KEY POINTS

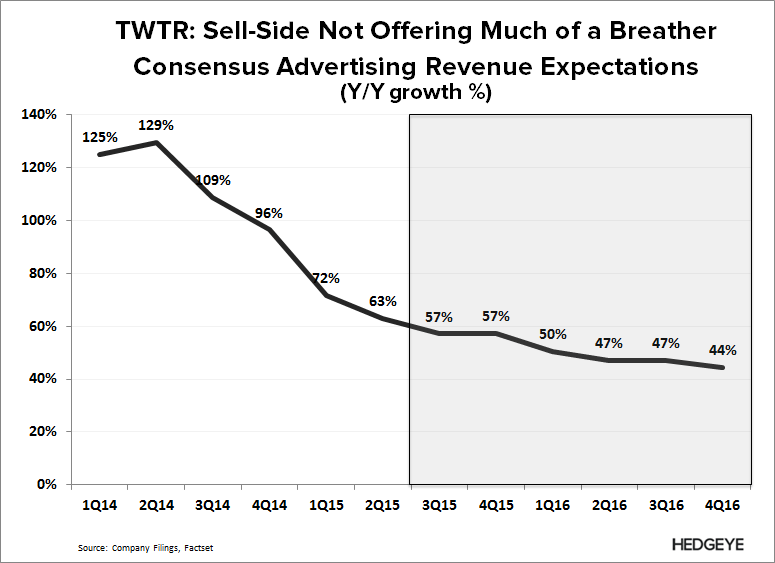

- UPSIDE ALREADY EXPECTED? TWTR preannounced 3Q15 revenues to come in at or above the high end of guidance, so now a 4Q guidance beat may also be the expectation. That will be a challenge since consensus is assuming no decay in y/y ad revenue growth from 3Q to 4Q, which means TWTR can't afford any slippage on either engagements or CPE (despite slowing user growth and its first positive CPE comp from 4Q14, respectively). While acquisition revenue could help fill the void, consensus already appears to be baking that in with 4Q data licensing revenues ramping to $63M by 4Q (vs. $50M reported in 2Q). However, TWTR could produce upside on MAUs following tepid user growth comments on its last call.

- BUT TRICKY SETUP: We’re not sure what matters more on this print: the release or how the new C-suite addresses the street regarding the longer-term story. That’s really tough to gauge since we’re not sure what Dorsey could offer to breathe life back into this story; but he may not need much on muted sentiment. But we also suspect that Dorsey knows that 2016 expectations need to be rebased, and doubt he is willing to risk another blow up similar to the 1Q15 release. That said, we suspect the new c-suite may try to manage expectations before it releases 2016 guidance on the next print (also less incentive to guide high for 4Q15).

- WHAT WE’RE KEYING IN ON: Ad engagements and CPE; the wider the divergence between the two, the more TWTR is increasing ad load. We suspect TWTR's surging ad load is what is causing its softening user growth metrics, and mgmt's ongoing attempts to appease street revenue expectations has led to a heighted level of cumulativer churn that will ultimately cap its long term upside (see 1st note below). Put another way, TWTR has been chasing short-term upside at the expense of long-term damage to its model; we're ultimately trying to figure out whether that may change under the new regime.

See notes below for supporting analysis on TWTR's user retention issues and monetization strategy. Let us know if you have any questions, or would like to discuss further.

Hesham Shaaban, CFA

@HedgeyeInternet

TWTR: The Crossroads (User Survey: n=7,500)

08/25/15 07:48 AM EDT

[click here]

TWTR: What the Street is Missing

05/19/14 09:09 AM EDT

[click here]