“You fail. You Improve. You grow.”

-Jon Gordon

I don’t know about you, but I fail. And when I do, I like to fail fast, so that I can get on with the next.

The aforementioned quote comes from a new book I cracked open this weekend called The Carpenter – A Story About The Greatest Success Stories of All. It’s an easy read. And after a Friday like I had, I needed something easy.

Our profession isn’t easy. But I love that. While being super bullish on #GrowthSlowing (bearish on rates) was dead wrong on Friday, the prospects of the Fed raising into a local and global slow-down being bearish for inflation expectations still looks right.

Back to the Global Macro Grind…

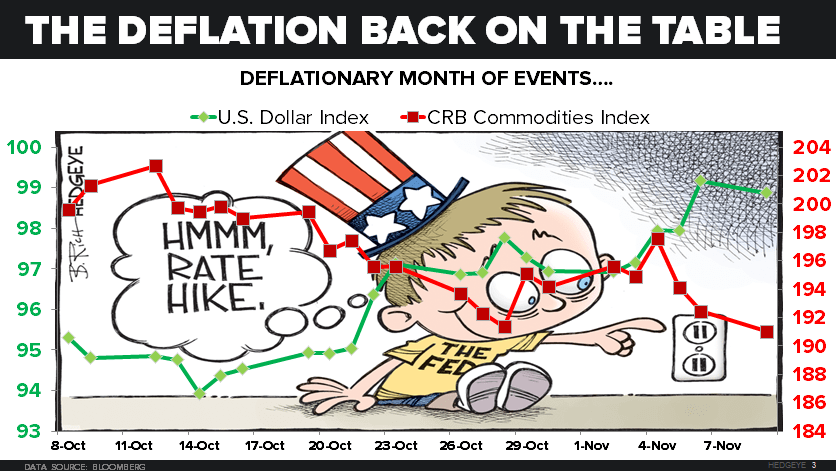

Being bearish on inflation expectations is another way of saying that you’re bullish about being positioned for the mother of all Global Macro risks, #Deflation. If you’ve failed to recognize that risk in the last 1.5 years, you need to improve and learn about it, fast.

The way that the #Deflation Risk really kicks in are twofold:

- The US Federal Reserve raises rates into a domestic cyclical (and secular) slow-down

- The rest of the world responds to slowing by “easing” (devaluing currencies) and raising the value of the US Dollar

Post the headline “great” US jobs report on Friday (which actually saw Non-Farm Payrolls slow to 2.01% year-over-year growth vs. the US Labor Cycle peak of 2.34% growth in FEB), this is what happens in FICC (Fixed Income, Currencies, Commodities):

- US Dollar Index +2.3% week-over-week to +9.9% YTD

- US 10yr Yield +18 bps week-over-week to 2.33%

- EUR/USD -2.4% week-over-week to -11.2% YTD

- Canadian Dollar (vs. USD) -1.7% week-over-week to -12.7% YTD

- Mexican Peso (vs. USD) -1.9% week-over-week to -12.2% YTD

- New Zealand Dollar (vs. USD) -3.7% week-over-week to -16.3% YTD

- Commodities (CRB) Index -2.3% week-over-week to -16.9% YTD

- Oil (WTIC) -4.9% (to $44.29/barrel) week-over-week to -25.5% YTD

- Gold -4.7% week-over-week to -8.4% YTD

- Copper -3.3% week-over-week to -20.8% YTD

In other words, everything that has been signaling #Deflation to you in the last year, resumed its crash on Friday and has not improved upon where it might be “reflating” in a Down Dollar scenario. It’s right back into what we call Quad4.

While US Equity markets didn’t like the “good is bad” response to the jobs print on Friday, they did have a good week both on an absolute basis and relative to something like Emerging Market Equities (MSCI) which were only +0.5% on the week and still -10.9% YTD.

The Style Factors of the US Stock Market that performed best were the ones that have been the worst for the last 6 months where markets have been pricing in both a top-down Global slow-down and bottom-up “earnings” ones:

- High Short Interest Stocks were +1.9% week-over-week vs. -7.5% in the last 6 months

- High Beta US Stocks were +1.7% week-over-week vs. -8.5% in the last 6 months

- Small Cap Stocks were +1.6% week-over-week vs. -8.3% in the last 6 months

*Mean performance of the Top Quartile vs. Bottom Quartile of SP500 companies

And, from a Sector Style perspective, small/mid cap banks had a big week inasmuch as the Financials (XLF) did, closing +2.7% on the week getting the XLF back to 0.0% for the YTD (for people who have been bullish on Financials all year, flat is the new up).

Since one of my favorite US Equity Sectors on the short side (alongside US Retailers, XRT) has been the Financials, that made me very wrong last week after being right into their lows in September.

Yes, one can be wrong for what we call the immediate-term (TRADE) while being right on what we call the intermediate-term (TREND). Unless you’re an Old Wall strategist (or Madoff), you can’t be right all of the time.

But where to from here?

Well, since the causal factors that drove the SEP lows were:

- Worldwide #Deflation

- GDP #GrowthSlowing

I’m going to stay with both because:

A) US Dollar strength perpetuates both commodity and leverage-linked deflation expectations

B) We don’t have US GDP bottoming in rate of change terms until potentially Q2 or Q3 of 2016

If the Fed raises rates into what’s been the most accurate rate of change calls on both inflation and growth, I think they’ll be talking about cutting those rates within 1-3 months of the 1st “hike” anyway.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.04-2.36%

SPX 2033-2119

RUT 1144--1213

USD 97.55-99.46

EUR/USD 1.07-1.10

Oil (WTI) 43.03-45.96

Gold 1078-1127

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer

Join Hedgeye CEO Keith McCullough live on The Macro Show at 9 am ET.