We said it earlier this week, and we’ll say it again – 3Q Marks a critical inflection point for KATE’s financial characteristics, as well as the stock. The market likes what it sees today, but let’s be real…it had previously lost 44% year-to-date, so a high-single-digit gain in a day is one of many battles it needs to win in order for anyone who is bullish – especially us -- to declare victory. We’re not making any changes to our model – despite management’s best efforts to take consensus down. There’s a lot of pent-up leverage associated with; a) where it is in the store growth/maturation curve, b) the fact that it is about to cycle a year’s worth of efforts to cull bargain-priced products, c) product initiatives like Home and Watches, and d) an e-comm business that just grew 30%+ on an already-high internet sales base of 20% of total. In fact, KATE just put up a 16% comp in total, which – as of yet – is the best comp of any company in North America.

We get that management wants to keep expectations low. But we’ll say again what we’ve been saying all along…”Watch what they do, not what they say.” We’d change a lot with how the company communicates with the Street, but -- without hesitation -- we would not change a single thing about how it manages its business.

For those who want to scrutinize guidance, here’s some ammo.

Sales Guidance – For the 4th quarter the current guidance implies a growth rate in the range of 4-22%. This, of course, is ridiculous. The company simply did not change annual guidance despite the 3Q beat. And no, we don’t think it accurately reflects the company’s internal forecast accuracy. It just shows where guidance stands in the hierarchy for KATE.

A few things to keep in mind…

1) KATE started to pull back on its Flash Sale promotions in 4Q14, eliminating a 75% off Flash Sale that occurred in mid-December 2013. We’ve seen one Flash Sale QTD in 2015, and we would expect the company to repeat the Black Friday sales promotion -- meaning we shouldn’t see the same Flash sale headwinds we’ve seen over the past 3 quarters which cost the company a total of $10mm in lost revenue.

2) Management cited 4 particular headwinds that would cost the company $30-$40mm in sales in 4Q. 1) Fx, 2) the licensing of the watch business to Fossil, 3) quality of sale efforts in the wholesale channel, and 4) new store openings pushed into FY16.

Perplexing Gross Margin Guidance – GM was down 160bps in the quarter against a tough comp last year when shifts in the calendar led to fewer promotional events during the quarter. On a 2yr basis the change in gross margin was essentially flat sequentially. For YTD, we’ve seen 75bps of gross margin leverage, but the 60.4% guide for the year assumes that gross margins are flat for the year implying that 4Q is down 150bps (which excludes the $8mm charge taken in 4Q14 from Jack/Saturday). That’s up against a -190bps GM (adjusted) number in the 4th quarter of last year which was caused by FX pressure in Japan, and outlet pull forwards; the exact same reasons cited this year. Additional FX pressure can explain away maybe a fraction of the confusion over guidance, but we have a hard time getting to the company's numbers. The punchline here is that there’s no way KATE is going to simply ‘hit’ (and not beat) its fourth quarter GM guidance.

Same for SG&A/EBITDA Margin Guidance – The top end of the sales and EBITDA guidance assumes a 15.7% EBITDA margin rate for the year. That implies that the company will get just 50 bps of leverage in 4Q as it comps against $29mm in charges from Jack/Saturday. If we net out all of the charges associated with those two brands last FY, we get to an EBITDA margin rate of 15.9%. To date this year the company has printed 300bps of margin leverage excluding all Jack/Saturday charges and 390bps of leverage reported. We’d have to see a material weakening in the business to get to the implied profitability rate in 4Q. Management couched it by saying ‘at least 200bps of leverage’ for the year, the ‘least’ part was a new addition.

Store openings – Management was cagey about its store opening targets beyond FY ’15, but it was clear that a) some store openings were pushed domestically into FY16 which explains the 17% sq. ft. growth rate in the quarter, and b) NA is only 50% built out. KATE started building out its own real estate footprint in earnest 2 years ago and there is a lot of runway left on the comp line as the new additions start to hit the peak part of the store maturation curve.

11/04/15 05:15 AM EST

KATE | CRITICAL INFLECTION POINT

Takeaway: We think that 3Q is fine, and that after 7 yrs, EPS will inflect and begin to lend valuation support. One of the best risk/rewards in retail

Though few sane people would argue this by looking at how the stock trades, we think that the quarter looks solid for KATE, and the long-term investment thesis is fully on track. We think timing here is absolutely critical, and that timing finally favors the long side. Keep in mind that this company has been a serial restructurer, having traded under three different tickers in five years, and the only constant during that time period has been a lot of red at the bottom of the P&L. Even though KATE has been executing extremely well on its plan, the fact is that the stock has looked extremely expensive to the average investor who cared about nothing but current year earnings. This is why the stock got annihilated when the category (Kors) hit a wall. It simply had no valuation support. That’s why we think that the quarter we’re currently in (4Q), will be critical, in that the company should earn 30% more than it did in all of 2014. In fact, we’re a few short months away from people focusing on $1.00+ in earnings power for next year – a level it hasn’t seen since 2007. People will be looking at a name trading at 18x an earnings rate that should grow 50%+ for 3-5 years.

So why has the stock been acting like death? For starters, it’s perfectly fair to be worried about what management will say on the call. Even though we think the trends look good, the fact is that KATE’s track record with communication is not good. We think it’s getting better, but wounds take time to heal. In addition, it’s extremely tough to dispute that tax-loss selling was an issue here. Last week was fund year-end, and KATE was down 44% YTD through Friday. The double whammy of tax-loss selling and the “what will they say on the call next week” served as a vicious cocktail for the stock, we think. There was virtually no fundamental news out – even out of COH last Tues – that should have rocked this name like it did.

Watch what KATE does, not what it says. Ultimately, ‘what it does’ will create the value we know is about to be unlocked. Do we need better disclosure? Yes. Enough financial information to build a basic retail/multi channel model (like RL, KORS, COH, and pretty much every other real company that sells product in this space)? Yes. Management to put it’s money where its mouth is and buy stock when real believers in the story are sweating it out on the down days? Yes. A CFO who is on the conference calls (like every other company in the S&P)? Yes, please. But these are factors that can all be fixed – quite easily, actually. The thing that KATE has down pat is execution on the Brand growth and profitability strategy. We’ll take that.

Ultimately, we think we’ve got between $2.50-$3.00 in EPS power in three years. The CAGR it takes to get there gets us to $62 on the low end (25x $2.50) to $90 on the high end (30x $3.00). Either way, we’re talking around a 3-4-bagger from where the stock is today. This is one of the best risk rewards out there from where we sit.

Here’s a Few Considerations Regarding the Quarter

The ‘Space’ – COH indicated on its call last week that the premium North American women’s and men’s handbag category grew at a LSD rate in the most recently completed quarter (no change from 3 months ago). That’s not a big surprise to us considering that two of the biggest competitors in the space, COH and KORS with market share in excess of 40% have comped negative in North America at a HSD to LDD clip. But, if we do some quick math on that and assume that a) COH and KORS market share = 40%, b) the category is growing at 3%, and c) the absolute dollar growth rate for COH and KORS is ~ -5%. Then that means that the rest of the space is growing in the high single digit range. For a company like KATE, with only 5% share of the US handbag market and significant market share available to capture as the company builds out its US distribution network, that’s not as ‘toxic’ an environment as commentary would otherwise suggest.

Flash Sales/Promotions – this might be the first quarter in recent memory that there has not been excessive chatter about the space being overly promotional. That’s particularly the case with KATE, as the company continues to step off the Flash Sale accelerator in the DTC channel while working with wholesale partners to remove the brand from promotional events (in other words, when you see online promos at retailers like Lord & Taylor, it includes Coach, Kors, but not Kate). At DTC in NA specifically, KATE ran 4 sales in 3Q15 compared with 5 in 3Q14. 75% off Flash Sales were pared down from 3 to 1 in the quarter the company will report on Thursday. In 2Q (reported 90 days ago) the pull back in Flash Sales cost the company $6mm in revenue or three percentage points of growth on the adjusted consolidated revenue line, and 400-500bps on the comp line (reported comp of 10% vs. mid-teens adjusted for change in Flash Sale strategy). Due to timing KATE had 3 days of its mid-year Friends and Family sale pushed into the 3rd quarter vs. only one day last year, and the company added an additional 25% of Sale Items event in early September. The bottom line is that on an underlying basis, KATE is absolutely, positively less promotional than a year ago, as well as on a sequential basis.

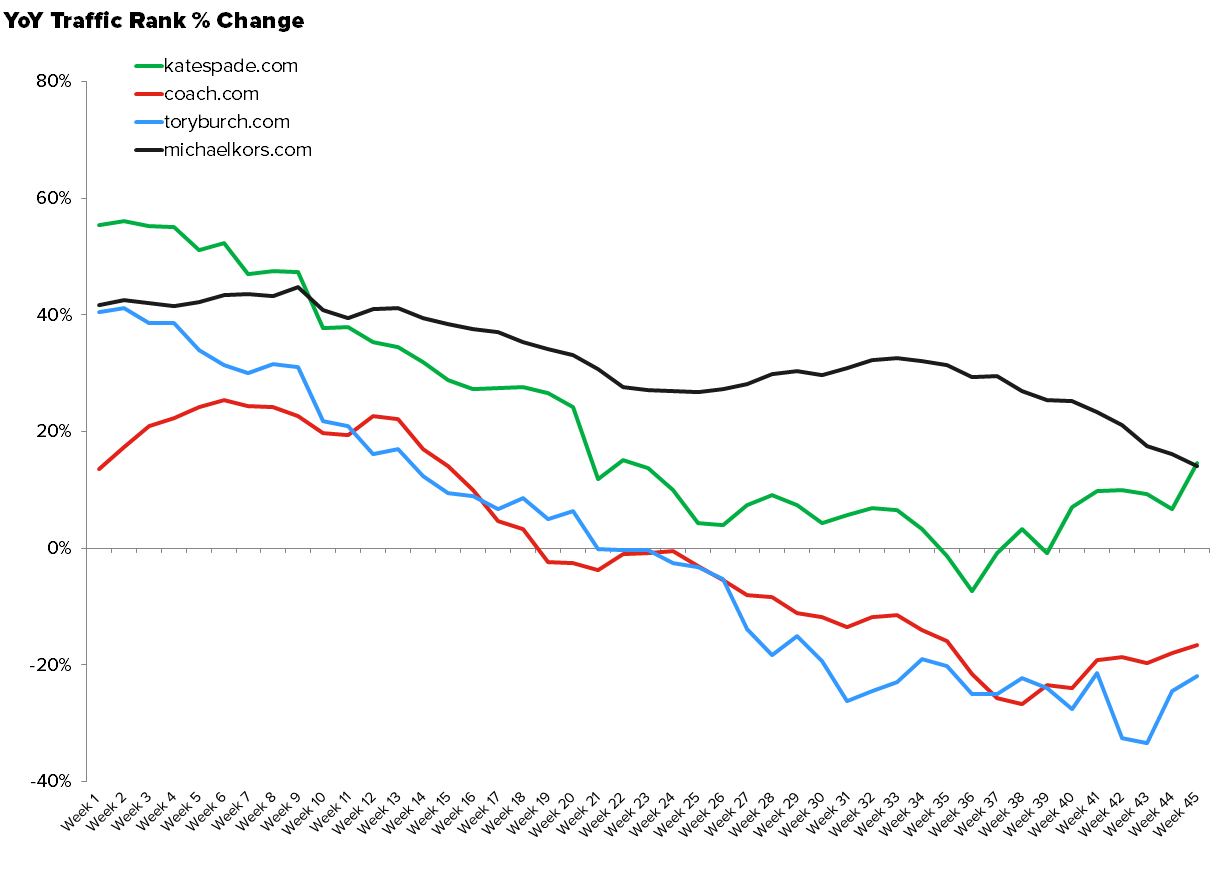

E-commerce trends – sequentially e-comm growth ended the quarter right in line with where the company ended the 2nd quarter with the index traffic rank up 7% YY based on our analysis. Traffic rank is a 90-day moving average that takes into account both unique visitation and page visits per user and ranks each URL relative to the internet in aggregate. Since late August, when KATE bottomed it has outperformed the rest of the space (COH, KORS, & Tory Burch) by a wide margin (see chart 2). Comparisons at the e-comm level ease up in the 3rd quarter as KATE comps against a 23% growth rate vs. a 26% growth rate in 2Q (assuming a 20% e-comm weight). That’s not as marked as the sequential step down in Brick and Mortar compares where the company reported a 32% comp in 2Q14 and a 13% in 3Q14, but on the margin compares in this channel ease up in the 3rd quarter as KATE continues to pull back on its Flash Sale posture. The bottom line is that recent trends, which will presumably be implicit in the company’s guidance, are directionally encouraging.

GM guidance – KATE is guiding to a 60.4% gross margin rate for the year, which is flat to LY after adjusting for the $8mm inventory right down hit the company took in the 4th quarter from Jack/Saturday. YTD the company has leveraged Gross Margin by 190bps (65bps if we adjust for the $6m hit in 2Q14 from the Kate Spade Saturday inventory liquidation) and current guidance would imply that gross margins need to be down in excess of 125bps in 2H. The company has a tough compare in the 3rd quarter, but we have a hard time reconciling the delta between the 1H and 2H performance. Especially when you consider that the factors cited as headwinds (Fx, increased outlet penetration) should be annualized by 4Q15 when the company comps the Juicy outlet pull forward and Fx pressure from 4Q14. On the positive side, KATE will see the benefit of the JV conversion, the elimination of Jack Spade and Kate Spade Saturday retail doors, and increased licensing penetration. We don’t have KATE getting back the full 210bps of GM it lost in FY14, but given that there is 130bps from inventory right downs alone, and the current trends we’ve seen in the business it only makes sense that the company gets the majority of it back.