Below are our analysts’ updates on our twelve current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this. Hedgeye CEO Keith McCullough’s updated levels for each ticker are below.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

TLT | EDV | JNK

To view our analyst's original report on Junk Bonds click here.

It was a nasty end to the week for the “growth is back” bulls. It was an equally nasty end to the week in equity markets. The S&P 500 was “going to all-time highs” Tuesday before retreating over 3% from Wednesday to Friday.

Macy’s CEO hinting at the ‘R’ word (“recession”) certainly didn’t instill any confidence or convince us that we should ignore talk of an impending earnings recession. To quote its CEO Terry Lundgren on the Q3 earnings conference call:

“We’re in one of those tough periods that retail experiences every 6 or 7 years.”

Company CEOs in pro-cyclical industries are not incentivized to call for recessions. Interestingly, the last time Terry was on an earnings call was Q4 of 2009. As our retail sector head, Brian McGough reminded us, “Macy’s represents about 10% of soft-line retail, or $28bn. In other words, it matters.”

Friday’s poor retail sales print echoed the softness outlined by Macy’s management.

As you can see in the chart below (artistic wizardry brought to you by Keith McCullough), retail sales peaked last November which means:

- The cycle is slowing

- The November number is comping on top of a peak 2014 number, so the chance of more deceleration in November is likely

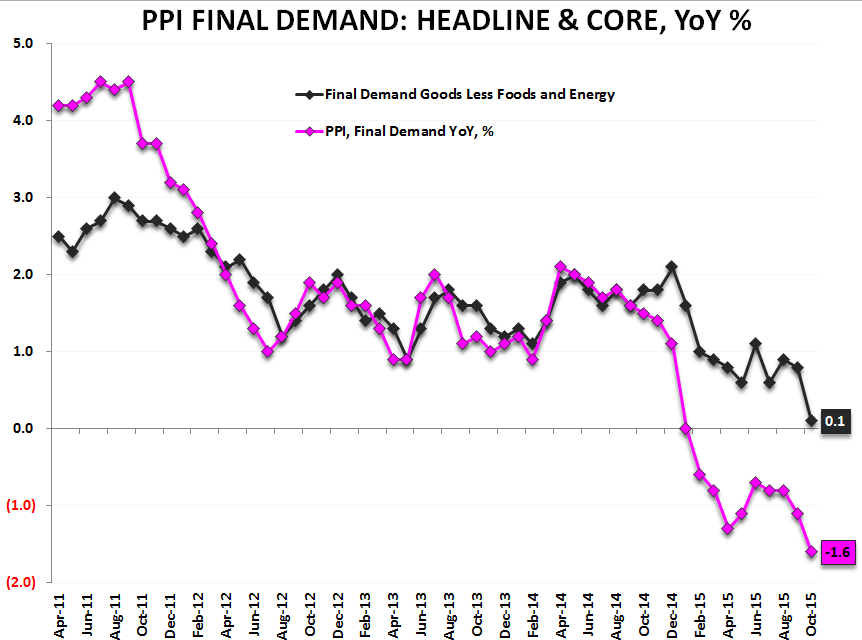

With continued data-driven confirmation that growth is slowing, the awful deflationary PPI numbers released Friday provides an easy segue into outlining why you want to short junk:

- PPI (producer price index) printed -1.6% Y/Y for October

- On a m/m basis, PPI declined -0.4%

- Declines in the energy component certainly bring the index lower, but PPI ex. Food and energy only printed +0.1% Y/Y which is ugly

Deflation crushes the debtor. Especially the debtor with high interest expenses (JNK). Even worse are debtors who borrow at expensive rates and sell something leveraged to commodity inflation because it creates a powerful feedback loop:

- Deflation takes commodity prices lower (Rev. & Cash Flows go down)

- Companies need more funding sooner

- However, a company looks like a worse credit as it’s generating lower cash flows. This means they have to borrow at even higher rates SOONER

- Now, as cash flows are going lower, interest expense is increasing, and funding often evaporates as a company can’t find lenders

This is why deflation is already crushing the high-yield energy debtor.

JNK was down -1.8% w/w with the CRB Commodities Index down -3.5% w/w. Picking up that gain on the short side in JNK beats getting clobbered for being long equities this last week.

WAB

To view our analyst's original note on Wabtec click here.

Editor's note: We added Wabtec to the short side of Investing Ideas back in September. Since then, our call has worked out well with shares falling 18.5%.

The latest carload volume data combined with fleet age demographics continues to point to a sustained period of weak rail car orders, a negative for Wabtec. With Class 1 Railroads curbing capex spending in the face of slowing freight volumes, the downcycle in freight rolling stock is just getting started with WAB still trading at over 19x peak earnings.

MCD

To view our original note on McDonald's click here.

Hedgeye CEO Keith McCullough added McDonald’s (MCD) to the long side of Real-Time Alerts earlier this week after covering some shorts. McCullough cited a number of catalysts for the stock put forth by Restaurants analyst Howard Penney including the launch of All Day Breakfast, MCD's history of returning value to shareholders and additional cost cutting measures.

On a related note, Penney attended MCD's investor meeting in New York City earlier this week. His takeaway from the meeting was that it was "very very bullish" for investors.

Expectations were high, but CEO Steve Easterbrook came to NYC with big changes which have ultimately exceeded those expectations. "The big smile on Steve Easterbrook's face when talking about the current quarter was very telling," Penney writes. "He could not hide the enthusiasm." MCD increased the dollar value returned to shareholders by $10 billion.

Penney and his team still see +30% upside from here.

LNKD

To view our analyst's original report on LinkedIn click here.

Hedgeye Internet & Media analyst Hesham Shaaban updated his current thinking on LinkedIn in a recent note to institutional subscribers.

While the selling environment remains solid, we're still cautious about staying long LinkedIn into its 2016 guidance release. The good thing is that the release won't be until February. As a result, we will get at least 2-3 more updates to our proprietary LNKD tracker before then.

If our tracker continues to improve, then we may stay long into the release. If not, we're definitely going to get out of the way and will reasses the setup post print. More to be revealed.

W

To view our analyst's original report on Wayfair click here.

After going through Wayfair's (W) 3Q and listening to management on the conference call, one question keeps popping up…"Why am I short the stock of a company that is growing its core business over 90% and where 44% of its float is held short?”

But then we consider the following… Wayfair added $266mm in revenue – an astonishing number. But the company still lost money. True, the operating loss narrowed, but only by $13mm. That pegs the company’s incremental margin at only 5.1%. To be clear, companies like Restoration Hardware and Williams-Sonoma – who are consolidating a different end of the home furnishings market (the good end) have incremental flow-through rates of about 20-25%. Heck, even AMZN, which is not afraid to lose money for a very long period of time, has an incremental margin of 15%. Then why are we looking at 5% for W?

The bottom line is that this company is spending – and it’s spending big – around penetrating what management believes to be the company’s total addressable market. Unfortunately, we think they are overestimating it by a country mile, and are building an infrastructure for growth that will not materialize – at least not profitably.

TIF

To view our analyst's original report on Tiffany click here.

Tiffany's (TIF) hit 52-week lows on Friday. Major department stores (JCP, M, KSS, JWN) reported earnings this week and results have been less than stellar.

The biggest sales slowdown and margin hit came at the high end of the space – Nordstrom and Macy’s. Who is TIF’s core consumer domestically? Look no farther than these two comps.

Sprinkle on weaker than expected tourism traffic and you have a pretty bleak picture for TIF numbers when reported next week. Keep in mind that TIF’s flagship store in NYC accounts for 10% of total sales and is highly levered to international tourist traffic.

This callout from JWN management during the company’s conference call paints a bearish picture for TIF consumer demand. When asked about what is going on in the department store landscape Nordstrom management responded very explicitly saying:

"It appears that there has been a slowdown in overall demand from the customer who is purchasing what we sell."

RH

To view our analyst's original report on Restoration Hardware click here.

Restoration Hardware (RH) shares got caught up in the tumultuous selloff of other high-end retailers. But we're still bullish on RH. Here's why.

RH Tampa has just opened. That makes 4 new Full Line Design Galleries in 90 days. And all will be open before the start of holiday shopping season and just in time to house the new product lines RH Modern and Teen. Add up the four stores and we’re looking at about 210k square feet. That alone represents about 25% growth in square footage.

When all is said and done, we still think this company has $11 in earnings power 4-years out, which is nearly double the consensus.

We remain convinced that the debate should not be ‘if or when’ the stock hits $115, but rather is it going to $200 or $300? We’ll be looking at an earnings CAGR of 40-50% over five years. What kind of multiple does that deserve? 20x? 25x? 30x?

We’d argue the higher end.

ZBH

To view our analyst's original report on Zimmer Biomet click here. Here is an update from Healthcare analyst Tom Tobin:

Citi launched coverage on the Orthopedics space this week with a very similar take on the industry as ours. Their rating on Zimmer Biomet Holdings and SYK are both Sells, a rare occurance from a bulge bracket firm. Incidentally, I know the analyst from my prior life on the buyside and always found him credible and well versed in his stocks.

As I understand it, the Sell rating is based on assumptions and research conclusions very similar to our own. It turns out Citi and Hedgeye believe the headwinds to growth facing surgical volumes in 2016 are likely to be material as we come up against the ACA tailwinds of 2014 and 2015, or the #ACATaper.

We received a lot of pushback on our research, mainly based on assumption economics, so it will hopefully help us find a more receptive institutional audience for our non-consensus research conclusions.

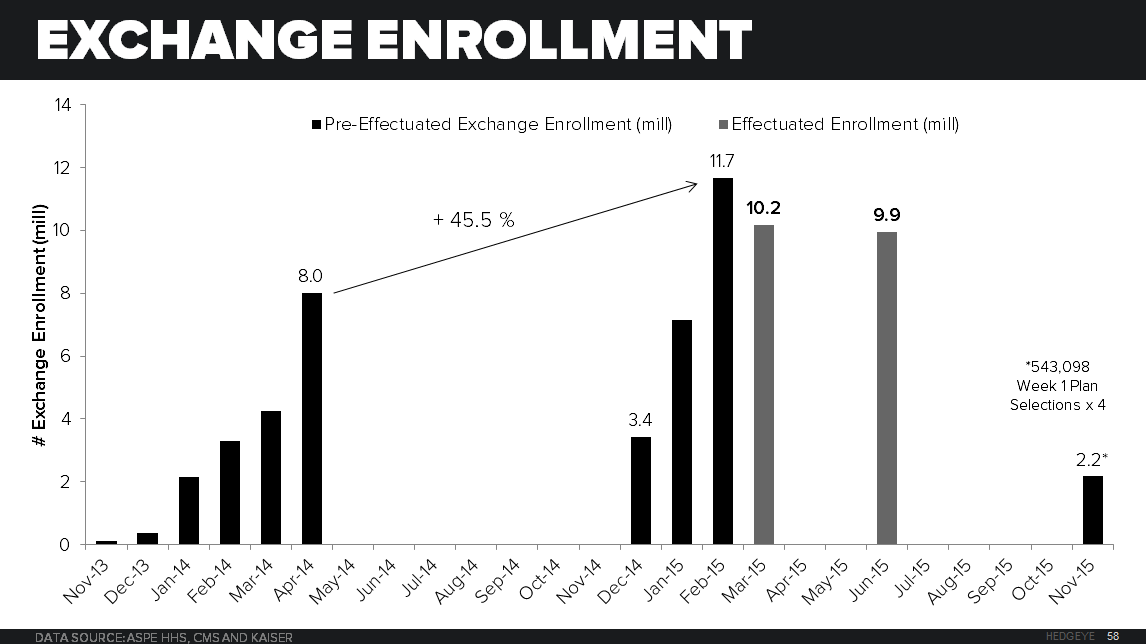

CMS reported this week that, compared to the same time last year, Public Exchange enrollment was up 17% year over year for the first week of open enrollment period. This is a decent beginning as a percentage change, but small in magnitude as enrollees grew from 462K to 543K, or only +80K individuals year over year.

Over the coming weeks we will be updating the enrollment chart below as well as continuing to speak to surgeons about their case volume, pricing, and policy impacts on their hospitals.

GIS

There has not been much notable news on General Mills (GIS) as of late. GIS continues to be one of our top ideas in the Consumer Staples sector. Sector head Howard Penney loves the name for its characteristics during the current macro driven market. Big-cap, low-beta, and their line of sight at growing the top line in a meaningful way, are contributors to our LONG thesis.

ZOES

We attribute a lot of last week's weakness in shares of Zoës Kitchen (ZOES) to style factors. Due to the macro-driven market, high beta, low-cap names such as ZOES have fallen out of favor. We still love the management team and the concept of the restaurant.

If you are a "buy and hold" type of investor this is a name you want to be in for the long run, especially at these values. This company has a long runway of growth which we believe is only just in the beginning stages.

We'll have a clearer picture of the company's outlook next Thursday when ZOES reports earnings.