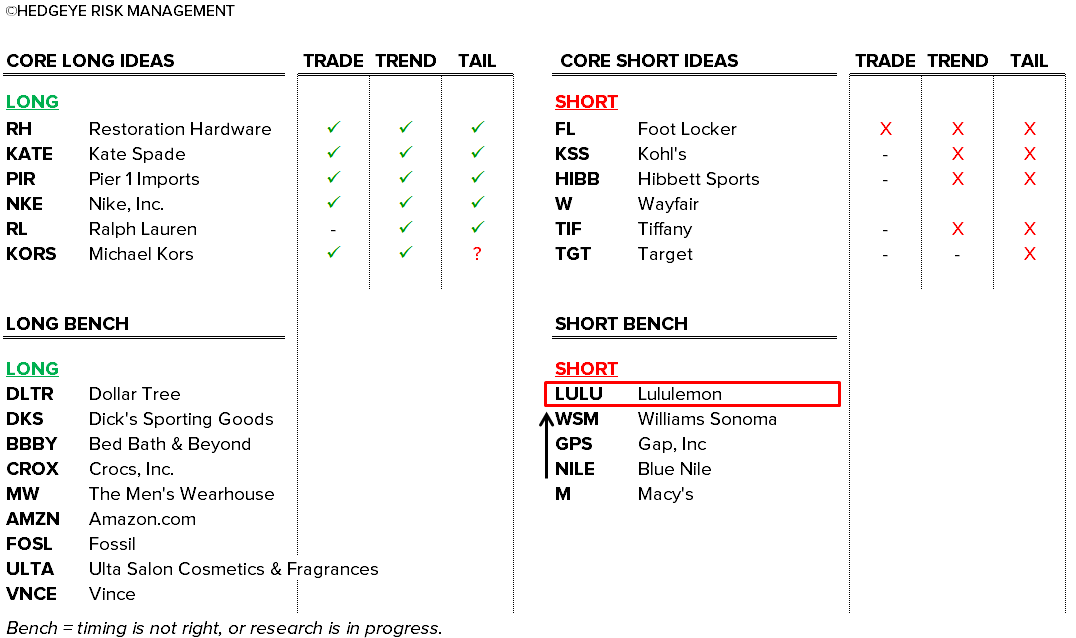

Hedgeye Retail Idea List

We took LULU to the top of our Short bench this week. While the stock sold off with the market on Friday, we still think that there is a very high liklihood that last week's management change is a precursor to the CEO ultimately getting fired. While we think that's a bullish event, it would likely come along with another operational Black Eye (miss and guide down). When we have a better sense of the timing -- or if the stock heads higher from here -- we'll press this short meaningfully.

To see our note LULU | CEO IS ON THE BLOCK NEXT - CLICK HERE

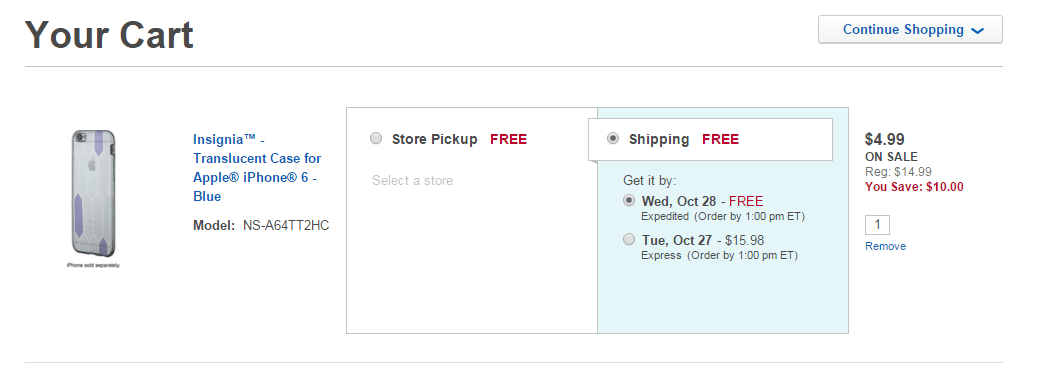

BBY, TGT, WMT, AMZN - Best Buy starts the move to free holiday shipping this year, announcing free shipping with no minimum order through Jan. 2.

(http://www.ecommercebytes.com/cab/abn/y15/m10/i26/s03)

BBY has kicked off the Free Shipping wars as we'll call them this year with a $0 free shipping promotion that kicked off on Sunday. We can't think of many things on the Best Buy site that we would actually buy that fall below the old $35 threshold, but in the rare instance that a consumer wants to buy a $5 iPhone case (see example below), well now it ships for free.

Target was the biggest player in the space to turn to free shipping last year. Though we haven't seen a formal announcement from the company yet, a few promotional pieces make it appear that TGT will start a similar free shipping promotion running through the Holidays on November 1st. And we would not be surprised in the least to see several other retailers use this as an offensive weapon. Unfortunately, for almost everybody except the bullet-proof content-owners of the world (i.e. Nike) that math doesn't work and free shipping would be even more dilutive to margins. Even worse news is that if they don’t play ball, then there’s risk to the top line (i.e. if either KSS or JCP opts-in to the free-shipping game, they both lose). The way we see it, retail is facing three margin headwinds heading into the quarter 1) free shipping, 2) labor inflation, and 3 bloated inventory positions.

LULU - Lululemon plans to expand the West Edmonton mall store which does $7000/SqFt. Taking size from 3.600 SqFt to 7,000 SqFt

(http://www.retail-insider.com/retail-insider/2015/10/lululemon)

JCP - J.C. Penney cutting 300 of 3400 positions at HQ

(http://www.retailingtoday.com/article/jc-penney-letting-go-00-hq)

WMT - Wal-Mart continues pressure on vendors, looking to reduce SKUs and extend its payment windows.

(http://www.wsj.com/articles/wal-mart-shrinks-the-big-box-vexing-vendors-1445820469?alg=y)

Hudson's Bay Company Announces New Off-Price Concept with launch of Find @ Lord & Taylor

(http://investor.hbc.com/releasedetail.cfm?ReleaseID=938301)

TJX - The TJX Companies, Inc. Completes Acquisition of Australian off-Price Retailer Trade Secret

(http://investor.tjx.com/phoenix.zhtml?c=118215&p=irol-newsArticle&ID=2100900)

UA - Curry Two launched Saturday, and Dub Nation colorway to launch Tuesday