ECB President Mario “Whatever It Takes” Draghi is teeing up another round of quantitative easing. Draghi addressed the European Parliament this morning ahead of the central bank’s December policy meeting. During the Q&A, Draghi’s responses were exceptionally dovish:

“The option of doing nothing would go against price stability… That is what will outline the strategy for the coming months.”

In a note to subscribers, Hedgeye CEO Keith McCullough broke down Draghi’s comments and the recent policy about-face:

“After suggesting #Deflation wasn’t a risk and European growth was 'encouraging,' our man Mario (ECB President Mario Draghi) pivots to 'downside risks are now clearly visible … and inflation dynamics have weakened.' Finally, some #truth. Don’t forget that Down Euro = #Deflation via Strong USD.”

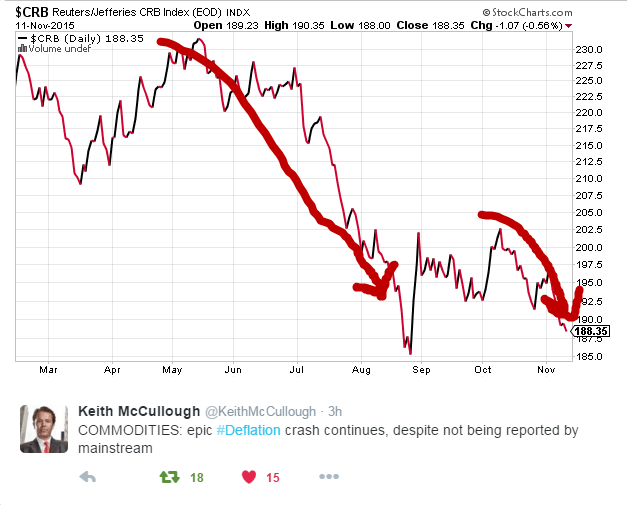

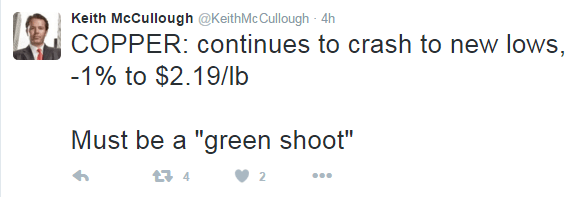

In related deflationary news, commodities are getting crushed.

It is just an awful November for whoever bought into the “reflation” thing that our competition has been pitching since July.