Below is a brief excerpt from The Macro Show earlier this morning. In it, Hedgeye CEO Keith McCullough explains a key risk embedded in financial markets today following Friday’s jobs report, and what to expect if the Fed raises rates:

“Notwithstanding people’s visceral reaction to last week’s "Waldo" jobs number, the Federal Reserve’s potential to make a policy mistake, which is that it raises interest rates into worldwide deflation and growth slowing, is a big risk.

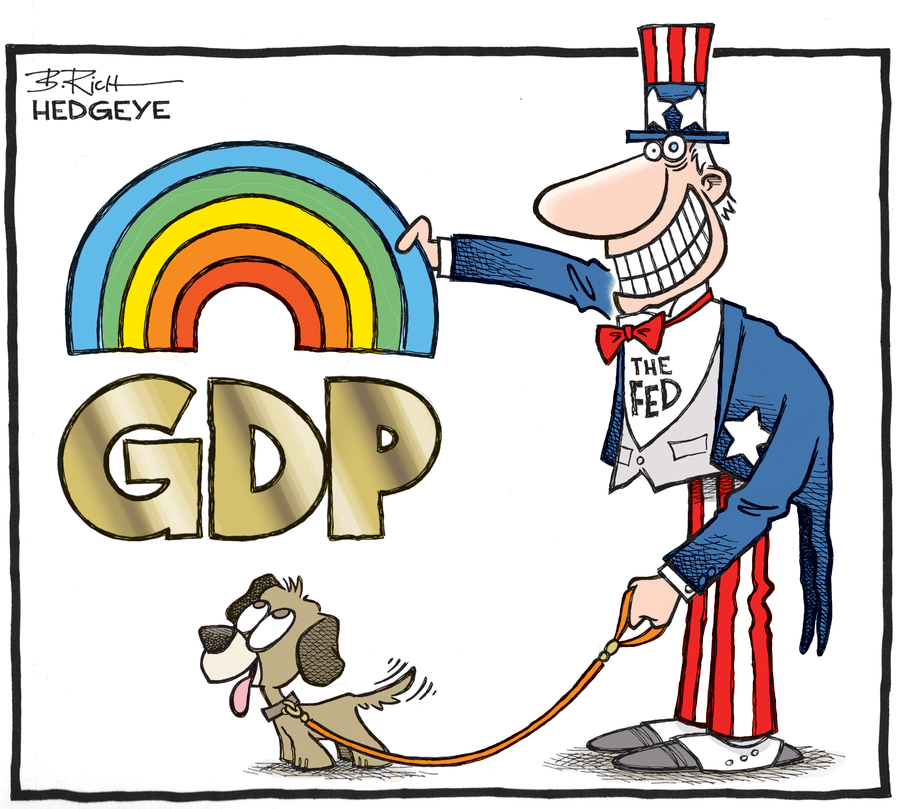

In particular, I am concerned that our forecast for GDP is right and the Fed’s forecast is wrong. Their forecast is that the jobs market is rainbows and puppy dogs and that GDP is going to be 3% to 4%.

We have Q4 GDP between 0.4% and 1.7% so anything in between is way slower than what the Fed thought. God help them if its 0.4%, on the lower end of the range, and they’re raising rates into that.

What does that mean for investors?

McCullough says that should the Fed tighten into a slowdown that would "blow up oil, China, Emerging Markets and anything tied to the aforementioned.”

In other words ... watch out.