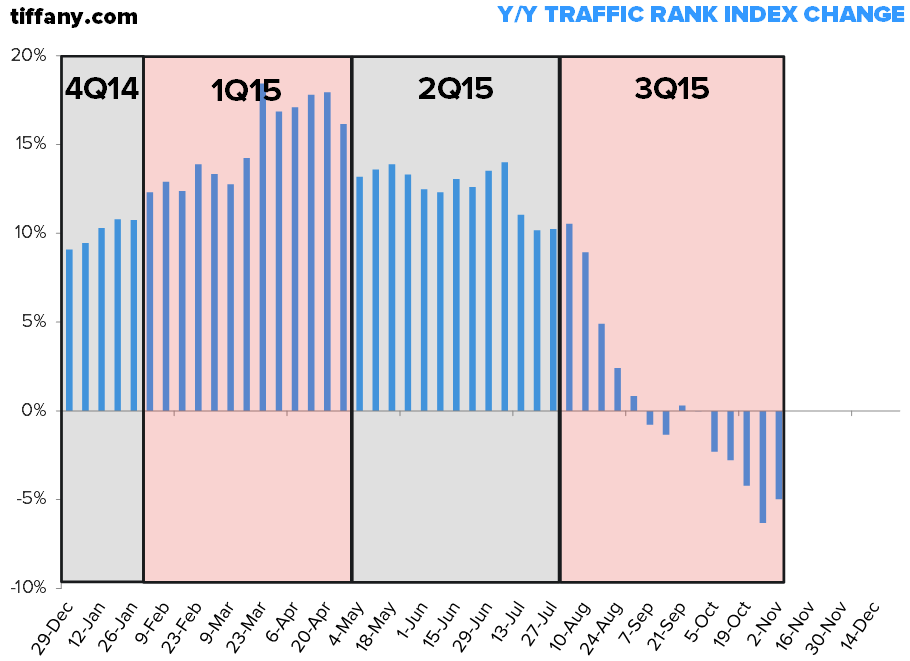

TIF - E-comm Traffic Trends Decelerate in 3Q

TIF just closed the books on 3Q, and the traffic trends headed out of the quarter look particularly weak. E-commerce accounts for just 6% of total sales for the company -- but because the average ticket for TIF sits at $750 there is a lot less impulse and a lot more planning before a consumer slaps down a credit card and walks away with a blue box. The metric, which looks at the relative strength of an e-commerce site relative to the internet in aggregate takes into account two metrics (unique visitation and page visits per user), decelerated from +10% YY at the end of the 2nd quarter to -5% at the end of 3Q with marked softness throughout the quarter.

Not a good barometer for brand strength in 3Q, especially when the common perception seems to be that “just because Tiffany (TIF) blew up earlier this year, it can’t blow up again.” We disagree. It actually blew up twice this year. And we think there will be another. Next year's estimates are sitting at $4.54. We think an optimistic number is $4.25. If our Macro team's bearish call plays out according to plan, TIF will be lucky to earn $4.00.

With productivity, margins and returns all near 10-year highs, and the stock trading at 19x a number we don't think is doable, we still like this one on the short side.

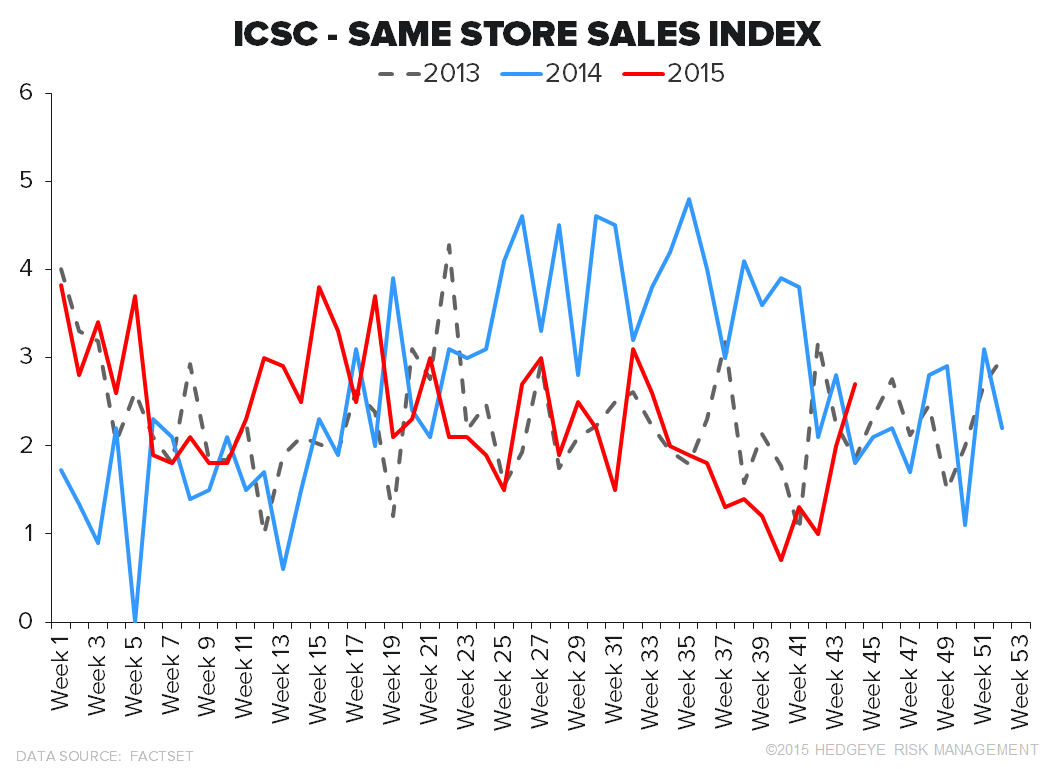

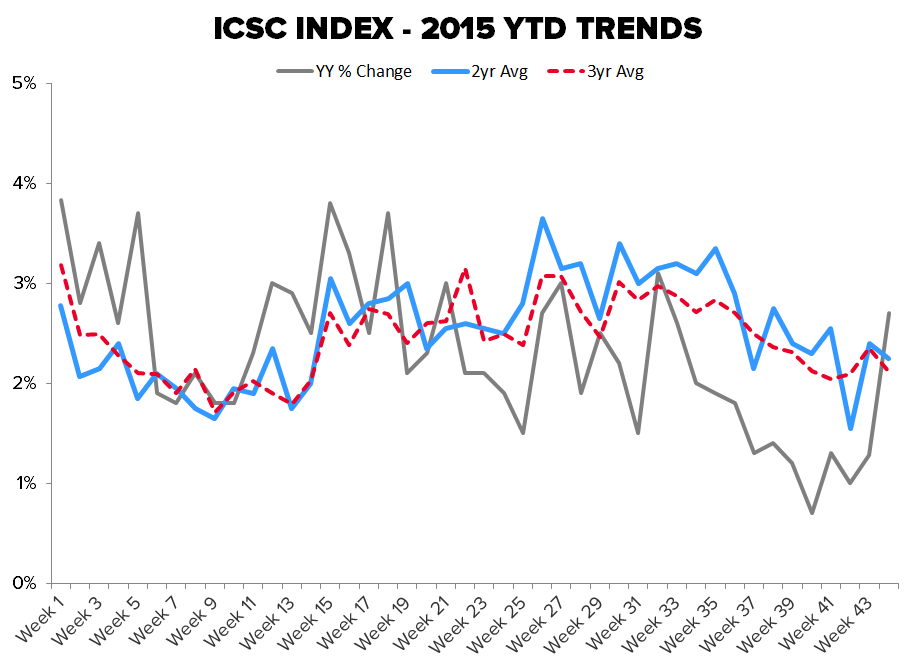

RETAIL sales Trends (ICSC / RedBook) - a rare spike in both indices, which happened on the same day LB put up a big comp (3Q at ~7% vs 5% expectations). On the heels of a lot of negative sentiment around retail, this offers up a 1-day reprieve. Note, however, that comps are very easy through most of November -- until Black Friday and December, which is what really matters.

LB - L Brands Reports Oct. Comp #s, Takes Up 3Q Ahead Of Investor Day

(http://phx.corporate-ir.net/phoenix.zhtml?c=94854&p=RssLanding&cat=news&id=2105541)

DLTR - Dollar Tree completes sale of 330 Family Dollar stores to Sycamore Partners. Stores to be branded Dollar Express.

(http://www.dollartreeinfo.com/investors/global/releasedetail.cfm?ReleaseID=939816)

AMZN - Amazon bookstore opening in University Village. The 5500 SqFt store will carry 5000-6000 titles.

AEO - American Eagle Outfitters acquiring Tailgate Clothing Company for $11mm, takes up 3Q guidance.

GNC - GNC expects to repurchase an additional $200mm shares by year end, raising guidance 2 cents to include the impact.

(http://phx.corporate-ir.net/phoenix.zhtml?c=88669&p=irol-newsArticle&ID=2105684)

EBAY - eBay Enterprise Sold Off and Broken Up

(http://www.ecommercebytes.com/cab/abn/y15/m11/i03/s04)

99 Cents Only announced Felicia Thornton has been appointed as its CFO and treasurer

(http://www.chainstoreage.com/article/-cents-only-stores-has-new-cfo)

SHLD - Sears enters online home services market

(http://www.chainstoreage.com/article/sears-enters-online-home-services-market)

BONT - Bon-Ton Stores Announces Extension of Private Label Credit Card Agreement With Alliance Data's Card Services Business

(http://investors.bonton.com/releasedetail.cfm?ReleaseID=939995)

GCO - Genesco To Acquire Little Burgundy Chain From The Aldo Group

(http://phx.corporate-ir.net/mobile.view?c=75042&v=203&d=1&id=2105697)

Sports Authority Launches New Fitness Training App

(http://footwearnews.com/2015/focus/athletic-outdoor/sports-authority-new-bodyfit-fitness-app-167141/)

Selfridges Buys Arnotts Department Store in Dublin