It’s clear to us, and we suspect many others, that BLMN is going to have a bad 3Q15. Given that the stock is down 28% year-to-date, we also suspect that the company will not recover from the 3Q15 miss and it will translate into a disastrous year. If the fundamentals unfold the way it looks like they will, the company is going to need to revisit the need for a major restructuring.

WHAT NEEDS TO HAPPEN

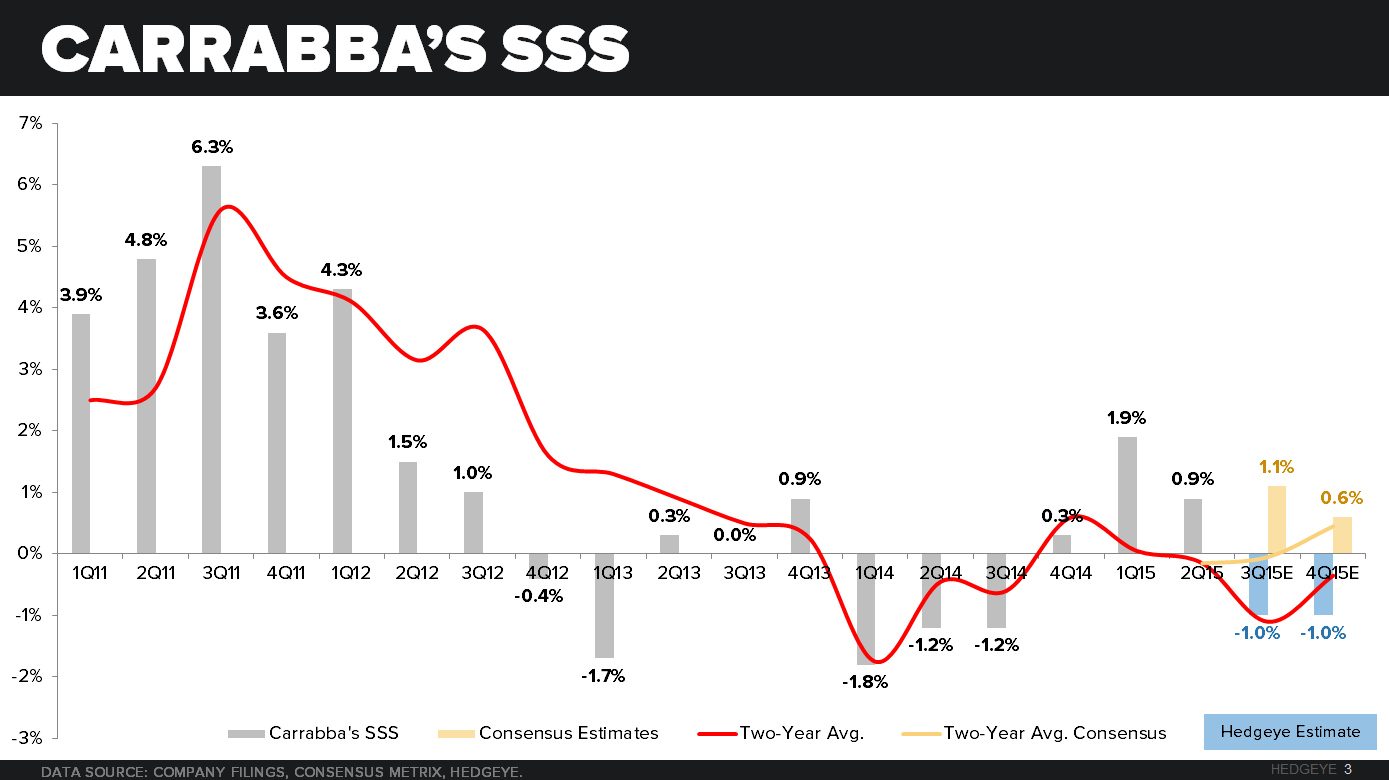

BLMN needs to sell off non-core assets and focus on the core concept, Outback Steakhouse. Looking at the same-store sales performance of Bonefish and Carrabba’s below, it’s clear that these concepts are in a secular decline and need to undertake a new path, under new ownership. Management constantly reminds investors that “we remain disciplined stewards of capital as we focus on delivering on our long-term goals and driving shareholder value.” Despite this, we believe that multi-branded casual dining companies are inefficient with capital, no matter what management says.

This means reprioritizing their investments as appropriate. For now, they should focus their investments on international opportunities, the successful Outback relocation initiative, new units at Outback and Fleming's and the remodel program that will keep assets up-to-date.

WHAT TO EXPECT IN THE QUARTER

The company is scheduled to release earnings on November 3rd before the market opens. As we see it, for 3Q15, BLMN will post flat EPS year-over-year of $0.10 for the quarter vs consensus at $0.14. For full year 2015, we see estimates coming down to $1.20 versus consensus at $1.27.

For 3Q15 we see the Outback concept missing same-store sale estimates by 370bps. In addition, Bonefish and Carrabba’s will also miss by 170bps and 210bps, respectively. In 2Q15, management updated full-year comp sales guidance from “at least 1.5%” to “approximately 1.5%.” At the time, the lowered expectation was due to lower sales expectations at Bonefish.

Needless to say the disappointing same-store sales will lead to disappointing margins. We suspect that the biggest deleverage relative to expectations will come from the Labor and Other expense lines.

On the positive side, management will likely lower expectations for commodity inflation. As of 2Q15, management expected commodity inflation to be between 3.5% and 4% down from 4% to 6% at the beginning of the year.

VALUATION

The stock has a very low value relative to its peers, but low is not always cheap. BLMN, currently trading at 6.8x EV / NTM EBITDA could compress slightly from here. Where we believe the real price drop will come from is a decline in EBITDA. We are currently projecting them to have total EBITDA in 2015 in the $445mm to $455mm range. Looking out into 2016 we are not expecting it to increase in any meaningful way, leading us to our bearish take on the name. Below is chart of EV / NTM EBITDA, showing little upside, with a reasonable amount of realistic downside.

MACRO MONITOR – STEAK TRACKER

For those of you who were not able to read our first note using the Macro Monitor, please refer to the link HERE. The macroeconomic data sets in the monitor allow us to pin point data that is relevant to the company and compare it to actual and projected performance. Economic data such as CPI, PPI, PCE, etc, is reported on a monthly basis, allowing us to get an intra-quarter read on the companies trends.

We are naming this the “Steak Tracker”, right now it consists of three very relevant employment and CPI data sets that have given a reliable read into the trends of Outback Steakhouse. The first is Men Employment 55-64 YOA, we view this age group as a major consumer of steak at restaurants. Secondly, CPI – uncooked beef steaks, and lastly CPI – beef and veal have been great barometers for Outback Steakhouse SSS trends.

As you can see all three of these are trending downwards. These trends, coupled with our fundamental analysis of the troubles this company is facing lead us to our BEARISH thesis, and with that we are adding it to the SHORT bench.

The stock is cheap and could get cheaper!

Additionally, we are also going to be taking Cracker Barrel (CBRL) off of the SHORT Bench.

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst