Takeaway: If you’re the band Europe, you sing The Final Countdown, it’s what you do. If you’re an economic cycle, you cycle. Income & Consumption Growth are now past peak.

Reading through consensus economist reactions to yesterday’s advance GDP release for 3Q, the basic, collective conclusion was this:

Bad: Global Headwinds, Energy and broader Industrial Sector Activity

vs.

Good: Continued strength in domestic, private sector demand

Right ... But Also Wrong: That conclusion isn’t inaccurate. Consumption was again good on an absolute basis (we knew that ahead of the GDP print) while export and industrial activity continued to flag (also a known-known).

Indeed, looking at Real Final Sales or Real Final Sales to Domestic Purchasers – which strips out exports and inventories and is meant to be a cleaner read on underlying domestic, private sector demand – the numbers remained solid (but decelerating) and better than the headline.

REMEMBER, IT'S ABOUT BETTER/WORSE: The liability in taking an absolutist view of the data is that macro trades on better/worse, not good/bad.

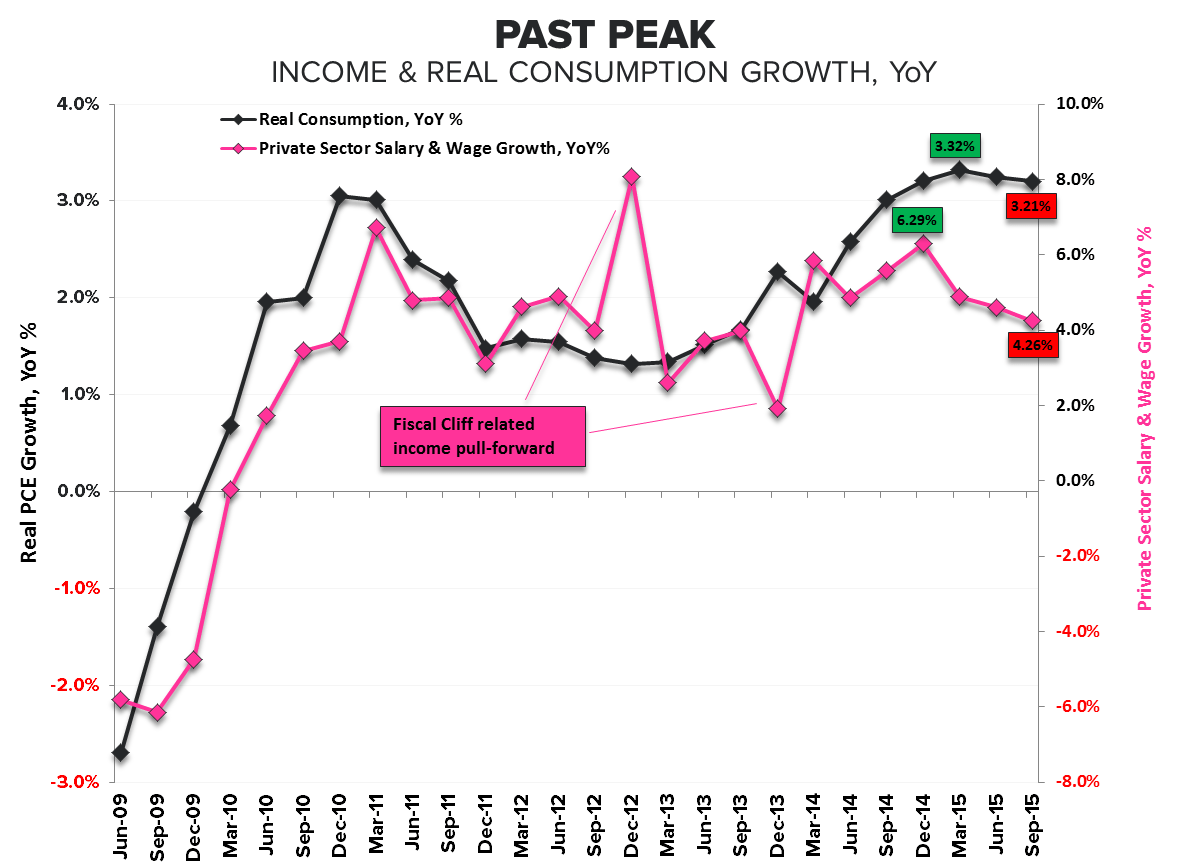

As we highlighted (again) in our latest quarterly themes deck, Consumption growth peaked in 1Q15 and the slope of the line has now been negative for two quarters. In employing a rate-of-change-centric view of the data, going from great-to-good is bad – or should at least serve as a red flag.

In our modern consumption economy where household spending accounts for ~69% of GDP and the balance of expenditure buckets are in retreat, negative 2nd derivative trends in the singular source of demand strength are not inconsequential.

So, can the domestic consumption train re-accelerate?

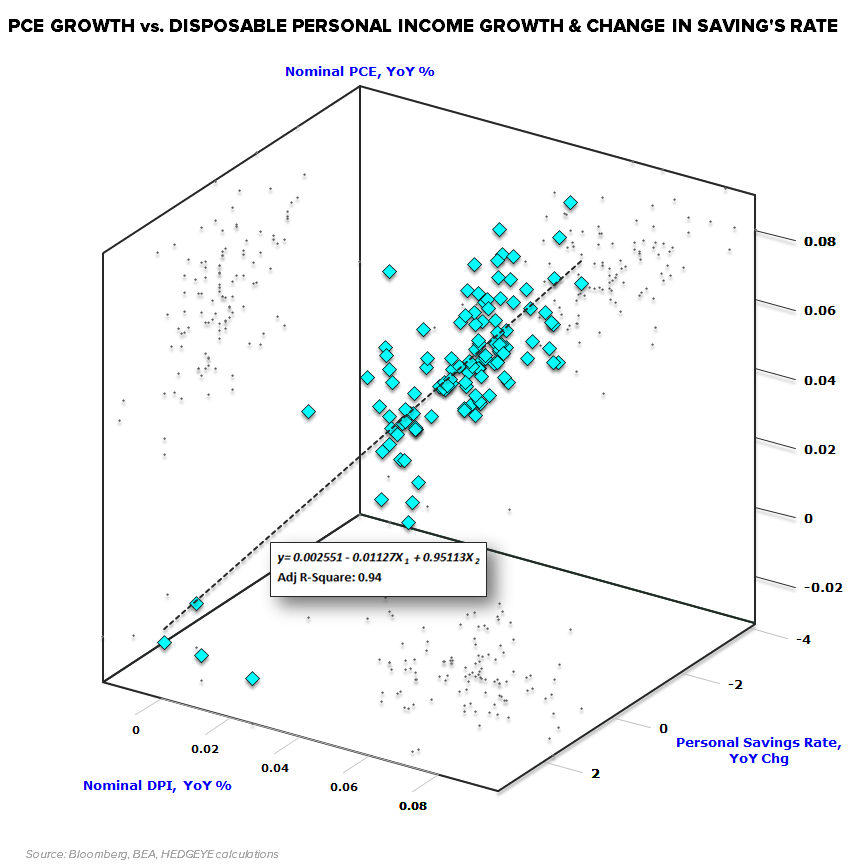

DON'T OVERTHINK IT: Broadly speaking, the drivers of Consumption aren’t overly complicated. In short, consumer spending growth is a function of the growth in income, the marginal propensity to consume or save that income, and the net change in household credit.

Together, growth in disposable income and the change in the savings rate explain most of the change in nominal consumption (PCE) growth. Indeed, over the last 30+ years, the multiple regression between PCE growth vs. nominal Disposable Income growth and the change in the Savings Rate produces an R-squared >0.94.

Because its convenient (and largely agrees with the data), let’s assume both credit growth and the savings rate stay largely static from here and income growth remains the predominate driver of spending growth. In other words, the forward slope of income growth determines the path of consumption growth.

INCOME GROWTH | THE OUTLOOK: This morning we got the detailed household income and spending data for September. Decelerating growth in aggregate hours and flat wage growth in the September employment report translated into a deceleration in income growth.

Aggregate private sector salary and wage growth decelerated to +3.8% YoY – a -50bps deceleration relative to August and well below the TTM pace of +5.1%. Indeed, aggregate private sector income actually declined -11bps month-over-month.

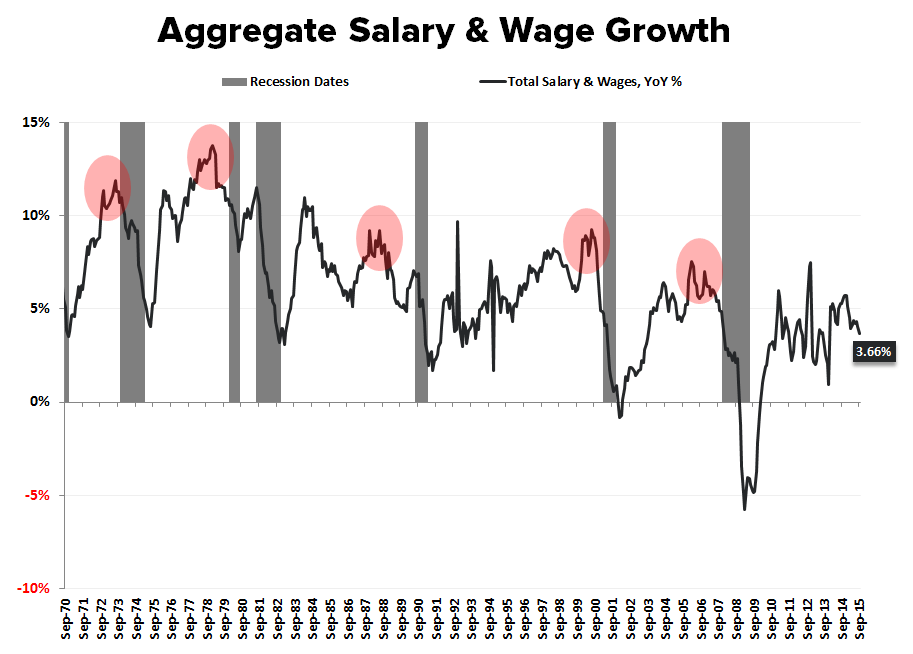

Given the slowing trend in payrolls and progressively steeper income and consumption comps, it looks increasingly likely that aggregate income growth is now past peak as well.

If you’re the band Europe, you sing The Final Countdown, it’s what you do. If you’re an economic cycle, you cycle.

Is a recession immediately imminent … the balance of lead labor market data doesn’t suggest that, but we are in the twilight of the current expansionary cycle and the slope of the line across a growing number of indicators has gone negative.

Our annotated summary table along with the longer-term income & consumption cycle charts are below.

Enjoy the weekend.

Christian B. Drake

@HedgeyeUSA