HEDGEYE COMMENTARY

Buffalo Wild Wings (BWLD) is on the SHORT bench and will remain there. We made a big SHORT call last quarter that did not work out. This business is all about timing.

Our concerns have been focused on increasing labor costs and slowing same-store sales trends. The company has been aggressively raising prices over the last year to mitigate the pressure from an increase in labor costs. Ultimately, that will impact traffic trends and we may be seeing that now. Traffic in 4Q15 is currently flat to negative, but the company expects traffic to turn positive again in 2016.

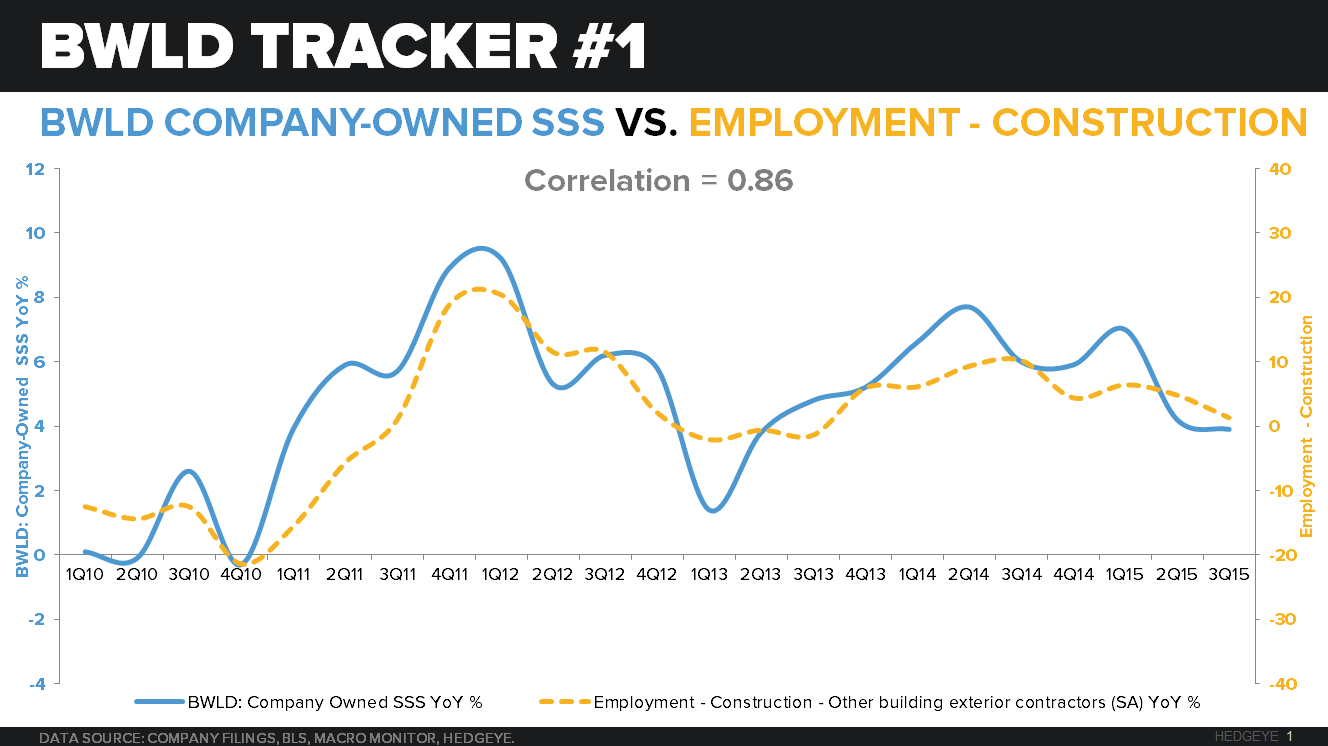

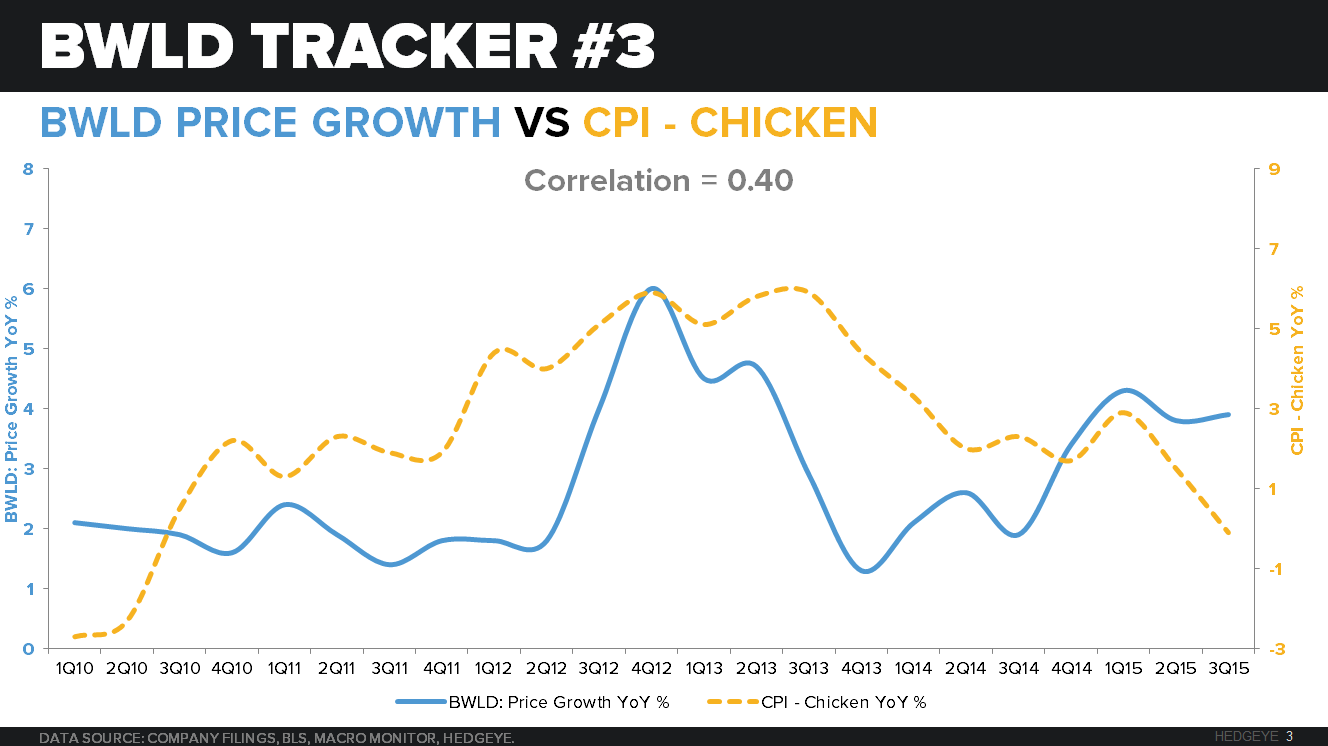

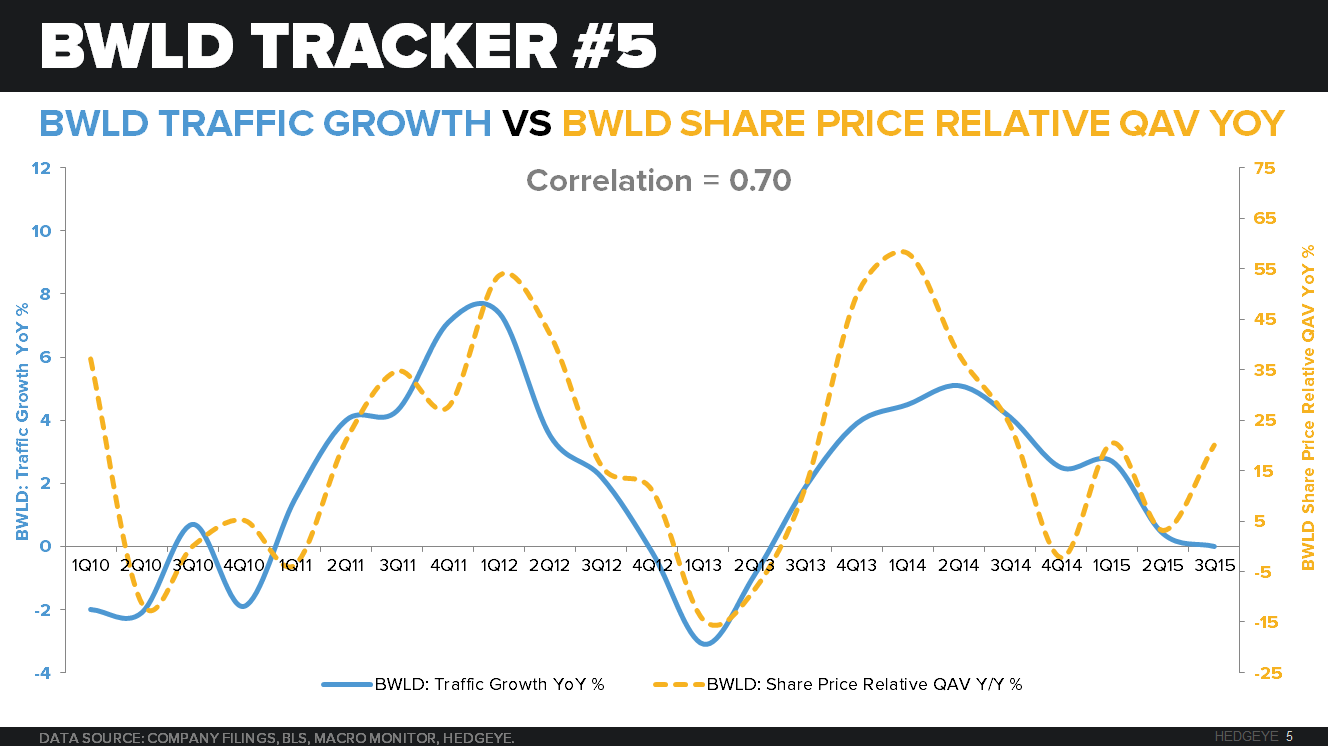

BWLD is not immune from slowing industry trends that we are currently seeing play out in the space. Specifically to BWLD, the Hedgeye Macro Monitor is highlighting four charts that suggest slowing same-store sales trends are not a one quarter phenomena for BWLD. Additionally, you can see that the company stock price is closely tied to traffic trends.

1. A core demographic, construction workers, jobs are slowing which suggest slower traffic trends for the company:

2. Employment in the Leisure and hospitality space has slowed:

3. The company is aggressively raising prices above inflation, although not a strong correlation historically, in the last four quarters BWLD has priced above CPI – Chicken. Prior to this time period they were only above this metric once in the last 17 quarters:

4. Aggressive price increases will not be sustainable in a slowing consumer confidence environment:

5. Traffic vs QAV YoY:

MANAGEMENT COMMENTS

- BWLD earnings in 3Q15 declined 11.6% to $19.2 million or diluted EPS of $1.00 vs $1.14 last year.

- For the first four weeks of 4Q15, same-store sales are trending at about 2.8% at company-owned restaurants and 0.8% at franchised locations. This compares to last year 5.4% at company-owned restaurants and 5.1% at franchised locations.

- Halloween is on a Saturday compared to a Friday last year and the Christmas holiday is on a Friday versus a Thursday last year, both of which we anticipate as a negative for same-store sales.

- A menu price increase of 2.2% is scheduled to take effect on November 2nd, bringing the total menu price in 4Q15 to 4.1% in fourth quarter.

- The cost for traditional chicken wings for the first two months of the fourth quarter averaged $1.80 vs the average cost for the full fourth quarter last year of $1.90 per pound.

- In 4Q15 Labor costs are expected to be approximately 31%.

- In 3Q15 BWLD spent $160 million to acquire 41 franchised locations in Texas, New Mexico and Hawaii, which includes two restaurants under development.

- The incremental costs to acquire the restaurants had a negative $0.13 impact on EPS.

- BWLD has increased company-owned Buffalo Wild Wings locations by 24% YoY.

- Same-store sales in 3Q15 increased 3.9% at company-owned restaurants and 1.2% at franchised locations

- One less week of football and fewer pay-per-view events than last year negatively impacted same-store sales by 80 basis points.

- Established affinity program for Buffalo Wild Wings - Blazin' Rewards loyalty program launched in September.

- Blazin' Rewards is currently at 50 restaurants in five pilot markets.

- Building its international presence through franchising - franchisee in the Middle East opened a location in Dubai in September and a second location in the Kingdom of Saudi Arabia in October. There are currently 13 international Buffalo Wild Wings in Mexico, the Philippines, the Kingdom of Saudi Arabia, and the United Arab Emirates.

- In 2016, new markets are Panama and India. In total, international franchisees are expecting to open 15 restaurants next year.

- Continue to invest into additional concepts – R Taco - shortened the name from Rusty Taco and created a new logo for the brand. Franchisees of R Tacos expanding in three markets and expected to launch a more aggressive franchise sales strategy.

- PizzaRev continues its company-owned and franchise development. There are currently 29 locations in five states and franchise locations in Nevada, New York, and Ohio are opening soon.

FINANCIALS

- 3Q15 revenues totaled $455.5 million, up 22%. Company-owned restaurant sales for the third quarter increased to $431.8 million, up 23.2%.

- System-wide sales were $897.3 million, an increase of 10.5% over the third quarter of 2014.

- 3Q15 same-store sales, at company-owned stores increased 3.9% vs 6% last year. Average weekly sales increased by 3.7%

- Menu price increases at company-owned restaurants was 3.9%.

- BWLD operated a 109 additional company-owned Buffalo Wild Wings in 3Q15, up 24% unit increase.

- Our royalty and franchise fee revenue for the third quarter grew 3.6% to $23.8 million versus $22.9 million last year even with 18 less franchised Buffalo Wild Wings units in operation at the end of the third quarter versus a year ago.

- Same-store sales at franchised Buffalo Wild Wings locations increased by 1.2% compared to a 5.7% increase in third quarter last year. Franchised average weekly sales volumes at Buffalo Wild Wings locations in the United States for the quarter increased by 2%, 80 basis points higher compared to the same-store sales percentage.

- Cost of sales for the third quarter was 29.4% of restaurant sales compared to 29.1% in third quarter last year, a 30-basis-point increase.

- Wings were $1.79 per pound in 3Q15, or 19% higher than last year's average of $1.50.

- Traditional and boneless wings reached 21% of restaurant sales flat YoY

- Cost of labor for the third quarter was 32.2%, up 20 basis points YoY. Health insurance and workers' compensation expenses were the primary drivers of the year-over-year increase. We continue to see wage pressure in our restaurants.

- We estimate that the transition of the 41 unit franchise acquisition had a negative 10 basis point impact on labor as a percentage of

- In 3Q15, restaurant operating expenses were 14.7%, a decrease of 30bps YoY driven by lower advertising cost per restaurant partially offset by increased repairs and maintenance expense related to the acquisition.

- In summary, restaurant level cash flow 18.2% vs 18.4% last year. This decrease in cash flow is primarily a result of the higher traditional wing cost and increased labor as a percentage of restaurant sales.

- General and administrative expenses were $33.7 million in the third quarter, or 7.4% of total revenue, compared to $27.8 million, also 7.4% in the prior year.

- Excluding stock-based compensation of $4.5 million in the third quarter and $2.6 million in the prior year, G&A expenses for the third quarter would have totaled $29.3 million or 6.4% of total revenue compared to 6.7% last year. Third quarter G&A expense was aided by a $500,000 loss on deferred compensation investments.

- Opened seven new company owned Buffalo Wild Wings during the quarter. This compares to nine new Buffalo Wild Wings and one PizzaRev location opened in the third quarter of 2014.

- Preopening costs for company-owned Buffalo Wild Wings averaged $253,000 per new restaurant during the quarter, compared to $314,000 in the third quarter last year.

- The effective tax rate in 3Q15 was 30.1% vs 26.9% in the prior year. The effective tax rate in 2015 will be about 32%

- On our balance sheet on September 27, 2015, our cash, cash equivalents, and marketable securities totaled $20.2 million, compared to $112.9 million at the end of 2014. Our unsecured line of credit had a balance of $47 million as of the end of the quarter.

- Cash flow from operations was $66 million and cap ex was $56.9. 2015 capital spending will be $378 million, including the $210 million spent to acquire franchise locations.

IMPORTANT COMMENTS FROM THE Q&A

“I would say that the top line revenue is the primary contributor to our reduced guidance for 2015.”

“If we can achieve comp store sales in excess of our price increase, we'd be happy at least for the fourth quarter of 2015.”

“That's what we are modeling, yes.” (Expect positive traffic in 2016)

“As you look at the back half of the year, there is not a lot favorable happening to the events calendar on a year-over-year basis which would cause us to anticipate particularly high same-store sales. And again, if you look at the market as a whole, I think there has been a same-store sales softening and we do tend to flow with the market, although outperforming”

“With the stores that are in Texas, Nevada and Hawaii, there is a handful of stores that are being affected by the downturn in the oil industry”

“So I think we are taking a cautious look on 2016 right now, exceeding 20% is very doable”

“Well, I'll walk through the menu price increase that will be in effect next year quarter by quarter after we get the November price increase in our stores. So, first quarter next year would go to 3.1%, Q2 would be 3% and then it would roll down to 2.6% in the third quarter next year and then down to 0.9% in fourth quarter.”

“So, we think on a year-over-year basis, we will have a lower average price per pound for wings in 2016 than we did in 2015”

“And we did raise our line of credit to $200 million. So we are open to debt on our balance sheet. We have conversations with our board of directors regularly and I'm sure it will be a topic at the next board of directors meeting to talk again about capital allocation and structure for the future.”

“But the – on traffic we are not – I think when you adjust for events that aren't matching year-over-year, we are not suggesting we are seeing negative traffic.”

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst