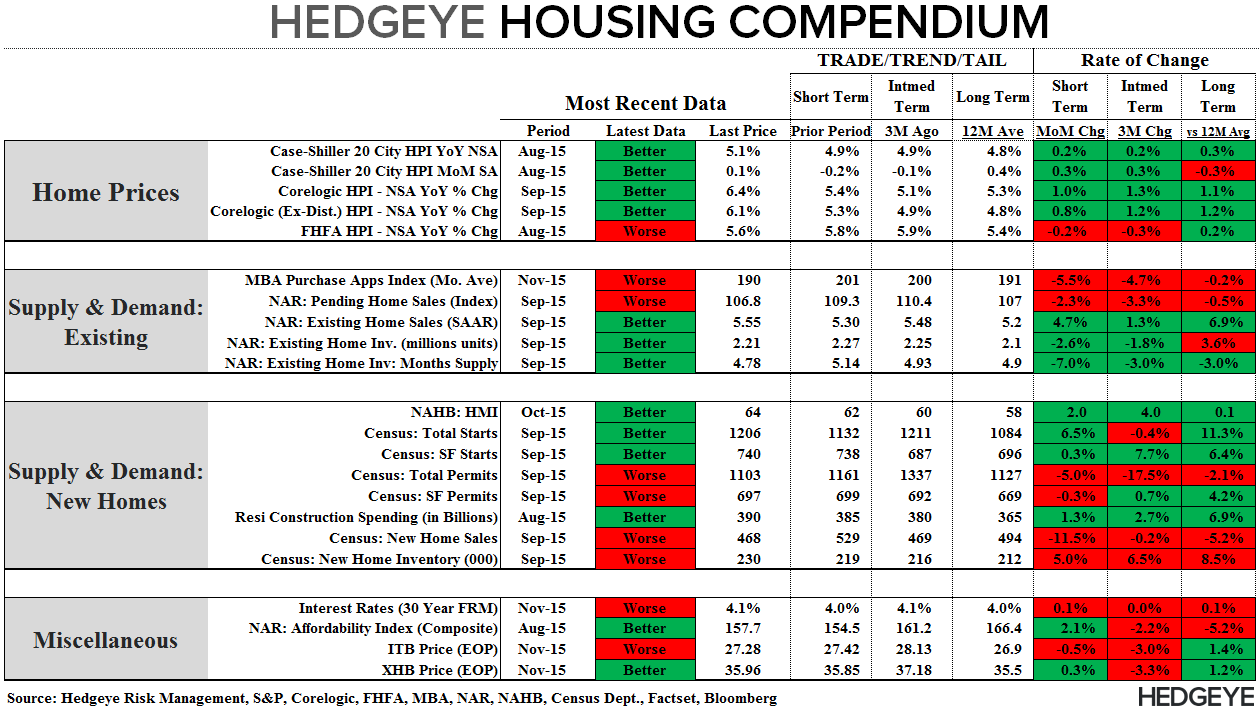

Our Hedgeye Housing Compendium table (below) aspires to present the state of the housing market in a visually-friendly format that takes about 30 seconds to consume.

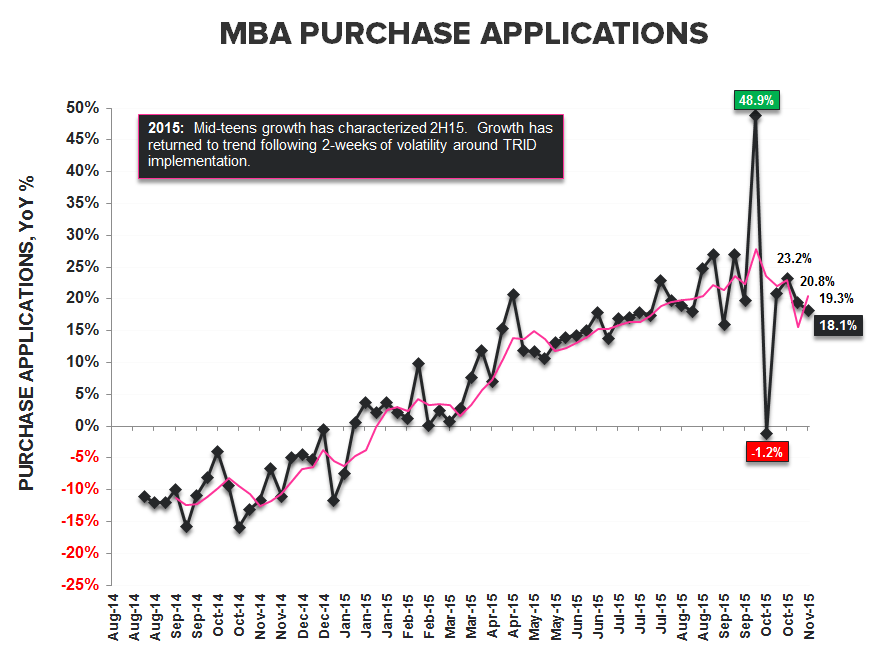

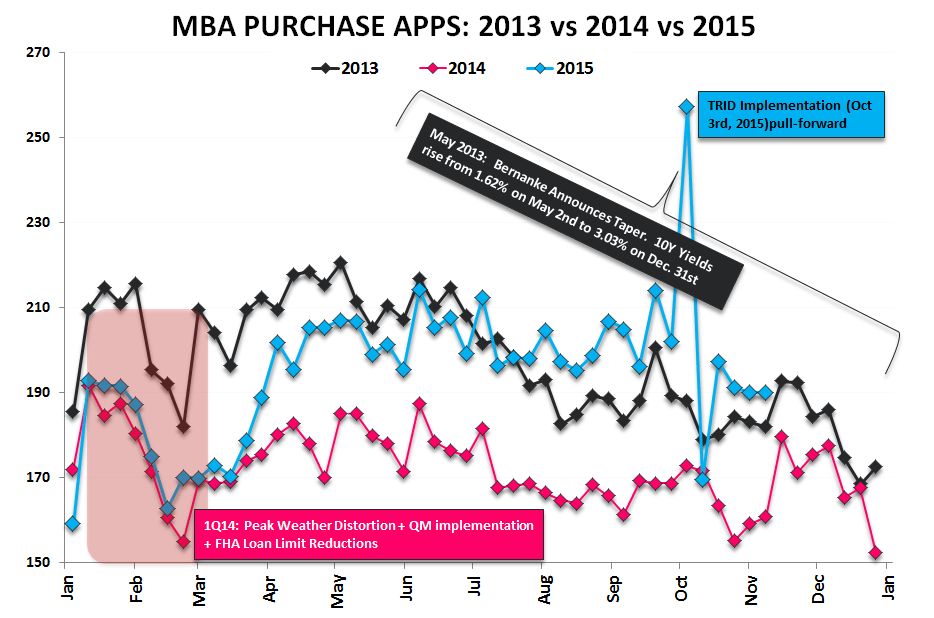

The modest southward drift in Purchase Activity to close out October persisted to start November. Headline Mortgage Applications dropped -1.3% week-over-week as Purchase Activity rose +0.1% and refi activity retreated -2.2% alongside the largest weekly backup in rates since early June.

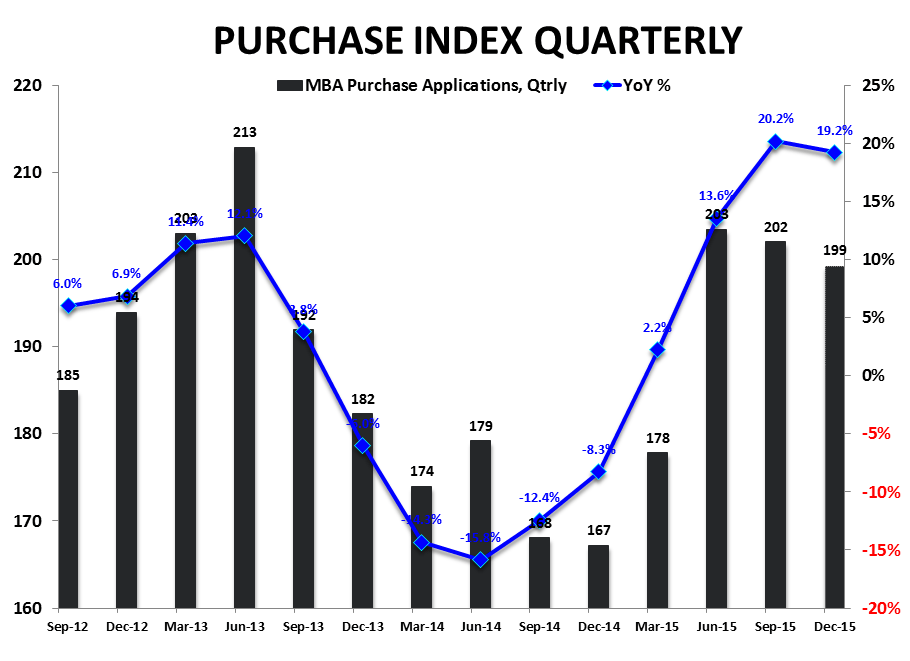

Purchase Demand declined -0.1% week-over-week, leaving the index flat at 190 to start November - at current levels, November is tracking at the lowest level since March (1st chart below). On a year-over-year basis, Purchase Demand decelerated -120 bps to +18.1% with activity currently tracking -1.3% QoQ.

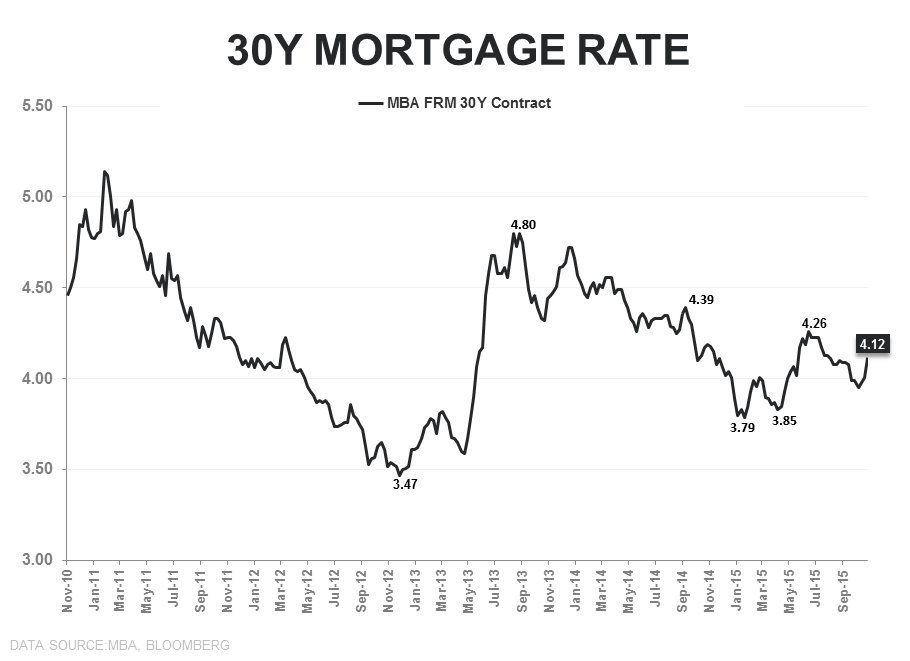

Rates on the 30Y FRM contract rose +11bps sequentially to 4.12% - marking the highest level in 3-months as the bond market bid both the long and short end higher in the wake of the strong October Employment report. At current levels, rates are now north of the 2015 average of 4.02% but remain below the 4.35% average for 2014.

In short, mortgaged purchase activity continued to underwhelm for a fourth week following TRID Implementation in early October. Looking out the next couple weeks, we expect largely trend consistent prints out of Starts/HMI while re-convergence to PHS suggests negative growth in Existing Sales in October (reported 11/23) and potential further softening (TRID-vacuum) in reported PHS/NHS data for October – see our recent note, Catalysts & Cross Currents | Contextualizing the Recent Housing Data, for further detail and context.

About MBA Mortgage Applications:

The Mortgage Bankers’ Association’s mortgage applications index covers more than 75% of mortgage applications originated through retail and consumer direct channels. It does not include loans delivered through wholesale broker and correspondent channels. The MBA mortgage purchase applications index is considered a leading indicator of single-family home sales and construction. Moreover, it is the only housing index that is released on a weekly basis.

Frequency:

The MBA Purchase Apps index is released every Wednesday morning at 7 am EST.

Joshua Steiner, CFA

Christian B. Drake