Our Macro team continues to question whether the recent equity market run-up is getting long in the tooth.

It was the same question Hedgeye Macro analyst Darius Dale posed back in July. (You remember how that ended in August.) Click the image below to read Dale’s previous note.

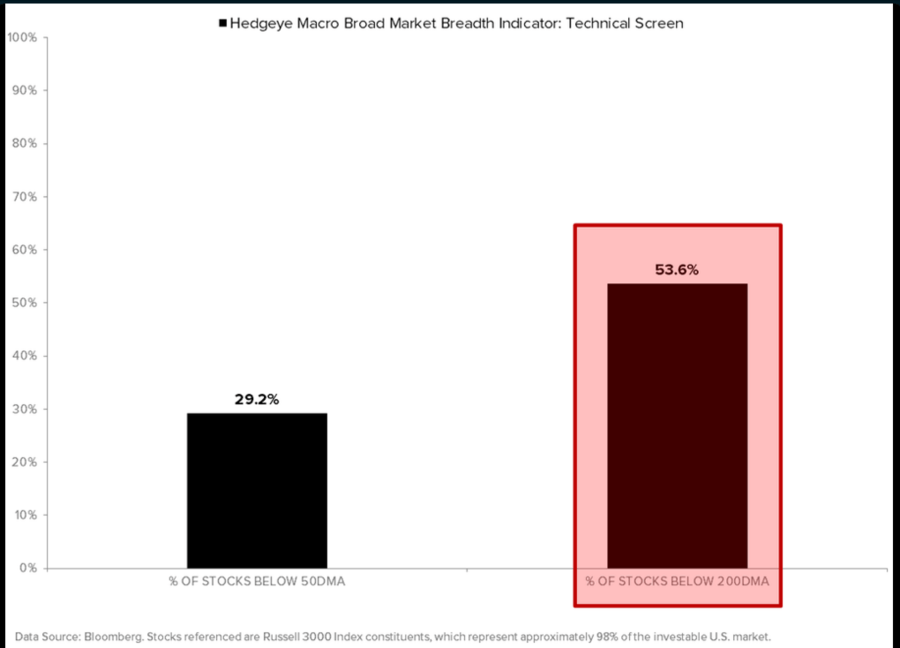

To update his previous research, Dale looked at the Russell 3000 (which is 98% of the investable public equity market) and, specifically, the percentage of stocks currently trading below their 200 day moving average to gauge the breadth of the market’s recent advance.

See the chart below which shows that 53.6% of stocks are below their 200-day moving average. To put that in perspective, back in May that reading was 39.1%.

As Dale notes:

“… While not useful as a [market] timing indicator, the aforementioned deterioration does imply the duration and scope for prospective returns are substantially worse than many investors may assume given consensus expectations for the length and strength of the current economic cycle…”