It was a very good week for our Investing Ideas recommendations.

Below are our analysts’ updates on our thirteen current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this. Hedgeye CEO Keith McCullough’s updated levels for each ticker are below.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

MCD

To view our original note on McDonald's click here.

What week it was for MCD shareholders! Shares finished the week up 7.3%.

We have been saying all along that the third quarter of 2015 would be the inflection point for the McDonald’s (MCD) turnaround. After this print, it appears that the heartache is finally over at McDonald’s, as this quarter marks the first good quarter the company has had in two years.

3Q15 EARNINGS

This quarter was astounding.McDonald’s proved once again that their brand is not dead. The operationally led turnaround is happening and the 3Q15 print was the inflection point. MCD reported total company revenue of $6.62bn roughly $210mm over consensus estimates of $6.41bn. Global same-store sales for the quarter increased +4.0% versus consensus estimates of +1.9%. The segment results were also very encouraging:

- United States reported revenue of $2.19bn versus consensus of $2.10bn, same-store sales for the segment came in at +0.9% versus consensus estimates of -0.2%.

- International Lead Markets reported revenue of $1.97bn versus consensus of $1.94bn, same-store sales for the segment came in at +4.6% versus consensus estimates of +3.4%.

- High Growth Markets reported revenue of $1.65bn versus consensus of $1.61bn, same-store sales for the segment came in at +8.9% versus consensus estimates of +4.7%.

- Foundational Markets reported revenue of $809.0mm versus consensus of $720.9mm, same-store sales for the segment came in at +6.1% versus consensus estimates of +1.4%.

Given the robust performance throughout the segments MCD reported 3Q15 EPS of $1.40 beating consensus estimates of $1.27 by $0.13. The currency impact to 3Q15 was $0.17, as the USD continues to hold its strength against most foreign currencies.

From here, the upside in the stock price lies with the growth of All Day Breakfast, additional G&A cuts, national value offering implementation, reimaging of restaurants, commodity deflation, especially in beef and increased operational efficiencies, among others. In addition, the REIT is a potential driver of incremental value but not crucial to the long-term success of this call. With Steve Easterbrook at the helm we are confident this company will be better managed than it has been in a long time.

LNKD

To view our analyst's original report on LinkedIn click here.

Shares of LinkedIn (LNKD) were up 5% today and finished the week up almost 8%. Our Internet analyst Hesham Shaaban reiterates his high-conviction in the name into its next earnings release on October 29th. We expect a clean beat and raise. We expect this will be a positive catalyst for the stock.

WAB

To view our analyst's original note on Wabtec click here.

Our short call on Wabtec played out extremely well for Hedgeye Industrials analyst Jay Van Sciver with shares down 8.4% on the week. Here's Jay's update:

We see freight rail equipment spending just starting to enter a multi-year downturn. It’s a cyclical market, and WAB shares remain priced for growth. This does not sound like a management team positioned to rescue shareholders from what we see as a ‘growth trap’. We expect 2016 EPS estimates to move below $4.00, with the recent ratcheting down just the first step.

W

To view our analyst's original report on Wayfair click here.

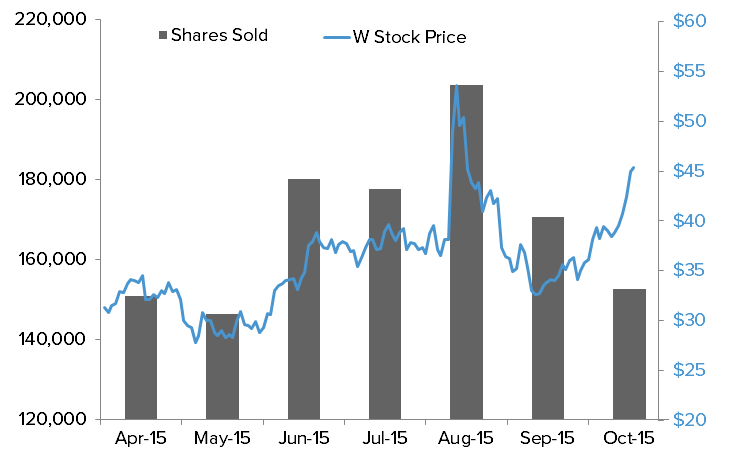

Since the IPO lockup expiration at the end of March, we’ve seen a steady drip of insider stock sales totaling ~$40mm in market value. That peaked out in August at the same time the stock hit all-time highs, but the steady flow of sales remains among the highest in consumer discretionary.

We think investors are significantly overestimating the addressable market, and that incremental sales will come from either excessive discounting, or from a part of the home furnishings space that is inherently subject to SKU transparency and commodity pricing. All of that leads to Wayfair being unable to sustain a profit over the long term.

While it might take a while, we think that Wayfair is ultimately headed to zero. Heck, if we were insiders, we'd sell our stock here too.

Insider Activity Since Lockup Expiration

TIF

To view our analyst's original report on Tiffany click here.

A notable insider purchase at Tiffany (TIF) hit the tape this week. But, contrary to what the headline suggests this is not an open market purchase, which many would consider a bullish indicator. Member of the Board of Directors, Abby Kohnstamm (former CMO IBM, now Pitney Bowes) exercised 10k options at a $39.64 strike – for net proceeds of $398,100.

Here is the skinny on TIF – Street estimates for earnings in 2016 sit at $4.54. If the macro environment plays out like we believe, then we think we’re looking at a number closer to $4.00. It is definitely not a ‘headed to zero’ short. But stocks of good companies like Tiffany go down all the time, and we think TIF is headed lower.

Abby Kohnstamm Historical Stake in TIF

RH

To view our analyst's original report on Restoration Hardware click here.

Restoration Hardware (RH) unveiled a full floor of Modern product in their New York Flatiron store this week. The new concept sits on the first floor of the 21k sq. ft. store and marks the 3rd property in RH’s fleet (along with Denver and Atlanta) to carry the new product line.

Fundamentally and financially, we’re about to see growth at RH go on a multi-year tear. We think this stock is headed to $300 over the next 2-3 years. We’ve been patient for the catalyst calendar to begin, and the waiting is finally over.

RH Flatiron Store

ZBH

To view our analyst's original report on Zimmer Biomet click here.

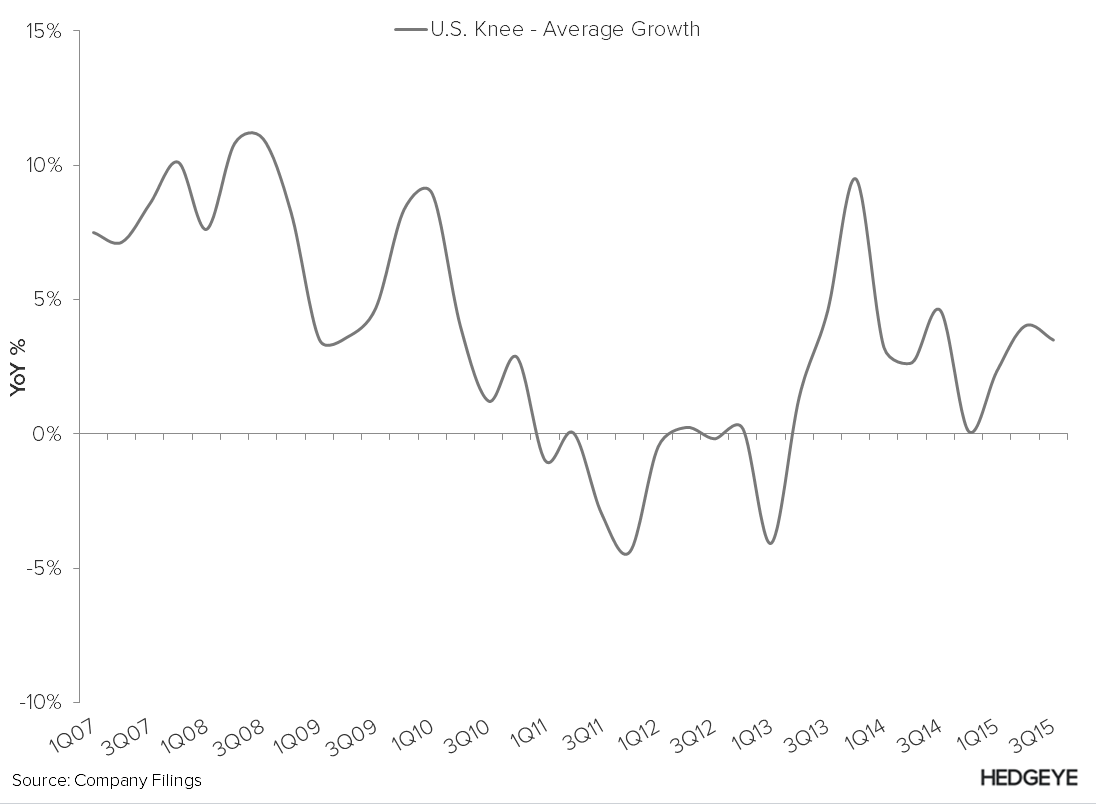

SYK reported a mixed quarter this week, there was weakness in ex-US markets, in particular Brazil and China, not from the core US Orthopedic market as we would have anticipated.

After the carnage across our #ACATaper Theme this week, the SYK quarter surprised us a little with the upside in US revenue growth. While JNJ’s Depuy division reported +2.0% growth in US Knee revenue a few weeks ago, SYK followed up with the second earnings Orthopedic report, posting 5% growth in US Knees.

We are focused on the US Knee market because we think it is the arena with the most #ACATaper potential, and the biggest product category for Zimmer Biomet (ZBH). ZBH missed revenue expectations 2Q15, the first with Biomet in the mix. At the time they suggested temporary disruption from the merger had caused the revenue miss, but “cascading execution plans” were in place, and well, executing.

Will ZBH report a number more like Depuy’s +2%, or SYK’s 5% when they report 3Q15? If SYK is benefitting from the disruption at ZBH, which we think they are, it’s likely to be closer to +2% than the +5%. Over the coming weeks we’ll continue to speak to surgeons about the trends they are seeing in case volume, device pricing, and the new Medicare global payment program, CCJR.

TLT | EDV | GLD | JNK

To view our analyst's original report on Junk Bonds click here.

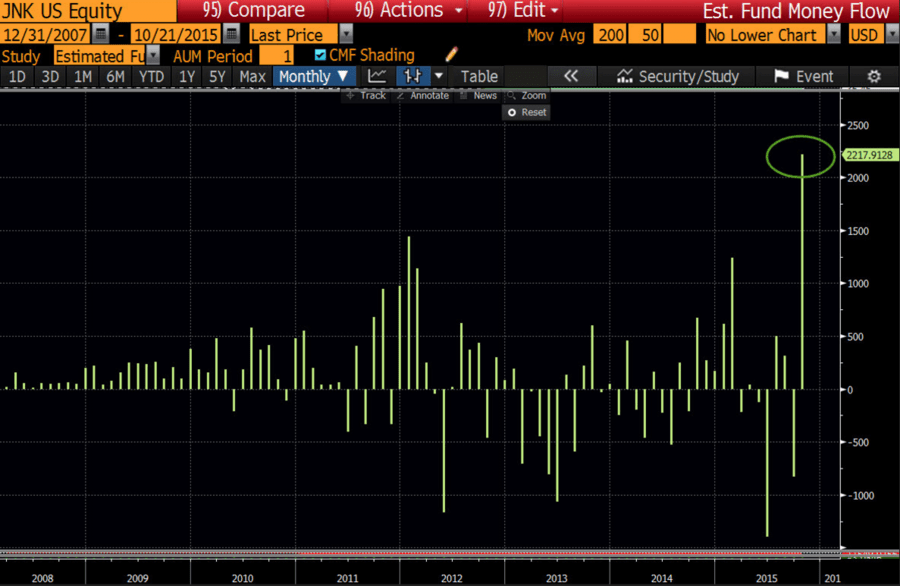

At Hedgeye, we like to pave our own non-consensus road and short things that the crowd chases. Junk bonds (JNK) are one of those vehicles. Investors have already plowed, by far, the most money ever into JNK, in October, with a full week to spare post rate-hike fears. That sounds risky to us.

The total into junk bond funds was $4Bn in October. $2.2Bn of it went directly into JNK. Large institutional players may see this as a value play post rate hike fear and sell-off, but our body of work suggests JNK is a cyclical and it’s not the beginning of the cycle. It’s maybe the 7th or 8th inning.

Here’s a chart of the October JNK Pile-in:

Source: BBG

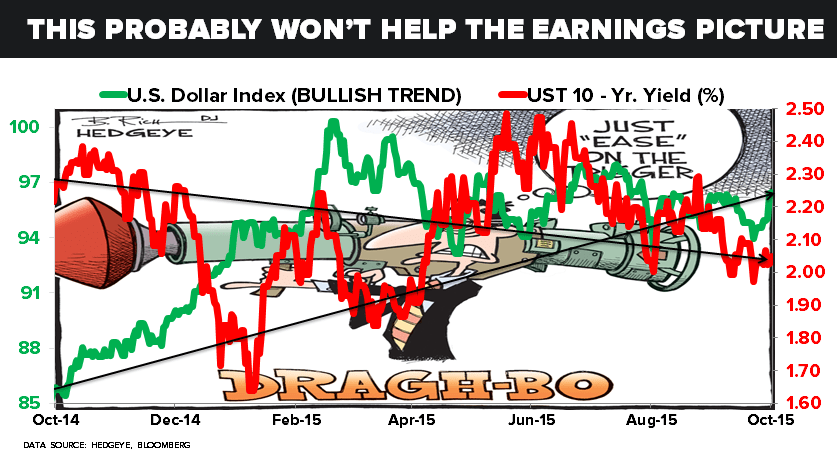

With deflation seemingly back for the time being post-ECB this week, piling into and ETF with some commodity leveraged credit risk isn’t something we subscribe to. In fact, we’re taking the other side and keeping with the short. Below is the chart of the day that we used in Friday’s “Early Look” note to product subscribers. Draghi cowbell = more global deflation:

As devaluation and global currency war jockeying from central bankers around the world continues, the acknowledgement of growth slowing continues to push yields lower. The long-bond was up on Thursday, after the ECB meeting, despite an easing-fueled rip in equities. The bond market doesn’t believe in the growth storytelling and we expect it to continue.

Remember that Down Euro Devaluation is a global TIGHTENING event because the world’s biggest asset price #deflation risk is that the world’s inflation expectations (commodities, debt, etc.) are DENOMINATED IN DOLLARS. That has implications for gold (risk to being long), but we want to get through the Fed meeting and GDP data next week before we pivot on a gold view. Stay tuned.

GIS

(No material update this week)

General Mills continues to be one of our top ideas in the Consumer Staples sector. Sector head Howard Penney loves the name for its characteristics during this macro driven market. Big-cap, low-beta, and their line of sight at growing the top line in a meaningful way, are contributors to our LONG thesis.

There has not been much notable news on GIS as of late, but they did recently announce the launch of a venture capital arm. Preexisting division, 301 inc., will now be given more control and freedom around investing and incubating smaller food startups. GIS has dabbled in this before but never in a truly focus way. Companies such as Boulder Brands and Coke do this currently and have seen success.

This is not something that will have a meaningful impact within the next year. But hopefully with some good investing and smart partnerships we will be able to see results.

ZOES

(No material update this week)

Nothing has changed at Zoës Kitchen. We still love the management team and the concept of the restaurant. But due to the macro-driven market, high beta, low-cap names such as ZOES have fallen out of favor.

If you are a "buy and hold" type of investor this is a name you want to be in for the long run, especially at these values. This company has a long runway of growth which we believe is only just in the beginning stages.