Bloomin’ Brands (BLMN) is on our Hedgeye Restaurants SHORT bench.

HEDGEYE OPINION

Last week we released a note on BLMN, previewing the quarter as well as introducing the STEAK TRACKER. Our core thesis on BLMN is that they need to divest non-core assets and focus on the core concept, Outback. This point was especially evident in this quarter as they lacked innovation and for the third year in a row rolled out a steak and unlimited shrimp promotion that did not resonate with consumers this time around. Traffic ended down -0.9% in the quarter for Outback, evidence that this lack of attention is not sustainable long-term.

During the call management spoke to sweeping remodels across the Outback system, renovating the exteriors of all stores over the next three years. The conviction in this initiative is the result of positive tests at 33 trial stores which showed 5% sales growth post remodel. Additionally, to our liking, management is focused on international growth. Outback Brazil had comp growth of 6.9% and Korea had traffic growth of 13.8% in 3Q15. BLMN is focused on investing “significant capital” in Brazil and looking for expansion opportunities across the world in areas such as the Middle East, China and Australia.

Even with this, we are still bearish on BLMN until they decide to divest non-core assets. Multi-concept casual dining restaurant companies in our eyes are destined to fail, as proper capital allocation is difficult to preserve.

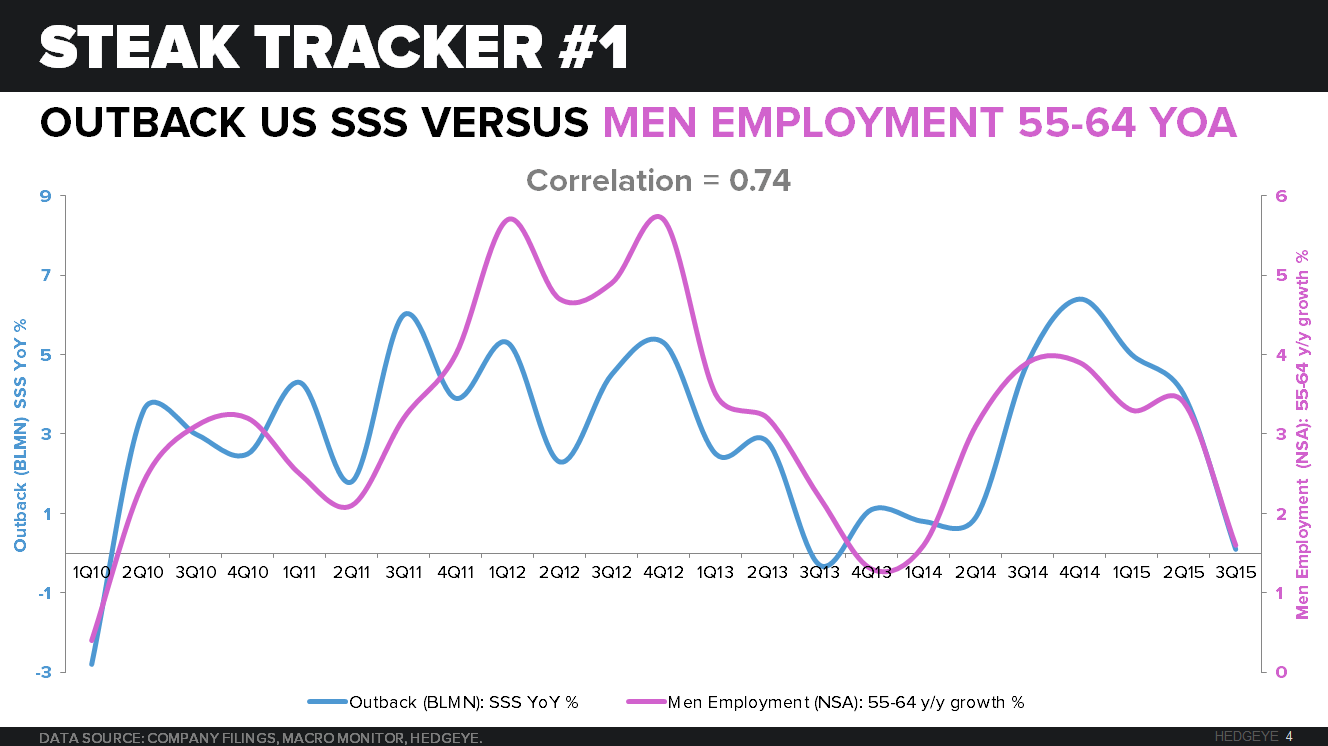

THE STEAK TRACKER

Outback SSS trend continued in line with what we were seeing in the steak tracker heading into the quarter. The correlation between Outback US SSS and Men Employment 55-64 YOA tightened in the quarter from 0.72 to 0.74. This specific tracker has been dependable in predicting the trend of Outback SSS and we continue to grow more confident in it.

Our other trackers, the more long term in nature, CPI – Uncooked Beef Steak and CPI – Beef and Veal, held up well. Although, the correlation decreased slightly, we are using them for trends not quarterly ebb and flows and those remained accurate.

3Q15 FINANCIAL RESULTS

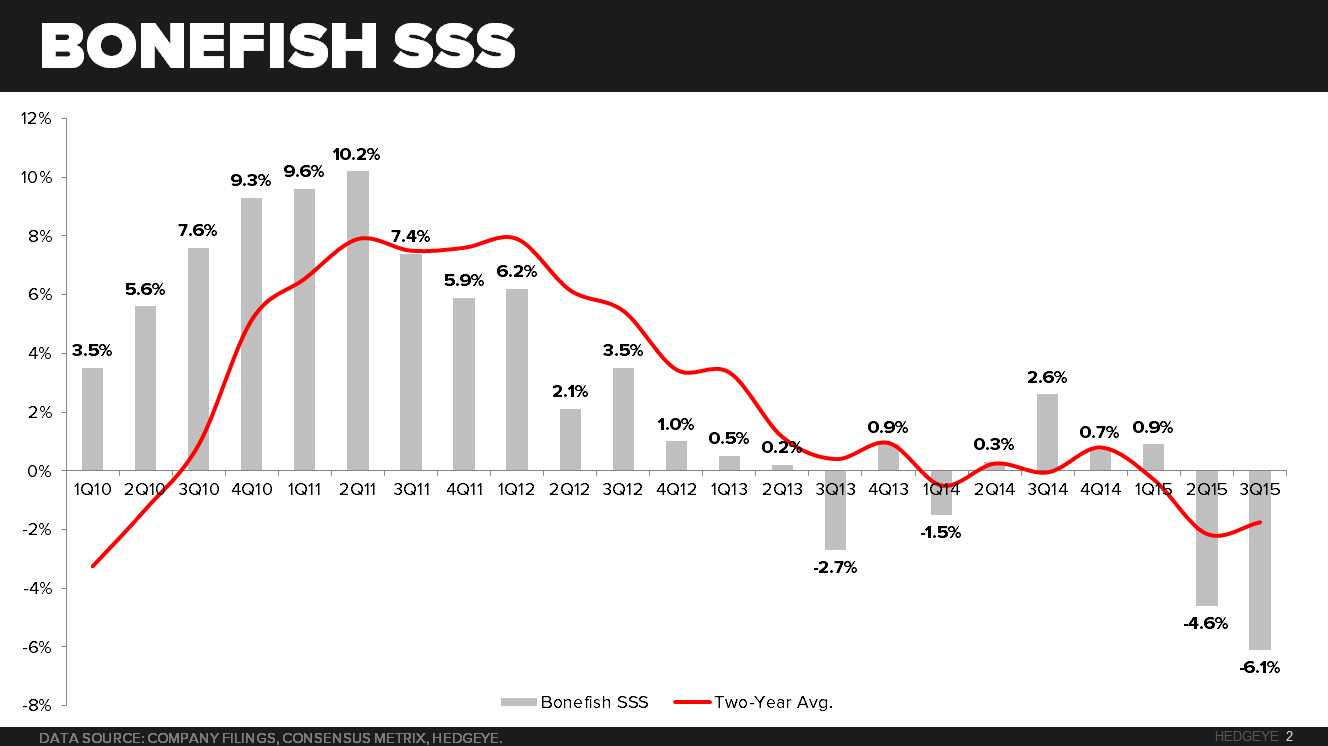

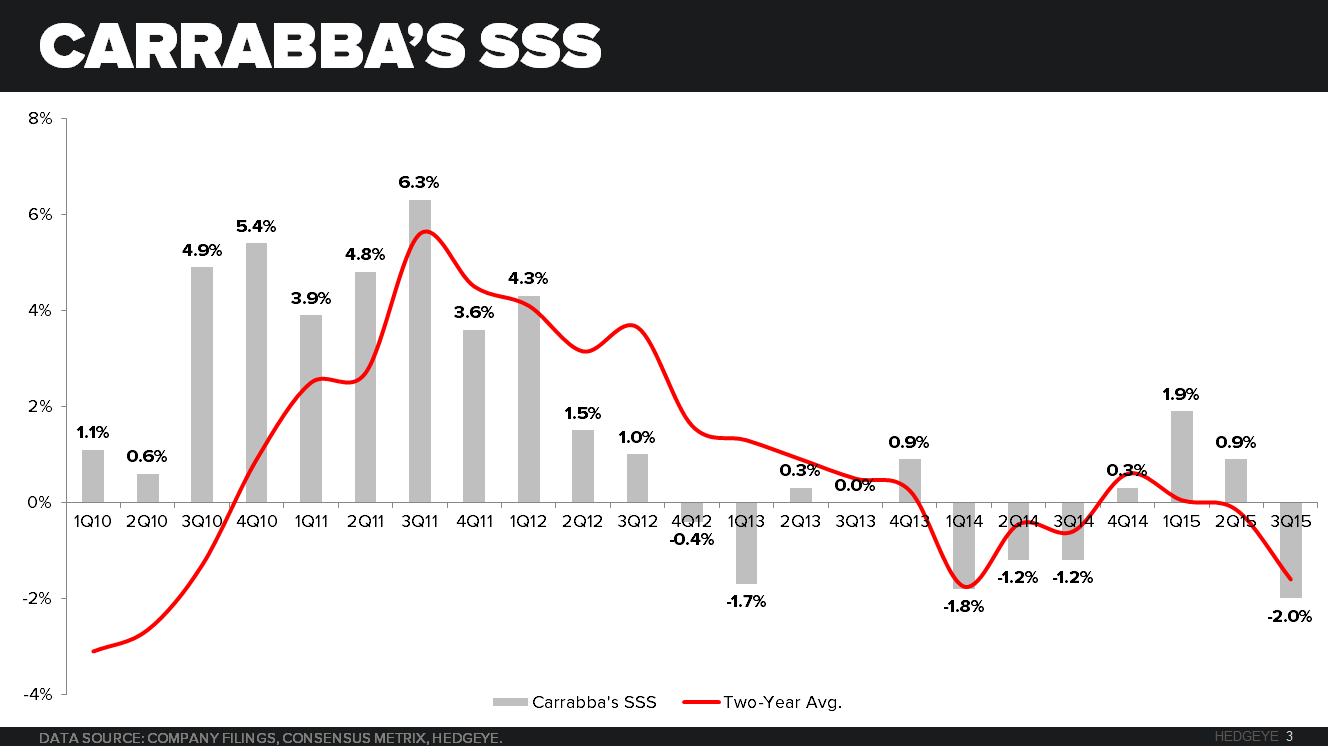

BLMN reported revenue declined 3.6% YoY to $1,027mm versus consensus estimates of $1,035mm. The top line miss was driven by bad same-store sales growth for all concepts. Outback US SSS increased 0.1% versus consensus estimates of 1.7%, a 470bps YoY decline. Bonefish reported SSS of -6.1%, 80 bps below consensus estimates of -5.3% and a 870bps decline YoY. Carrabba’s SSS came in at -2.0%, 310bps below consensus estimates of 1.1% and representing an 80bps decline YoY. Restaurant level operating margins improved 70bps in the quarter to 14.5% in-line with consensus estimates. Moving to the bottom-line BLMN was able to translate a top-line miss into a bottom-line beat, reporting EPS of $0.15 versus consensus estimates of $0.14.

MANAGEMENT GUIDANCE

Management reaffirmed full year EPS guidance of at least $1.27. The company revised blended US comp growth to be 0.5% to 1.0% versus prior guidance of “approximately 1.5%”. Total revenue guidance was shaved slightly, to approximately $4.37bn down from approximately $4.43bn.

Looking to FY2016, management expects EPS growth of 10% to 15%, with positive SSS in the U.S. Additionally management is calling for commodity basket inflation of approximately 1%. This number is variable depending on how beef shakes out through the course of the year.

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst