“Truth is stranger than fiction, but it is because fiction is obliged to stick to possibilities. Truth isn't.”

-Mark Twain

The New York Federal Reserve’s Bill Dudley rocked the 2yr US Treasury Yield to the upside yesterday by suggesting that there is a “live possibility” that the Fed raises rates in December.

He provided the same caveat that Janet Yellen has guided markets to all year long. That, of course, is that America’s inaccurate forecasters at the Federal Reserve are “data dependent.”

That damn data, I tell you. If the US government simply didn’t report the data the Fed would have raised rates when they said they would (June). Instead, as markets discounted US GDP getting cut to 1.5% in Q3, the truth set accurate forecasters free.

Click here to join Hedgeye CEO Keith McCullough live on The Macro Show at 9am.

Back to the Global Macro Grind…

Ah, the possibilities of “green shoots” though – they remain. As does the effervescent hope that by year end stocks can’t go down because the Fed is back on hold.

Wait a minute – aren’t those conflicting possibilities?

Not to get caught up in the actual details or get in the way of any fictional story that may or may not be supported by one’s “company surveys”, our #process doesn’t leave room for cherry-picking data like our competitors do.

As my main man Darius Dale outlined in a note to Institutional Investors last night titled “Global Growth Has Not Bottomed”, we run a predictive tracking algorithm on every relevant data point from every relevant economy in the world.

The goal of this modern-day (math) macro #process is threefold:

- To contextualize sequential deltas (in data) as either ACCELERATING or DECELLERATING

- To contextualize immediate-term data within its intermediate-term TREND (accelerating or decelerating)

- To determine if the absolute value of the most recent data point (s) is at/near a probable mean reversion level

This is the precise process that called for US growth to accelerate coming out of the 2009 and 2012 lows inasmuch as it called for it to slow from the 2007-2008 and 2014-2015 #LateCycle highs. Our model is better than the Old Wall’s. And we don’t apologize for that.

As opposed to trying to write his own history, Ben Bernanke should have had the courage to act and apologize to Janet Yellen for not raising rates when US growth was accelerating in 2013.

Bernanke could have raised rates 4-6x by the time we hit US employment and consumption cycle highs of Q1 2015.

But he didn’t. And now, going on 78 months into a rate-of-change-slowing US economic expansion, Janet has the “live possibility” of making an even bigger mistake than not hiking into an acceleration – she could tighten into a slowdown!

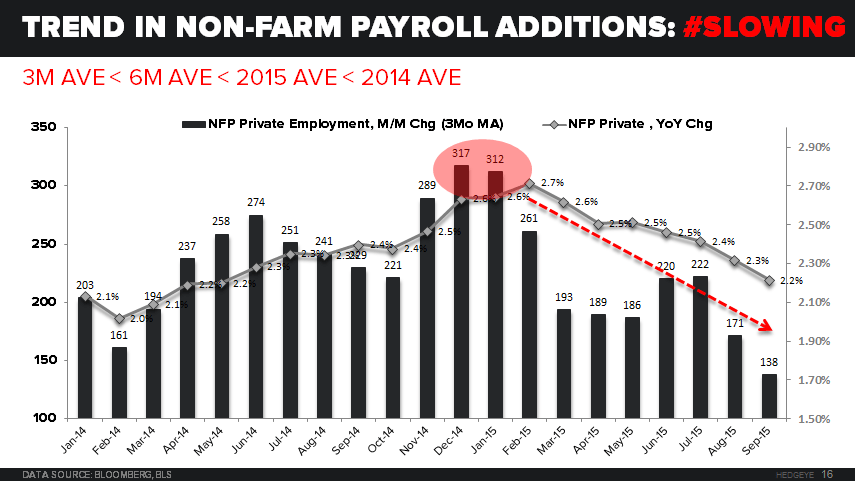

Unless tomorrow’s jobs report flashes something > 317,000, there’s not a hope on this side of centrally planned hell that the TREND in the US Labor Cycle goes from DECELERATING to accelerating.

While the probability of another #GrowthSlowing Non-Farm Payroll (NFP) print remains as high as it’s been since we started making the call that the US Labor Cycle peaked in Q1 of this year (see Chart of the Day with the DEC 2015 NFP top circled in red), what if the perma bulls paint it as “good”?

This is where the fiction of “good” can become very bad for macro markets. But, if you were looking at what happened in FICC (Fixed Income, Currencies, Commodities) yesterday instead of staring at Dow Bro 18,000’s possibility, you already know that.

- US Dollar ramped > 98 on the US Dollar Index

- Euro (vs. USD) got smoked down to $1.08

- CRB Commodities Index deflated -1.7% on the day, resuming its crash

And that, my friends, remains the live possibility you need to be very much prepared for – the possibility that, 7 years after the US driven financial crisis, that the Fed becomes the catalyst that perpetuates the next global one.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.98-2.28%

SPX 2029-2116

USD 97.21-98.24

EUR/USD 1.08-1.10

Oil (WTI) 42.96-48.23

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer