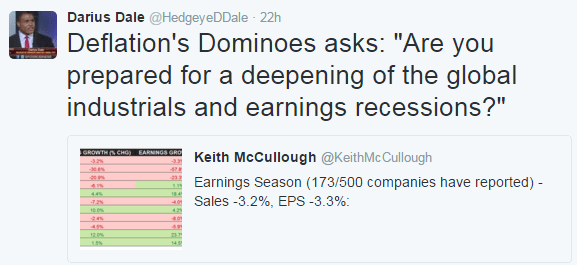

We’re still in the early days of earnings season. Here’s a quick update on where we stand. As you can see below, it's not looking good.

U.S. industrial firms are continuing to warn of a pullback in spending. Why? Because we're in a global industrial recession.

Click headline below to read full story.

Make no mistake. This year has been the best year for short selling since 2008 - every hedge fund should have capitalized on it. There is plenty of alpha out there for hedge funds to be capturing in 2015. Here are a few recent long/short ideas we've highlighted to our customers (see Pandora, Athenahealth and Boyd Gaming in respective order here, here and here.)

Hedgeye Macro analyst Darius Dale chimed in on these developments:

On a related note, I think hedgies shorting the lows and then chasing these highs will be one major reason why stocks crash again.