Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye CEO Keith McCullough. Click here to learn more and subscribe.

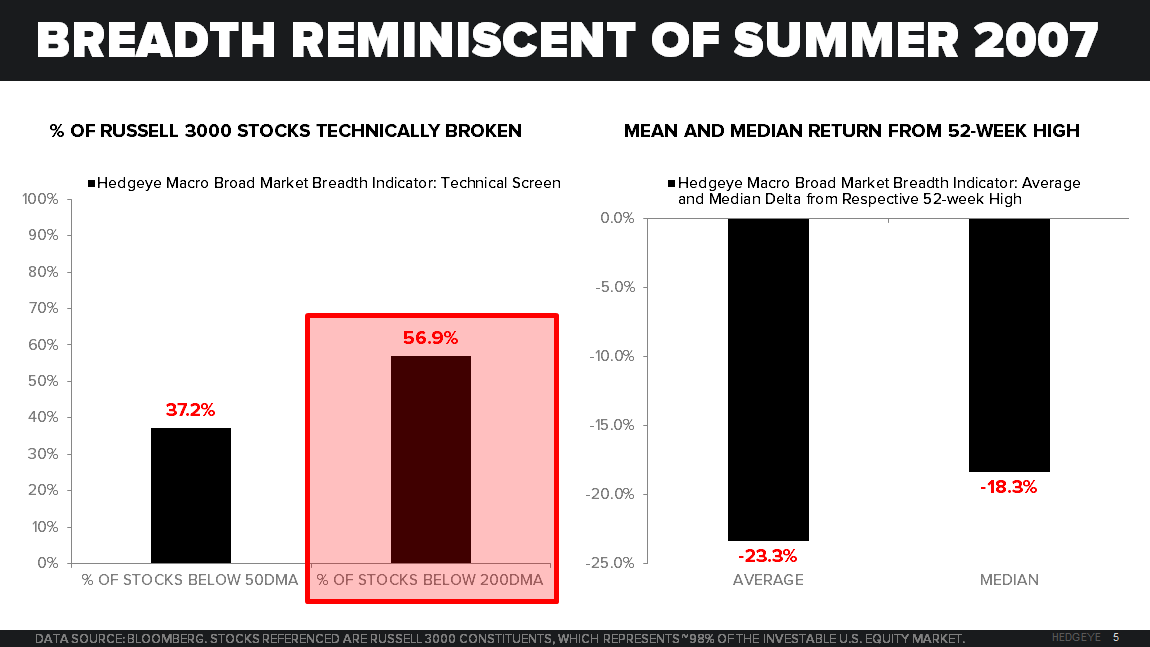

"... With almost 2/3 of stocks in the Russell 3000 (98% of US stocks you could buy/sell) trading below their 200-day Moving Monkey, even the non-quant-one-factor-price-momentum-chart-chaser sees the decay in the internals of the US stock market at this point."