KEY POINTS

- DISPLAY HEADFAKE INDEED: We thought this might be a remote possibility, but should have known better with this mgmt team. The source of the 3Q beat was entirely Brand Advertising (aka Display); it missed everywhere else. Note that YELP annouced on its last call that is planning to shutter that segment by year end, and also provided 2H15 Display revenue guidance of $10M (tranlated to -56% y/y decline vs. -8% in 1H15). YELP actually produced $9M in Display revenue in 3Q15 alone, which was as acceleration in growth from 2Q15 levels. YELP also refused to provide an update to Display Guidance for 4Q15. So the only reason why YELP was able to guide inline for 4Q was because it sandbagged 2H15 Display guidance on the 2Q release, which consensus baked into 4Q estimates...Great quarter guys.

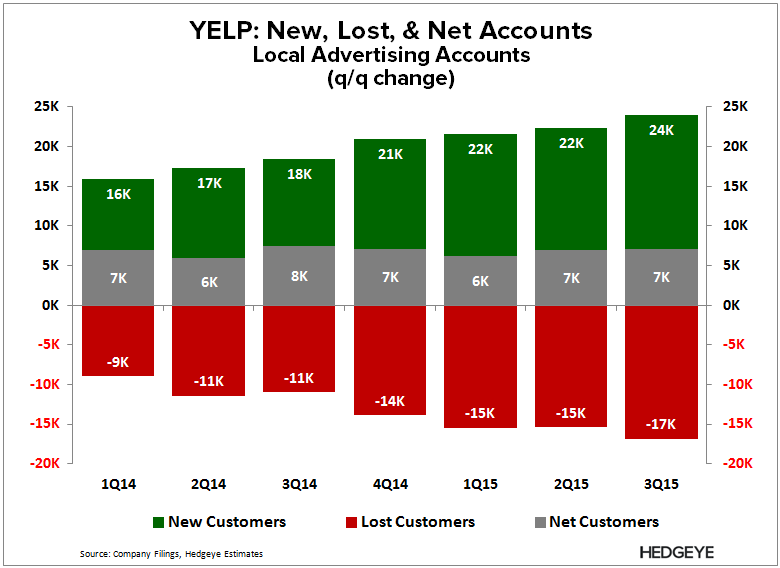

- DETERIORATION AT THE CORE: YELP has missed consensus Local Ad revenue estimates for the past last 3 quarters. While YELP was able to essentially maintain both new LAA growth and attrition rates at 2Q levels, Local Ad revenue growth still decelerated to 36% from 43% in 2Q15 (vs. 51% in 1Q15, and 60% in 4Q14). That’s because attrition is exerting more pressure across its model. The more accounts YELP enters any period with, the more it will lose, and the more brand new accounts (and sales reps) it needs compensate. The one positive is that YELP was able to ramp its salesforce to plan in 3Q (+35% y/y), but its still struggling to drive new account growth in excess of the rate that it's hiring reps.

- NOW WHAT? We'll be monitoring consensus estimates from here since the 2016 guidance release remains our next short catalyst. As it stands now, YELP would need to maintain its new LAA growth rate from now through the end of 2016 with historically low attrition rates in order to hit consensus Local Ad Revenue estimates. But we're not expecting YELP's Display headfake to completely evade the sell-side; especially since mgmt dodged two direct questions on the matter. That said, there's a chance the sell-side may disproportionately cut 2016 Local Ad estimates off this print, which could accelerate an exit on our short position, albeit temporary since YELP remains a secular short until it blows up its model.

Let us know if you have any questions, or would like to discuss further.