Our Hedgeye Housing Compendium table (below) aspires to present the state of the housing market in a visually-friendly format that takes about 30 seconds to consume.

Today’s Focus: August Case-Shiller HPI & 3Q15 HVS

HVS: Housing Vacancy Survey, 3Q15

We received the Census Bureau's HVS survey data for 3Q15 this morning.

The HVS survey is timely and widely cited, but it’s volatile and doesn’t always comport cleanly with the more comprehensive annual Census/CPS housing surveys or a common sense reading of reality.

We take the data with a grain of salt and, while we view the magnitude of change as a distorted reflection of the underlying reality, we view directional changes in the data as a largely accurate depiction of the underlying trend.

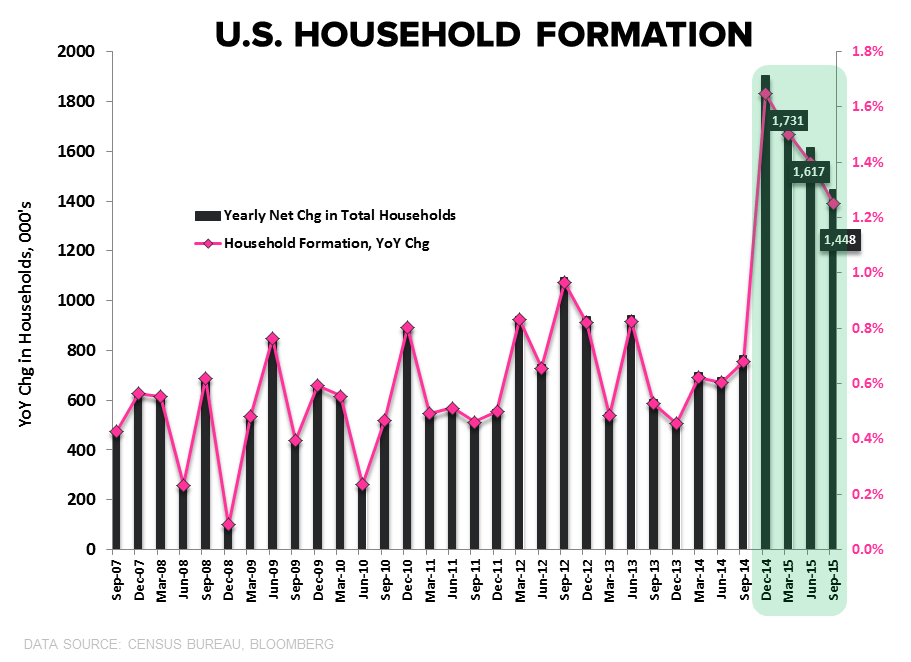

Household Formation: The yearly net change in Households in 3Q15 was 1.45MM, down modestly sequentially but marking a 4th straight quarter of breakout following a half-decade hibernation in household formation following the great recession.

The gains were again concentrated on the rental side with 92% of the increase stemming from an increase in renter households. Notably, however, 3Q15 marked the first time in 6-quarters in which Owner Occupied Households saw positive gains on both a QoQ and YoY basis. The quarterly HH formation trends along with the cumulative HH formation changes by type are shown in the charts below.

Homeownership: The National Homeownership Rate bounced off the 48-year low recorded in 2Q, rising to 63.7% in 3Q from 63.4% prior. The seasonally adjusted Homeownership Rate was flat sequentially at 63.5%.

The one callout is probably the notable increase in the Homeownership Rate among 18-34 year-olds which increased to 35.8% in 3Q from 34.8% prior.

Given that the employment recovery for that age cohort - which lagged the broader employment inflection - is now maturing towards the 3-year mark and has been growing at a premium to the broader average over the TTM, it's not particularly surprising to see upward pressure on ownership rates. Ongoing improvement in employment/income trends should continue to support rising headship rates with emergent rental demand slowly tricking through to the SF purchase market.

Again, we don't put significant stock in the precision of the HVS estimates but the data has begun to move directionally.

Case-Shiller HPI: August Godot Arrives (kinda)

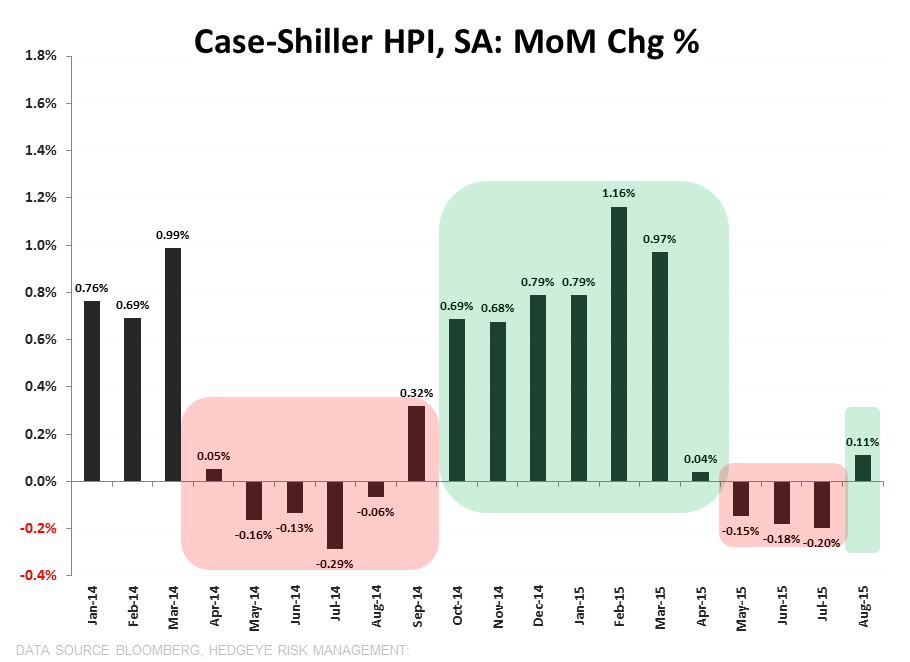

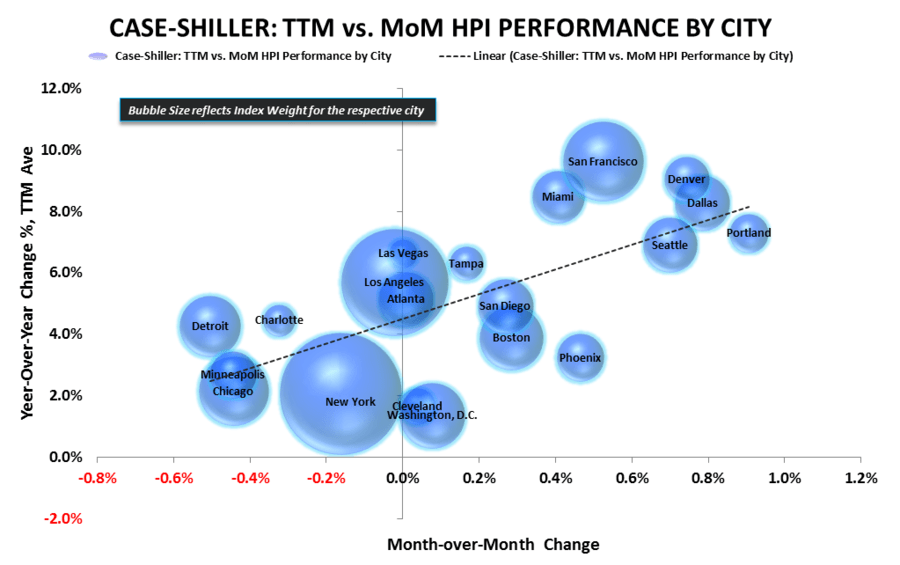

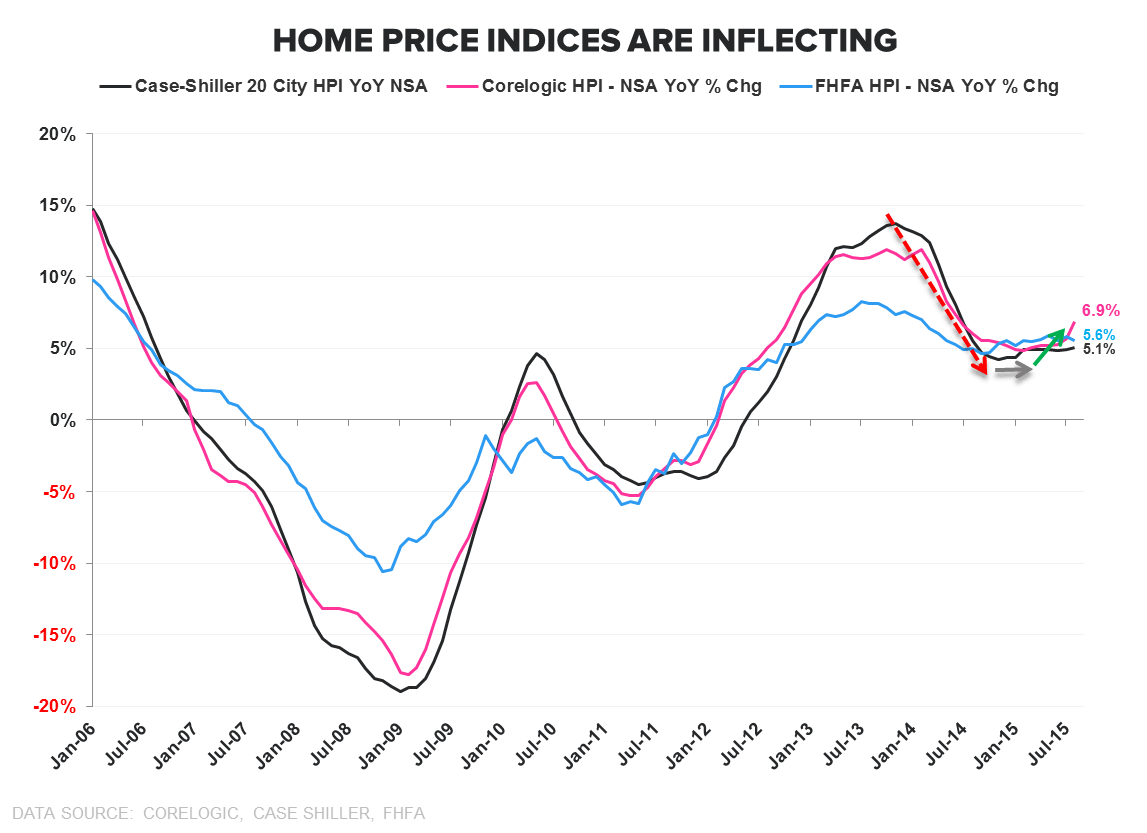

The Case-Shiller 20-City HPI for August released this morning – which represents average price data over the June-August period – showed home prices rose +0.11% MoM while accelerating +20bps sequentially to +5.1% year-over-year. On an NSA basis, 18 of 20 cities reported sequential increases (down from 20 last month) while, on an SA basis, 11-cities reported increases (up from 10 prior). Notably, the Case-Shiller National HPI (which covers all U.S. Census divisions) accelerated for the 6th consecutive month, accelerating +10bps sequentially to +4.68% YoY.

Improving second derivative price trends have augured outperformance in the housing complex historically as rising prices are margin supportive and help perpetuate the Giffen Good dynamic that characterizes housing demand.

The National Case-Shiller HPI has been in accord with the improving price trend observed in the CoreLogic and FHFA series since late 1Q. The 2nd month of improvement in the 20-City Index in the latest August data provides more solid evidence that the most lagging of the HPI series is (finally) beginning to comport with the broader trend in prices.

About Case Shiller:

The S&P/Case-Shiller Home Price Index measures the changes in value of residential real estate by tracking single-family home re-sales in 20 metropolitan areas across the US. The index uses purchase price information obtained from county assessor and recorder offices. The Case-Shiller indexes are value-weighted, meaning price trends for more expensive homes have greater influence on estimated price changes than other homes. It is vital to note that the index’s printed number is a 3-month rolling average released on a two month delay.

Frequency and Release Date:

The S&P/Case-Shiller HPI is released on the last Tuesday of every month. The index is on a two month lag and therefore does not reflect the most recent month’s home prices.

Joshua Steiner, CFA

Christian B. Drake