"I would love to be in the room watching someone who needs to consult these directions."

- Brian Regan

There are actual directions for how to eat a Pop-Tart.

Apparently we’ve devolved to the point that “remove pastry from pouch” needs to be an actual instruction.

And yes, it says microwave on high for 3 seconds … As in "three" seconds.

Back to the Global Macro Grind….

The Pop-Tart bit isn't mine but it's great (you can watch it HERE, it’s worth your 3 minutes).

In complexity, proper Pop-Tart preparation rivals what has been perhaps the most profitable macro strategy of the last half-decade.

Stop me if you’ve heard this one:

Rotate the QE (Euro/Yen ↓) => $USD ↑ => Reflation ↓ => Growth/Inflation Expectations ↓ => Bonds ↑

In other words,

When Draghi or Kurodo have the QE ball => Euro/Yen Go Down => the Dollar Goes Up => things priced in those dollars go down => Inflation expectations and OUS growth expectations flag => the market prices in those expectations and bonds get bid (again).

Yup, that’s it. Pop-Tart macro strategy alpha fully-baked in 3 seconds.

With global inflation expectations priced in dollars and central planning centricity defining markets in the post-crisis period, that QE-Currency connection has only played out “like infinity times” (my 5-year olds new favorite line) over the last 6 years.

Moving on.

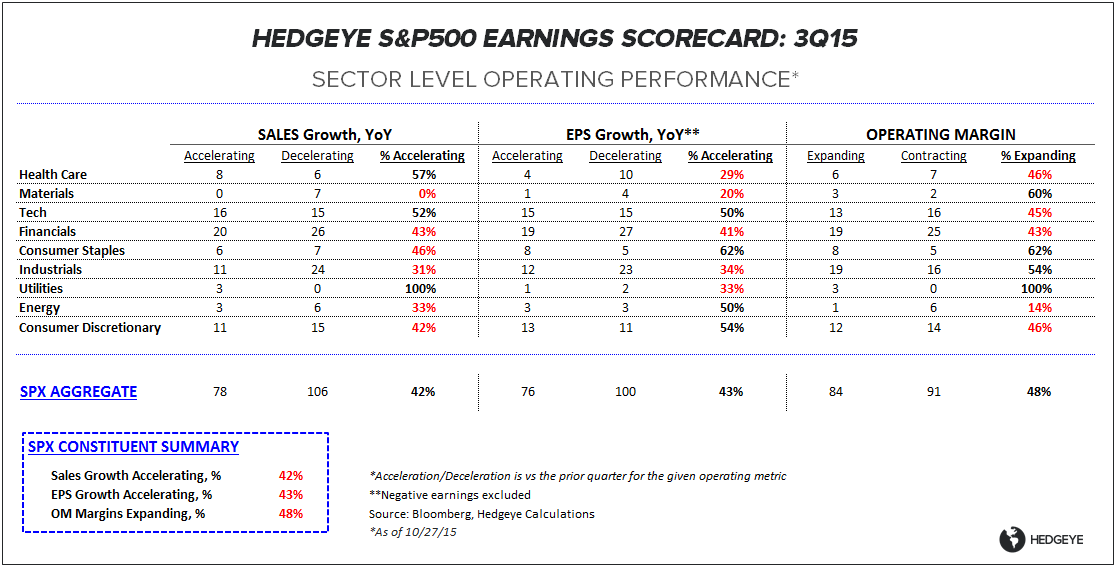

Keith has provided some high level earnings season updates the last couple weeks. Let’s take a quick look below the flaky, frosted surface of earnings management to the thin layer of toasted growth at the center:

3Q Earnings Scorecard: With ~40% of SPX constituent companies having reported earnings for 3Q, the growth data remains dismal – particularly for a private sector economy purportedly still flirting with a multi-year march higher in policy rates.

- Sales/EPS: In the aggregate, Sales growth is running -3.08% while Earnings growth is tracking at -3.31%. Granted, the weakness is once again centered on the energy and the industrials complex but those sectors don’t operate in a vacuum and that softness has begun to creep in across the Financials, Staples & Tech sectors as well.

- Beat/Miss: Only 43% of companies have beaten topline estimates while 75% (in-line with recent qtr averages) have beaten on EPS. Indeed, despite 9-months of progressive deflation in consensus estimates, a full 0% (as in “zero”) of Materials and Utilities companies have managed to best sales expectations thus far in 3Q. Again, the weakness is not just confined to the energy/commodity space – across Consumer Discretionary, Staples and Financials less than 46% of companies have beaten revenue estimates. A topline recession with broad margin contraction is not a fundamental factor cocktail supportive of resurgent capex and gangbuster hiring.

- Missing’s Mattered: The Macro has been driving the fundamentals but accurately forecasting those fundamentals has mattered again as we’ve seen sector variance increase and stock picking has re-emerged as an alpha driver. 75% of companies that have missed earnings expectations have gone on to underperform the market by -6.7% on average while 70% of the companies that have beaten have outperformed the market by +3.7% over the subsequent 3 trading days.

- Operating Performance: Taking a 2nd derivative view of the data, operating momentum has remained decidedly underwhelming with just 43% and 45% of companies registering sequential acceleration in sales and earnings growth, respectively. More than 50% of companies have reported sequential contraction in operating margins as well. Our operating performance scorecard for 3Q to-date can be seen in the Chart of the Day below.

What about housing? You guys like the housing trade for 4Q but that New Home Sales print yesterday was a complete brick.

Yea it was. We like housing currently and we are more than willing to pivot on our view if the data supports it (recall, we were bearish in 3Q) - but the current data is noisy and incongruent. Here’s the summary contextualization, hopefully you’re well caffeinated:

TRID (Tila Respa Integrated Disclosure) – which was a regulatory change in mortgage disclosure requirements and required a large-scare overhaul of lending and mortgage financing systems – went into effect on October 3rd. Mortgage Purchase Applications which had been running +2.41% MoM and ~+20% YoY in September, shot up to +50% YoY to close out September as demand was pulled forward ahead of the implementation.

In other words, according to the MBA (Mortgage Bankers Association), Mortgage Purchase Demand (which includes mortgages for both New and Existing Homes) was up big in September with the bulk of the increase stemming from the regulatory distortion.

In contrast, the Census Bureau data for the same period showed New Home Sales declining -11.5% MoM and decelerating to +2% YoY - marking the lowest level of sales in 10 months and well off the +20% year-over-year pace of growth averaged YTD.

Two data sets, two completely different conclusions on the sequential direction of housing demand. They can’t both be correct.

The lone avenue for reconciling the difference is if all of that excess purchase demand reported by the MBA was concentrated in the existing market. That seems unlikely.

But we won’t have to wait long for additional clarity as Pending Home Sales (which represents signed contract activity in the existing market) for September will be released on Thursday. We’re content to wait on that before taking a more convicted view on the state of underlying demand or the distortive effects of TRID implementation.

The evolution of social media and the democratization of information flow has been great. A byproduct of that evolution, however, has been an exponential increase in noise – the informational/analytical equivalent of empty calories.

Filter you’re source menu by accountability, transparency and analytical density.

Better yet, be your own source.

Our immediate-term Global Macro Risk Ranges are now:

SPX 1

RUT 1135--1175

UST 10yr Yield 1.98-2.09%

VIX 13.56-19.77

Oil (WTI) 43.28-46.13

Gold 1151-1175

You don’t get the brain you want by not using the one you have,

Christian B. Drake

U.S. Macro Analyst