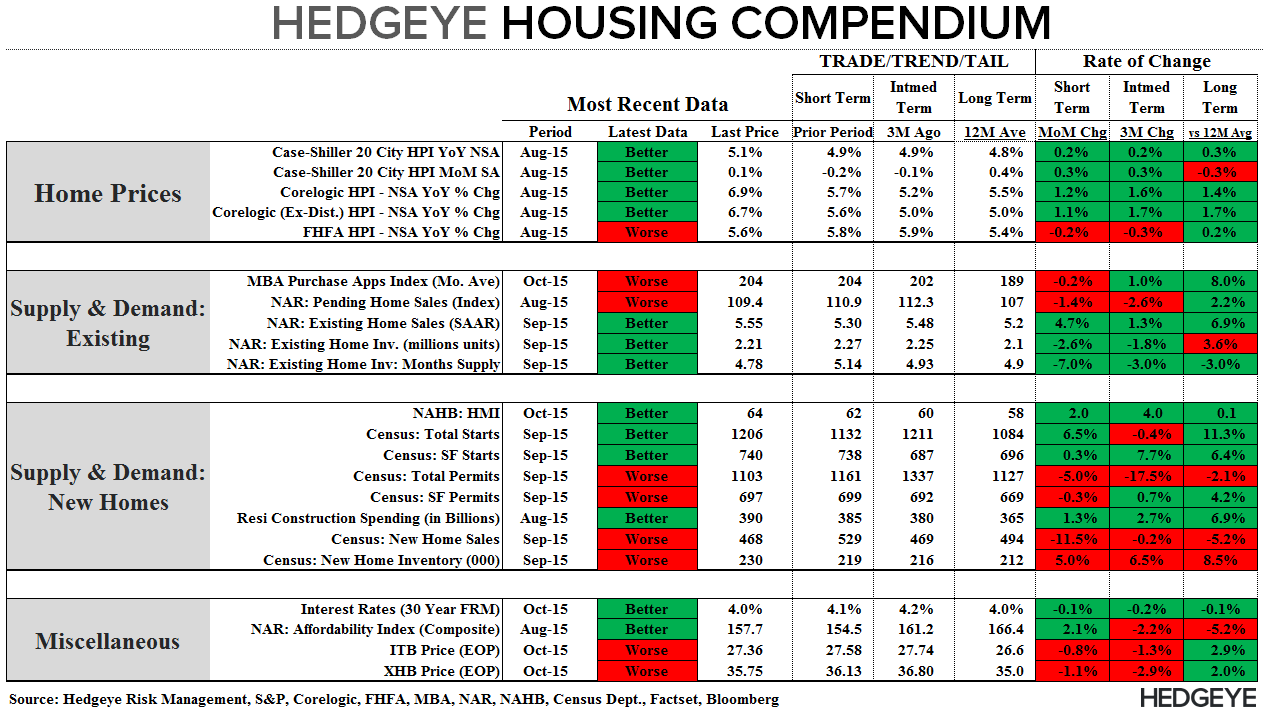

Our Hedgeye Housing Compendium table (below) aspires to present the state of the housing market in a visually-friendly format that takes about 30 seconds to consume.

Today's Focus: MBA Mortgage Applications

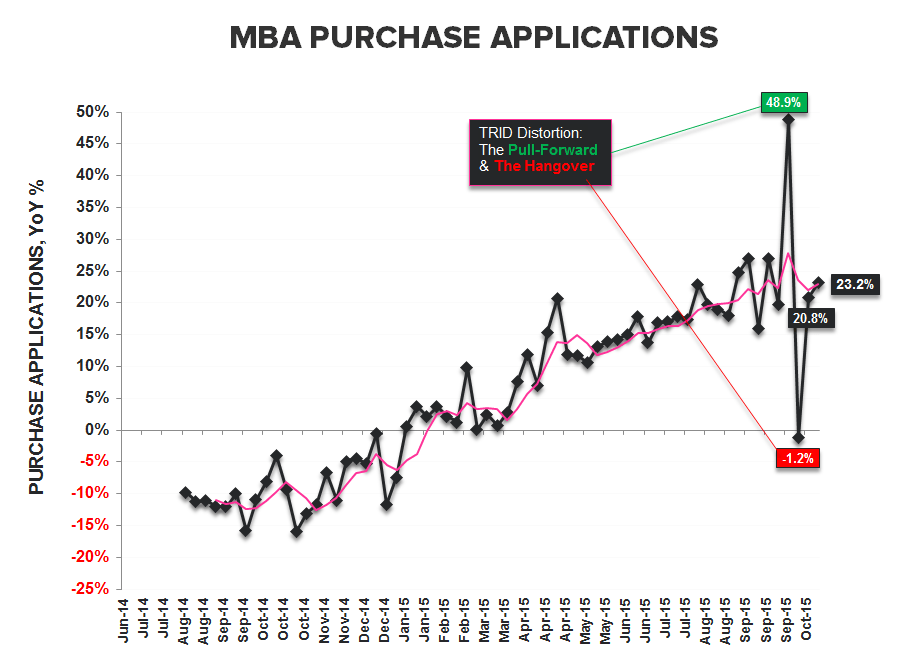

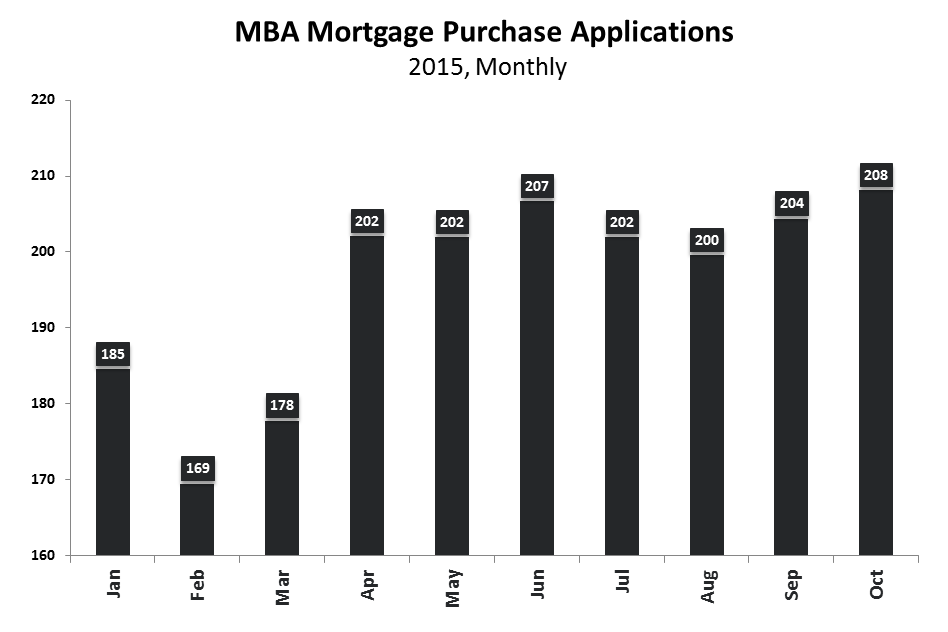

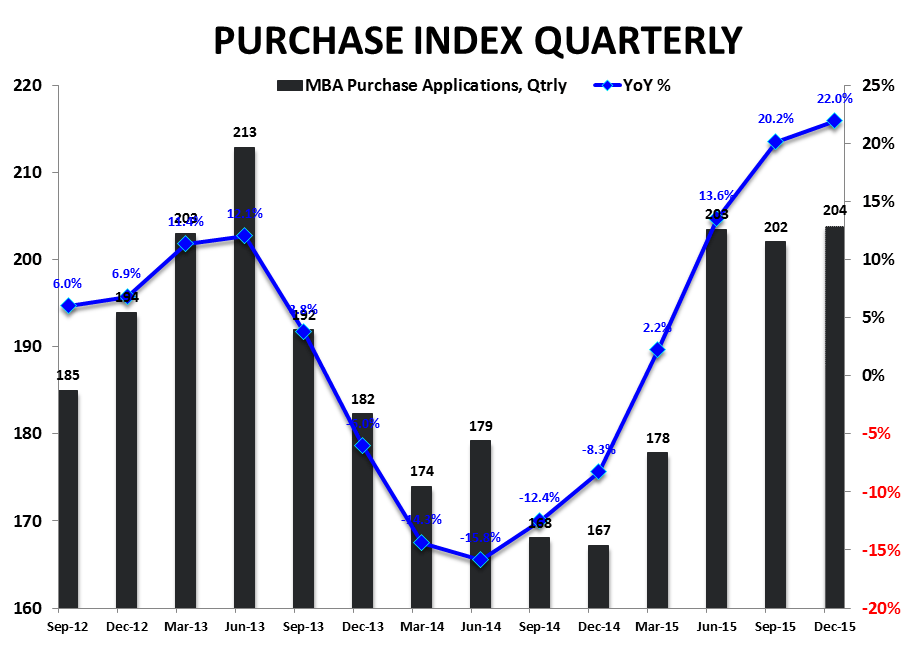

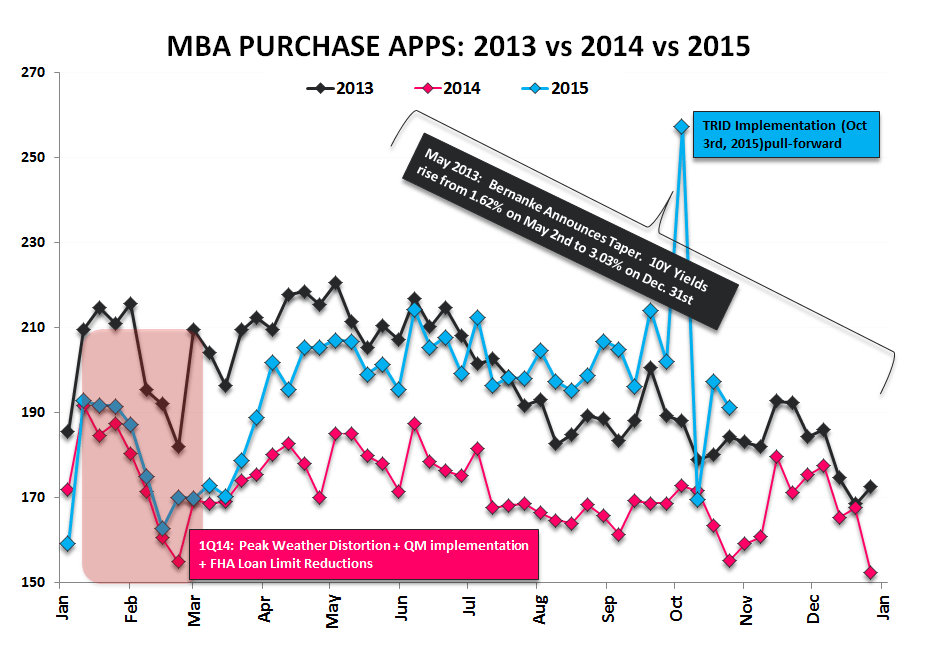

The Data: Purchase Apps declined -3.1% WoW but accelerated back near the fastest pace of growth YTD at +23% YoY.

The Distortion: The TRID related pull-forward in demand and its subsequent reversal convoluted the first two weeks of October data (see 1st chart below). The last two weeks of semi-clean data have averaged 194.3 – which compares to the 3Q average of 202 and the YTD average of 194.4.

So the data was marginally softer sequentially, better on a year-over-year basis and largely in-line with the recent quarter and YTD trend. Discerning a discrete inflection in trend from a single, middling print in a volatile high-frequency data set is challenging, particularly with some measure of residual distortion likely still impacting volumes.

The Disagreement: We’re more interested in tomorrow’s PHS data for September which we hope will serve as the arbiter of the underlying demand Trend/TRID implementation impact as the Purchase Application (up significantly) and New Home Sales (down significantly) data for September told antithetical demand stories.

The preponderance of housing data remains strong (HPI, HMI, EHS, Purchase Apps, Interest Rates, Seasonality, Election Cycle, etc) but given the NHS decline alongside the emergent slide in consumer confidence, the recessionary data in the industrial space and twin softness in the Aug/Sept Employment reports, we’re more acutely focused on marginal shifts in the data than we have been in a while.

About MBA Mortgage Applications:

The Mortgage Bankers’ Association’s mortgage applications index covers more than 75% of mortgage applications originated through retail and consumer direct channels. It does not include loans delivered through wholesale broker and correspondent channels. The MBA mortgage purchase applications index is considered a leading indicator of single-family home sales and construction. Moreover, it is the only housing index that is released on a weekly basis.

Frequency:

The MBA Purchase Apps index is released every Wednesday morning at 7 am EST.

Joshua Steiner, CFA

Christian B. Drake