OVERVIEW

It was announced this morning that Goldman Sachs sold 1.3 million shares of Valeant stock that was pledged by CEO, J. Michael Pearson in exchange for a $100 mill loan. Pearson owns ~10 mill shares, of which ~2 mill are pledged as collateral in exchange for loans "to fund tax and other equity incentive awards and purchases of Company shares". There are also 1.2 million shares in addition to the 10 million that belong to Pearson's grantor retained trust (GRAT), but are not included in the total as Pearson has "no pecuniary interest". The proxy filing does not explicitly state whether the 1.2 million GRAT shares were used as collateral for the loan.

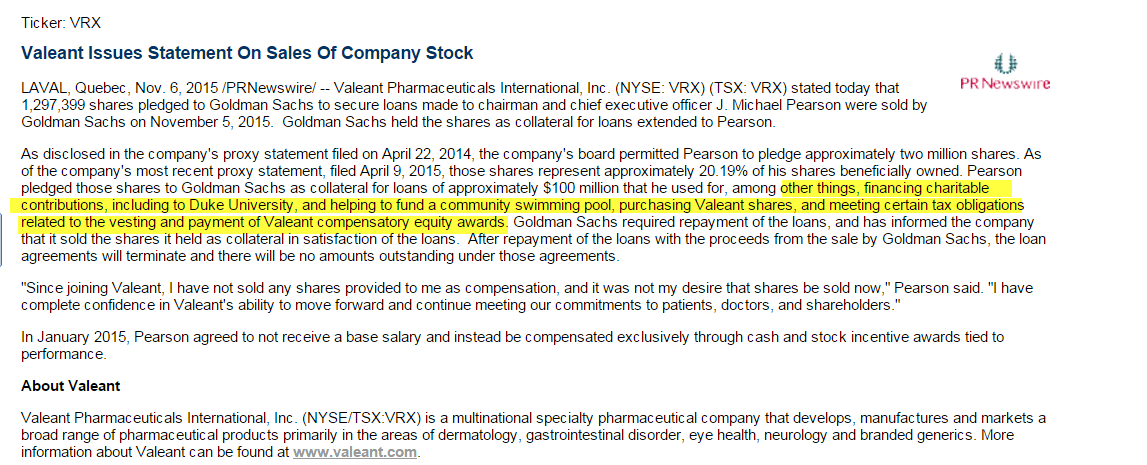

According to Valeant's press release, the $100 mill in loan proceeds was used for "among other things, financing charitable contributions, including to Duke University, and helping to fund a community swimming pool, purchasing Valeant shares, and meeting certain tax obligations related to the vesting and payment of Valeant compensatory equity awards".

This is a problem if the 1.3 million in pledged shares were unrelated to Pearson's GRAT, because the proxy filing explicitly states that the proceeds of those loans were used only "to fund tax and other equity incentive awards and purchases of Company shares". There is no mention of charitable donations, and brings into question what else Pearson may have used the proceeds of the loan for?

Michael Pearson's large stake in the company and compensation tied to TSR has been a cornerstone of the bull thesis, providing assurance that incentives are properly aligned. Therefore, it is clearly a problem if Michael Pearson used the loan proceeds for anything other than what is stated in the proxy filing.... even if it is for "charitable" purposes. It is possible that the charitable contributions were made through the GRAT, although a GRAT is usually established as a way to transfer wealth to relatives to avoid paying a gift tax.

We have no problem with the practice of pledging stock as collateral in exchange for a loan. What we do have a problem with is if Pearson used the proceeds of the loan for purposes other than what was disclosed to shareholders. Given the falling stock price and heightened scrutiny, we would welcome an audit of the loan proceeds.

pearson allowed to sell stock

The 2014 proxy filing states that Michael Pearson is not permitted to sell "net shares until 2017". However, the proxy filing in 2015 "permits Mr. Pearson to sell 3,000,000 net shares.... plus transfer an additional 1,000,000 net shares in charitable contributions". This represents 50% of his stake (net of the 2 mill shares pledged as collateral), compared to 0% in 2014.

"Valeant has adopted a policy generally disallowing future pledges and is permitting Mr. Pearson to sell shares, which may reduce the level of pledging"

<chart5>

This is a big change from the policy of prior years. Pearson has touted that he has "not sold any shares provided to [him] as compensation" since joining Valeant. However, we don't see any difference between selling stock and pledging shares as collateral for a loan, and based on the commentary in the latest proxy filing, neither does the board.

Please call or e-mail with any questions.

Thomas Tobin

Managing Director

@HedgeyeHC

Andrew Freedman

Analyst

@HedgeyeHIT