Hedgeye has long been skeptical about Valeant Pharmaceuticals (VRX). Last summer, before the barrage of bad news broke for the company, we issued a comprehensive Black Book laying out the short case. In it, our Healthcare analyst Tom Tobin highlighted Valeant's unsustainable business model.

Incidentally, Tobin's team sent subscribers an update just now explaining why they believe the stock may fall another 75% from here.

CLICK HERE to access their original institutional research report.

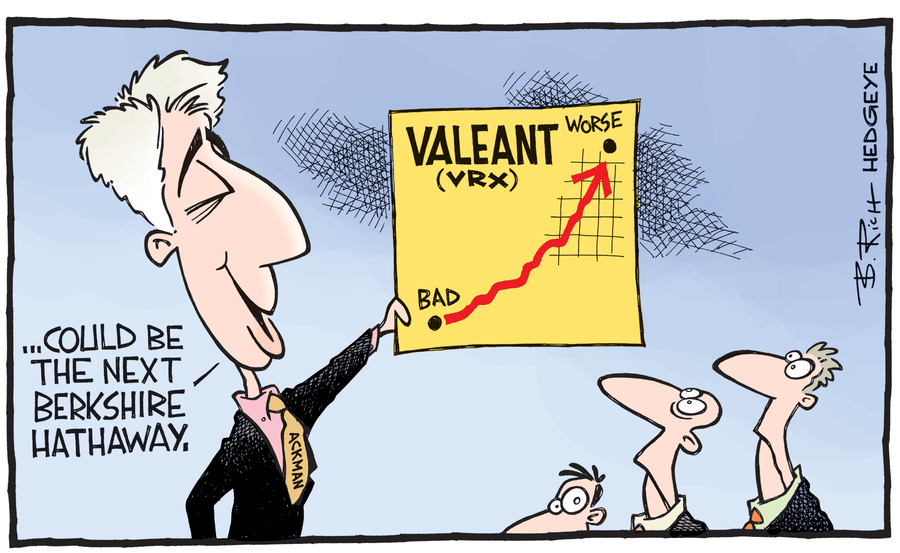

Fast forward to today... In the most recent deluge of bad news for Valeant and hedge fund manager/shareholder Bill Ackman, Congress is now getting involved. Not a good sign. Apparently, a bipartisan special committee has been put together to “better understand [Valeant’s] drug pricing” (sic “price gouging”). In addition, it was disclosed earlier today that Bill Ackman sent a letter to Valeant CEO warning that his reputation is at "grave risk" and Valeant is at risk of becoming "toxic."

Talk about being a day late and a dollar short. Shares of VRX are down 14.6% today on the news.

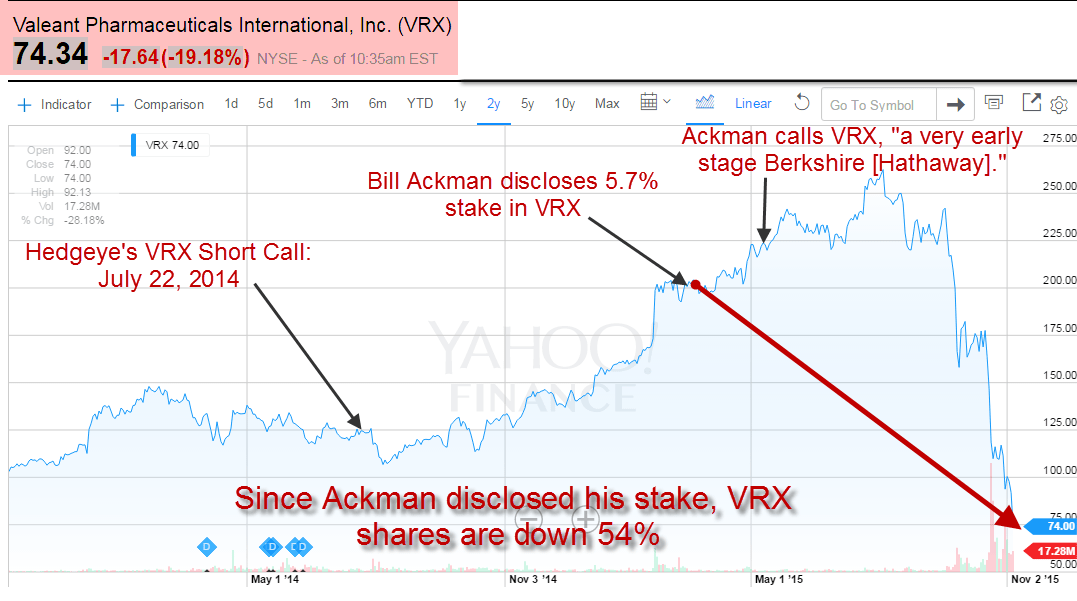

But that's not the worst of it for Ackman. Since March, when his hedge fund Pershing Square Capital first disclosed it's 5.7% stake in Valeant, the stock has fallen 54%.

Our Healthcare team warned subscribers of the many “underappreciated risks” we saw in the stock. From the report:

“Valeant is operating what we believe is an unsustainable business model of serial acquisitions and underinvestment, fueled by debt, that will continue to lead to deterioration in the ongoing business.”

In October, the stock got hammered after Citron Research released its research note comparing the drug maker to Enron. Here's what Hedgeye Healthcare analyst Andrew Freedman had to say shortly afterwards:

“It was only a matter of time before Valeant’s debt-fueled acquisition binge would come to an end. If you look at what the underlying assets are worth and subtract the debt, you get an equity value that is closer to $20.

We spent the better part of six months researching Valeant, and there were no shortage of red flags. To name a few: Alternative pharmacy channels, inventory accounting on the Aesthetics assets, FDA investigations, price increases and questionable organic growth rates…

Trying to reconstruct the financials of Valeant’s business was near impossible given the acquisitions/divestitures and number of reclassifications… a huge part of the long thesis was a “Trust Me” story with management and that didn’t cut it with us.”

And then... Ackman came to the rescue! On that fateful October day, with VRX shares down as much as 20%, he rushed onto CNBC proclaiming to the world that he bought another 2 million shares. The stock bounced 10% the following hour.

But the story obviously doesn't end there.

Much of the recent VRX criticism has been focused on the drug maker's questionable relationship with the specialty pharmacy Philidor, which Valeant may have used to artificially inflate prices. Valeant has denied these allegations, but announced last week that it would sever its ties with Philidor, noting that Philidor accounted for only about 7% of its revenues.

Huh?

Here's Hedgeye CEO Keith McCullough today on the VRX “shenanigans.”

“There was a day when a $2.5B Hedge fund [position] blowing up was news. Ackman had a $2.5B position crash - and CNBC doesn't report it. This Ackman crash is going to ripple through the hedge fund community. They did everything, literally, to try to prop up $VRX - sucked little guys into buying it ... and Kaboom!”