“If there is any period one would desire to be born in, is it not in the age of Revolution?”

-Ralph Waldo Emerson

Emerson was a 19th century essayist and poet from Boston, MA best known for leading what they called the “Transcendentalist” movement. It was a New Englander thing that probably resonates with many Americans (and other humans who think for themselves) today.

Transcendalists believed that “institutions ultimately corrupted the purity of the individual.” They believed people were at their best when they were “self-reliant” and able to think independently of government and its propaganda.

That’s why the aforementioned passage from Emerson is such a progressive one. On revolution against the Establishment, it’s a time “when the old and the new stand side by side… when the glories of the old can be compensated by the rich possibilities of the new era.”

Back to the Global Macro Grind…

At this stage of the Fed’s forecasting game, I don’t hope that you see the mediocrity in this un-elected institution that decides the fate of what used to be free-market moneys every day. Instead, I pray that you understand the risks associated with their market moving forecasts.

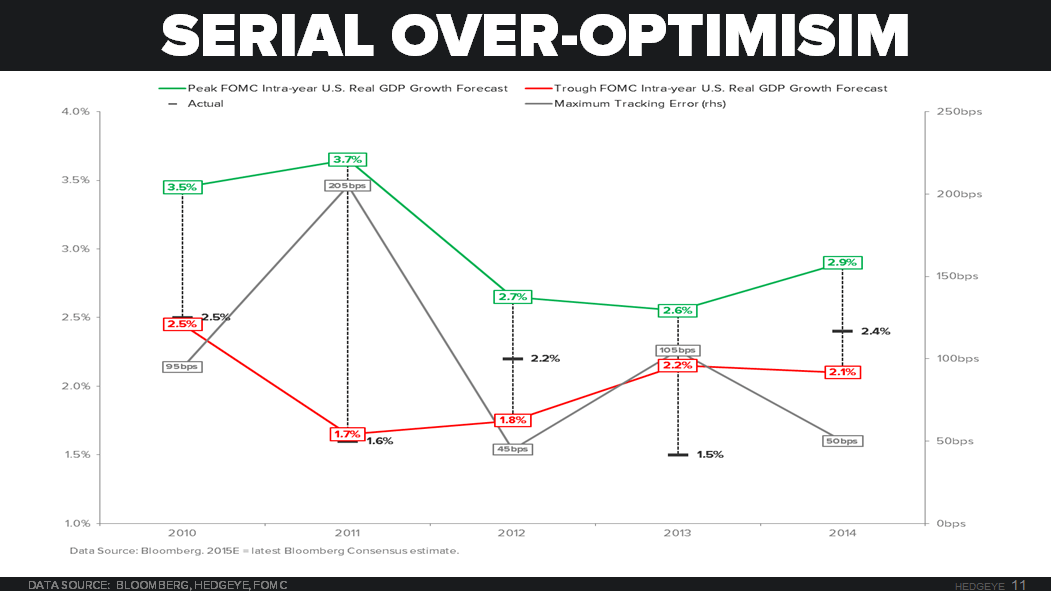

As you can see in today’s Chart of The Day, “Serial Over-Optimism”, the US Federal Reserve has overestimated US GDP growth by approximately 100 basis points every year since Ben Bernanke had the courage to act on economic models that don’t work.

What’s 100 basis points?

- Uh, the difference between 1% and 2% GDP growth

- The Difference between a 10yr Bond Yield of 2.0% and 3.0%

I know. I know. Let’s not get caught up in the details.

Instead, after the almighty Fed changed their forecast, albeit subtly, yesterday – let’s analyze where the Fed could be wrong (again):

- In the side by side statement (OCT vs SEP), the Fed removed the bearish concerns about the Global Economy and…

- Added the latest concerns (#LateCycle US Employment) embedded in the most recent US jobs reports slowing

This, of course, comes:

A) After the US Dollar stopped going up AFTER the slowing US jobs report (that they didn’t forecast) and…

B) Countries, Currencies, and Commodities took a break from crashing, for 3 weeks

So, after dynamically adjusting their latest forecast for everything they missed calling for to begin with:

- The US Dollar and interest rates went straight back UP again yesterday

- And everything Global #Deflation is falling in Country, Currency, and Commodity land this morning

Yep. Look at the overnight reaction to a more “hawkish” Fed:

- Australian Stocks (levered to Commodity #Deflation) down -1.3%

- Indonesian Stocks (levered to EM and FX risk) down -3.0%

- Russian Stocks (levered to Oil #Deflation) down -2.1%

*hint: the world’s leverage bubble (including inflation expectations) is denominated in Dollars

Oh, and after, “rates ripped” (5 basis points on the 10yr) on the Fed’s latest proclamation of lagging indicator faith, Bond Yields, globally, are falling (again) this morning ahead of another slowing US GDP report.

So, what if the Fed’s US domestic admission of #GrowthSlowing continues to be “data” driven like it has this week (New Home Sales, Durable Goods, and Consumer Confidence reports all slowed, again, sequentially) and the US Dollar rises as rates fall?

Oh, boy. That is the mother of all #Deflation Risk signals. So stand ready, side by side. Because the biggest risk of this entire “600 rate cuts globally” experiment is already here. It’s the Fed’s forecast that could very well perpetuate the next market crisis.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.99-2.11%

SPX 2004-2099

RUT 1136--1182

USD 96.02-98.63

EUR/USD 1.08-1.11

Oil (WTI) 42.97-47.32

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer