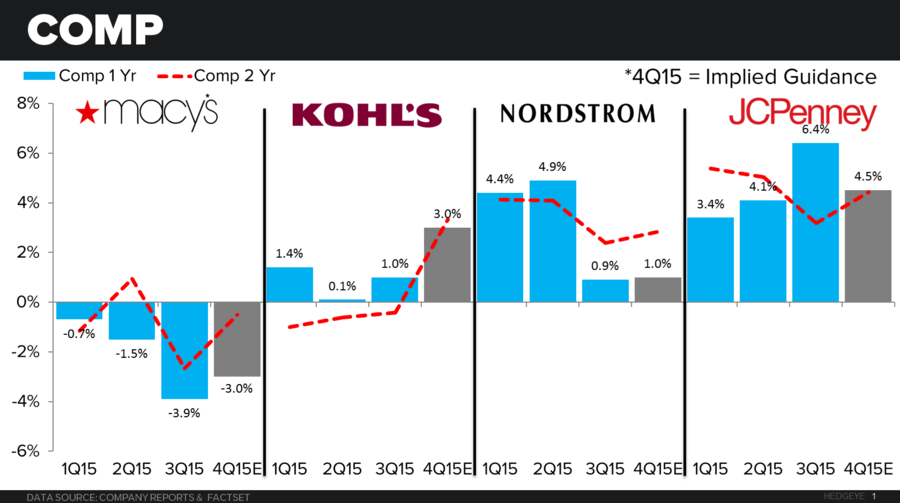

COMP SALES

- The first thing that jumped out at us is that implied fourth quarter guidance is for a sequential acceleration in the two-year comp for every retailer.

- Expectations are highest in 4Q for the mid-tier players -- JCP and KSS -- and are lowest for the upper end (M and JWN).

- KSS 4Q expectations look like the biggest stretch to us.

MARGINS

- Macy's is looking for a 4Q gross margin decline, while the others are implied to be improve sequentially.

- JWN is banking on the biggest 4Q improvement, which we think is partially fair given that it's probably cleaner than the others due to the excessive levels of clearance in 3Q vs last year.

- JCP Margin guidance (Gross and EBIT) seems reasonable to us, but when heading into the holidays with competitors carrying so much inventory, we don't think it’s a slam dunk by any means.

SIGMA

This chart is not pretty -- showing that inventories are growing faster than sales by about 5% for the group headed into holiday. We need to see a huge surge in underlying demand to have margins positive for the group. Our sense is that the department stores end up in Quadrant3 -- right where they started.