Key Takeaway:

Brazil appears to be coming apart at the seams. Sovereign CDS have widened to +455 bps, up another +14 bps last week. The move is remarkable not just because of its speed and magnitude (swaps have doubled since June), but also because not much else in EM following suit. While most of EM was widening from the summer through the early Fall, the trend over the last ~4wks has been tightening, whereas Brazil continues to widen.

More broadly, most of our heatmap below has shifted from red to green based on the latest data. One broader theme underpinning the move is the central bank action from China last week. The positive reaction came despite the country's third quarter GDP coming in at 6.9%, the slowest rate since the financial crisis. Chinese slowing continues to be a point of concern for us, and we advise caution against relying on central-bank-stimulated optimism.

Current Ideas:

Financial Risk Monitor Summary

• Short-term(WoW): Positive / 6 of 12 improved / 1 out of 12 worsened / 5 of 12 unchanged

• Intermediate-term(WoW): Positive / 7 of 12 improved / 2 out of 12 worsened / 3 of 12 unchanged

• Long-term(WoW): Negative / 2 of 12 improved / 2 out of 12 worsened / 8 of 12 unchanged

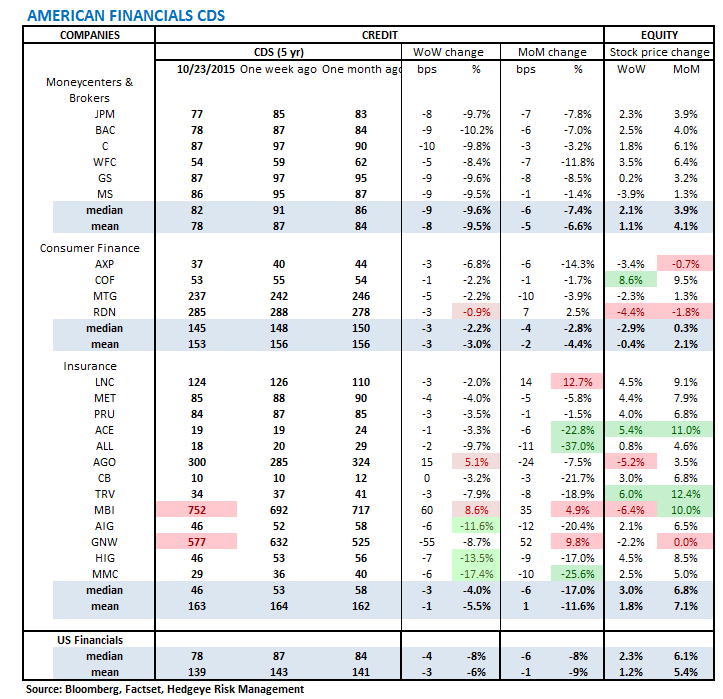

1. U.S. Financial CDS – Swaps tightened for 21 out of 27 domestic financial institutions. CDS for Genworth financial tightened the most, by -55 bps to 577, while CDS for MBIA widened the most, by +60 bps to 752.

Tightened the most WoW: MMC, HIG, AIG

Widened the most/ tightened the least WoW: MBI, AGO, SLM

Tightened the most WoW: ALL, MMC, ACE

Widened the most MoM: LNC, GNW, MBI

2. European Financial CDS – Swaps mostly tightened in Europe last week. Likely aiding the decrease in risk perception was a better than expected reading from the EU's PMI composite flash. Additionally, as expected, the ECB signaled no rate changes at its October policy meeting.

3. Asian Financial CDS – CDS for Chinese banks tightened following the PBOC's cutting interest rates and the reserve-requirement ratio. The central bank's move followed Chinese third quarter GDP coming in below 7% in the October 18 reading. CDS in India also tightened significantly, between 10 and 17 bps.

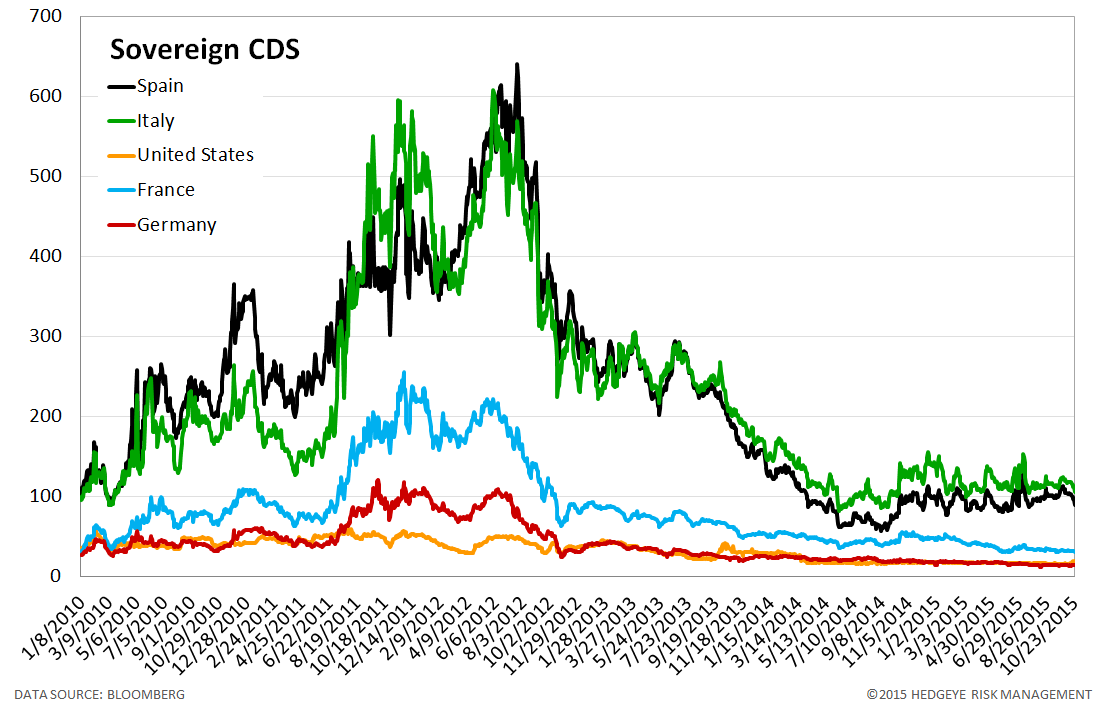

4. Sovereign CDS – Sovereign Swaps mostly tightened over last week. Spanish and Italian sovereign swaps tightened the most, both by -13 bps.

5. Emerging Market Sovereign CDS – Brazilian CDS rose another +14 bps last week to 455 bps. For context, that's roughly a doubling since the summer. What's particularly notable is that the rest of the EM complex is actually trending tighter over the last few weeks.

6. High Yield (YTM) Monitor – High Yield rates fell 15 bps last week, ending the week at 7.39% versus 7.54% the prior week.

7. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 3.0 points last week, ending at 1849.

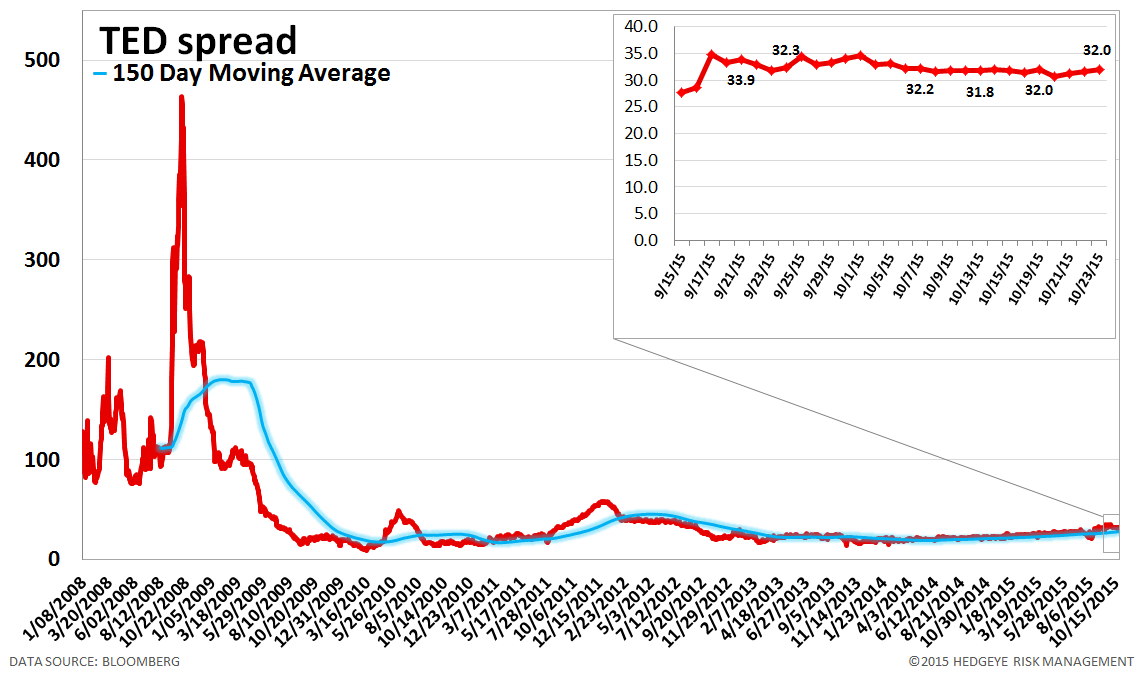

8. TED Spread Monitor – The TED spread rose 1 basis point last week, ending the week at 32 bps this week versus last week’s print of 31 bps.

9. CRB Commodity Price Index – The CRB index fell -3.1%, ending the week at 194 versus 200 the prior week. As compared with the prior month, commodity prices have decreased -1.0%. We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

10. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread widened by 2 bps to 12 bps.

11. Chinese Interbank Rate (Shifon Index) – The Shifon Index rose 1 basis point last week, ending the week at 1.91% versus last week’s print of 1.90%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

12. Chinese Steel – Steel prices in China fell 0.9% last week, or 19 yuan/ton, to 2138 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity and, by extension, the health of the Chinese economy.

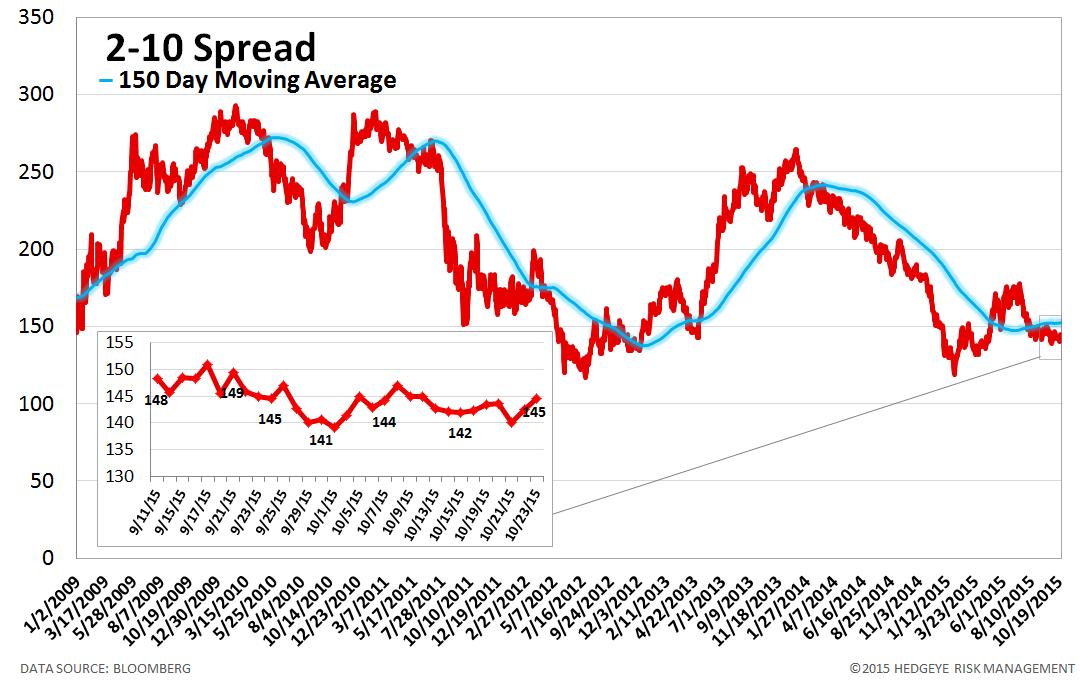

13. 2-10 Spread – Last week the 2-10 spread widened to 145 bps, 2 bps wider than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

14. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 0.0% upside to TREND resistance and -5.9% downside to TRADE support.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT