Claims are maintaining steady strength below 330k, rising by just 1k last week to 260k. However, even with claims now marking their 20th month below the 330k level, the Federal Reserve once again held the Fed Funds rate flat at zero yesterday. Last week, as we show in the chart below, we pointed out that this delay in a rate increase appears to be different versus previous cycles. Historically, by now the Fed would already be well underway raising rates. This is one of the arguments put forward by bulls for why the current cycle may not yet be long in the tooth.

The reality, however, is that the Fed has actually been tightening policy since December 2013 when it began tapering QE3. Interestingly, as Christian Drake of our Macro Team pointed out, the Fed actually quantifies the effect of the current cycle's non-traditional policy action and the tapering thereof in the chart below with a measure called the Wu-Xia Shadow Fed Funds Rate (HERE). The Shadow Rate is basically the rate the Fed has set by implementing non-traditional policies. The following chart shows that we have been in a rising rate environment since April, 2014 and the effective Fed Funds rate has risen ~225 bps to -0.75% from -3%. This is one of the main reasons why a) growth is now slowing and b) the cycyle is, in fact, very late stage.

On the energy front, claims in energy states continue to worsen versus the country as a whole as we approach the end of the year around which point many energy firms' hedges will roll over. The chart below shows that in the week ending October 17, the spread between the indexed series of energy state claims and country-wide claims widened to 22 from 20 in the prior week.

The Data

Initial jobless claims rose 1k to 260k from 259k WoW. The prior week's number was not revised. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -4k WoW to 259.25k.

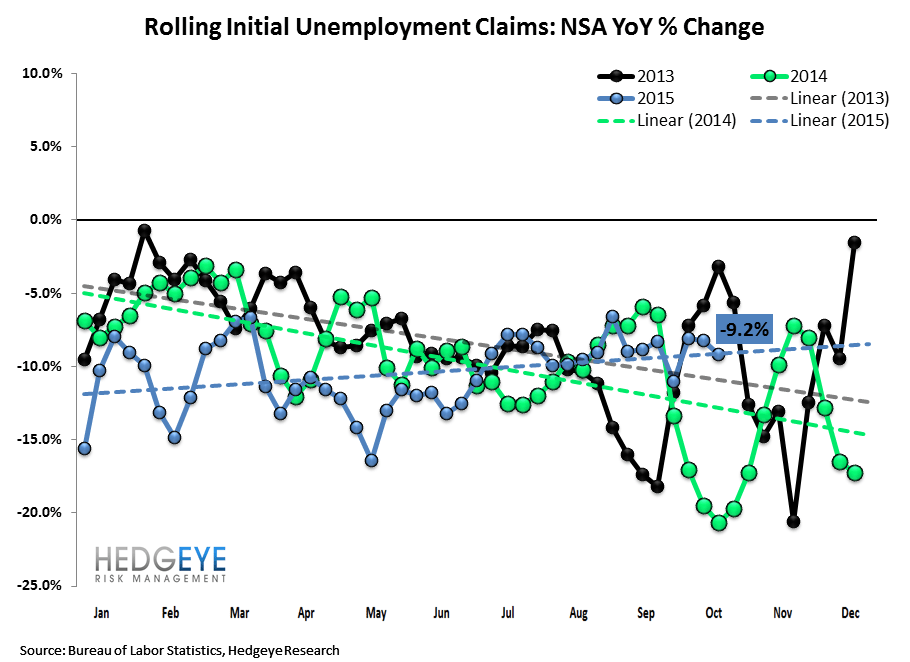

The 4-week rolling average of NSA claims, another way of evaluating the data, was -9.2% lower YoY, which is a sequential improvement versus the previous week's YoY change of -8.2%

Yield Spreads

The 2-10 spread rose 1 basis points WoW to 141 bps. 4Q15TD, the 2-10 spread is averaging 143 bps, which is lower by -10 bps relative to 3Q15.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT