Twitter’s long-term growth prospects look increasingly suspect. Shareholders learned that lesson the hard way after the bell yesterday. The stock has fallen 7% after the social networking site reported declining “monthly average users.” In other words, fewer eyeballs viewing ads and lower revenue guidance.

The miss was no surprise to us here at Hedgeye. In fact, the bearish case on TWTR has been the mantra of Hedgeye Internet & Media analyst Hesham Shaaban since issuing his original Black Book on the stock, pre-IPO on Nov. 2013.

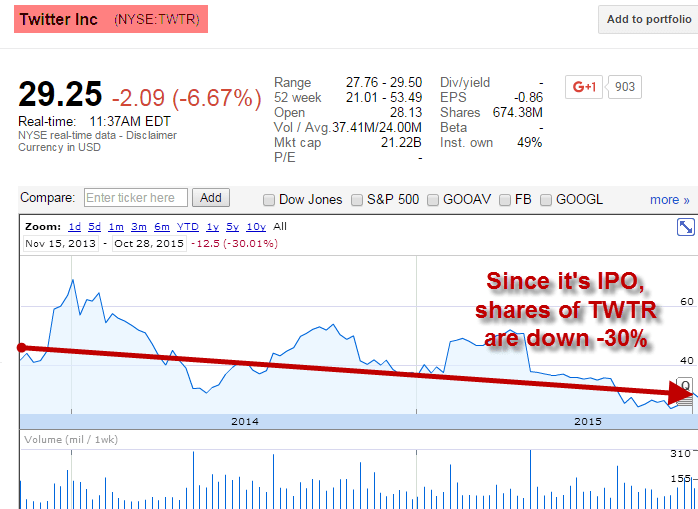

Since then shares are down 30%.

Here’s a small snapshot of a research update sent out to subscribers this morning.

And two recent HedgeyeTV videos of Shaaban laying out our bearish Twitter thesis.

The Crossroads: Here’s What Twitter Management Needs to Do, 9/3/2015

Why Twitter's Problems Run Deep, 6/15/2015

Editor's Note: If you’d like to learn more about our institutional research offerings or access our Twitter research please ping sales@hedgeye.com.