We are adding Boulder Brands (BDBD) to our Hedgeye Consumer Staples LONG bench.

HEDGEYE OPINION

BDBD is a company we have been following on the sidelines for the past six months. One quarter does not make a trend, but with this most recent earnings call and the upside from a potential acquisition we feel confident in dipping our toes into this one.

3Q15 RESULTS

Business trends were mixed in the quarter, but it appears they have bottomed out and stabilized. Management has embraced SKU rationalization, and the efficiencies gained from that will play out over the next 12-18 months. Reported net sales decreased 0.7% in 3Q15 to $132.9mm, although topping consensus estimates of $130.2mm.

Gross margin declined 4.8% in 3Q15 to $48mm, or 36.1% of net sales versus 37.7% in 3Q14, additionally, actuals fell short of consensus estimates of 36.72%. This poor performance was driven by a mix shift to the lower margin Natural segment (Udi’s, Glutino, Davies and EVOL) from the higher margin Balance segment (Smart Balance, Earth Balance and Level Life).

BDBD reported non-GAAP diluted EPS of $0.08, beating consensus estimates of $0.06 by $0.02.

Management reiterated 2015 guidance of $0.20 to $0.25.

NOTABLE COMMENTARY FROM THE CALL

- Identified SKUs to be rationalized and will begin the process in 2016

- Will discontinue Level Life

- Launched EVOL cups in Q3 in Target stores under three platforms, veggie, fajita and breakfast scrambles

- Management is working diligently on improving the operations of the company by outsourcing certain manufacturing to co-packers and increasing efficiencies in their four North American plants

- Seeing marked sequential improvement in core categories Udi’s breads and spreads

- Although net sales declined 0.7% in the quarter, consumption was actually up 0.5%

- Udi’s net sales increased 7.7%, consumption increased 8.5%

- EVOL net sales increased 24.8%, consumption increased 30.3%

- Earth Balance net sales increased 3.6%, consumption increased 3.7%

- Company experienced declines in Smart Balance and Glutino (down -5.7%)

- The company is experiencing higher yield loss in bread after implementing processes to reduce consumer complaints about air pockets and holes in the bread

- Smart Balance is seeing velocity improvements, but offset by distribution losses

- BDBD gluten free products were up 6% in the quarter, being outpaced by the segment, management determined to get back the share lost

- Gluten free category growth has moderated but still growing much faster than the broader food segment

- Foodservice category doing very well and accretive to margins, one current big partner is Pizza Hut

STRATEGIC OPTIONS PROCESS

On August 6, 2015, BDBD announced that its Board “has authorized a process to explore a range of strategic and financial alternatives to enhance shareholder value.” At that time the company engaged William Blair as its financial advisor to assist with the process. They have been mum about the project to date, but given the time that has elapsed they must be nearing a conclusion sometime in the next quarter. There are a range of possibilities that can come with this, but we believe all scenarios include a sale of all or a portion of the company.

As we have gone back and forth, we came up with a total breakup (or sale) of the company as a most likely scenario. In which a strategic buyer (CAG, GIS, PF) would purchase the entire company outright or if there is a sale of the parts, purchase just the highly valued assets, EVOL and Udi’s. Leaving Earth Balance, Glutino and Smart Balance to financial buyers. We have our bets on a total outright sale of the business.

Interim CEO James Leighton has done a good job of stripping out costs, and streamlining the operations, all while improving the trajectory of the business. Can they succeed on their own? Maybe.

VALUATION POTENTIAL

It’s not hard to see the upside in this company, relative to its peers it is undervalued, currently trading at just 11.1x EV / NTM EBITDA.

It has been a volatile year for BDBD shares. Currently trading 26% below their 52 week high of $11.68 on 2/24/15, and 34% above from their 52 week low of $6.42 on 7/8/15.

WALL STREET CONSENSUS

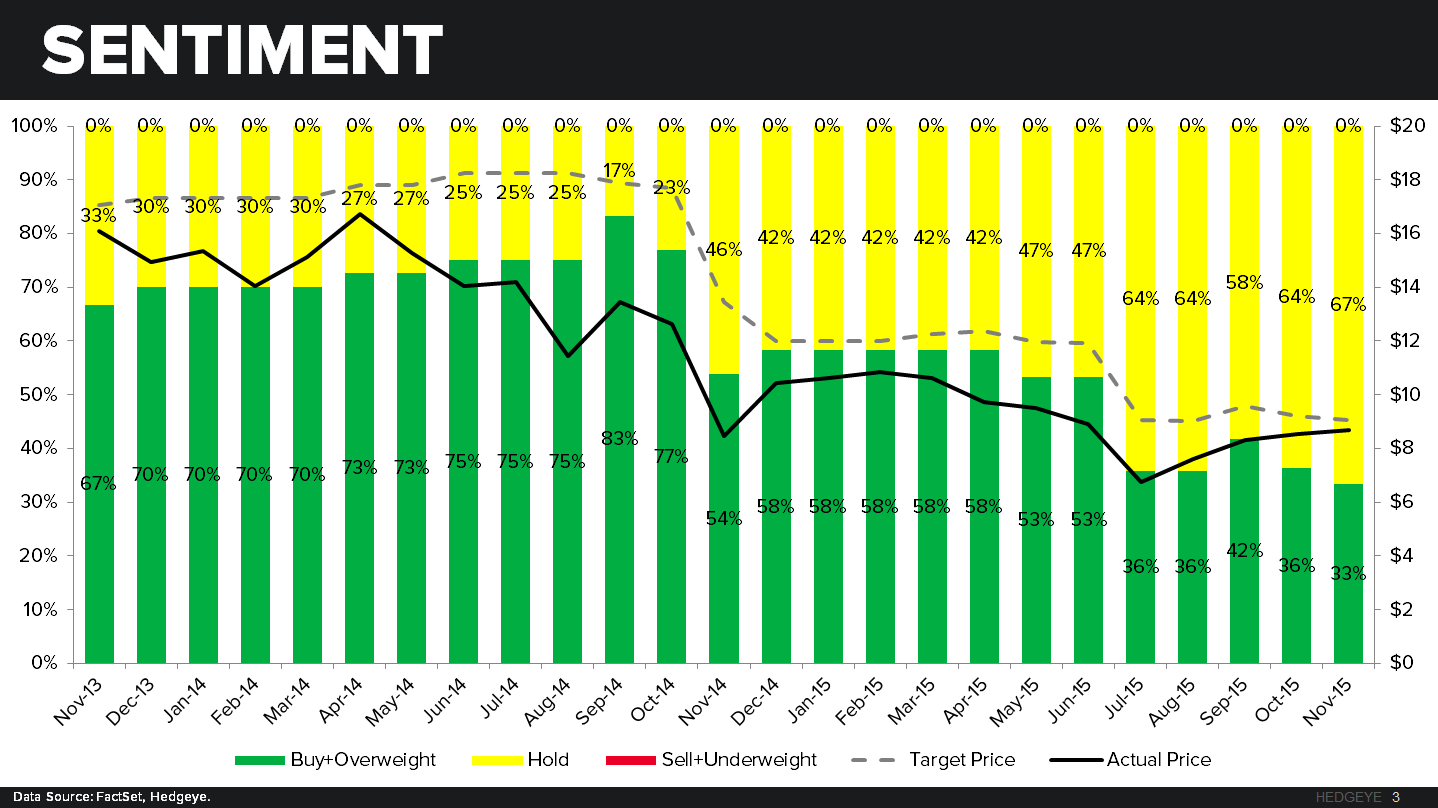

Confidence in this company’s ability to succeed has continued to wane over the last year. In September of 2014, 83% of analyst rated it as a Buy, now just 33% rate it as a Buy. Where is the love? We firmly believe in this company’s ability to create shareholder value organically, as well as through their strategic review process.

We will update our thinking on the name over the coming weeks and bring forth additional insights we have.

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst