“Never believe anything in politics until it has been officially denied.” - Otto von Bismarck

Upshot: We see the potential stress at CAT Financial to be a downside catalyst for CAT shares in early 2016, and see commentary to the contrary as a sign that it is an internal concern. Deteriorating order trends still suggest that 2016 sales estimates need to move lower. If those two catalysts play out, there is the potential for CAT shares to overshoot what we would see as a long-term fair value (perhaps around 60). This management team seems frustrated, but after that 2016 reset, a new bullish narrative may emerge focused on structural cost reductions.

Relevant Prior Notes

- In Rehab: Would Reduce Short Exposure For Now (9/24/2015)

- Needed - Activist With A Time Machine (10/13/2015)

Black Book: Feeling Used?

- Replay: CLICK HERE

- Slides: CLICK HERE

Three Takeaways

CAT’s report this morning is a mixed bag; that the shares could trade higher on it is probably a sign that sentiment is a bit down on the name. We aren’t going to provide a tedious summary of the quarter since management did that at length on the earnings call. There are lots of potential call-outs, like Resource Industries finally posting a negative margin. But instead we will highlight our three takeaways.

- Hey, CAT Financial Is Fine Because Management Said So And They Always Nail It

“Just a comment on CAT Financial in our captive finance business. It's a great business model. It's been proven through several ups and downs. Key metrics are in line with long-term averages despite weakness in a few very critical markets and it's healthy, well managed and risk is very much under control.”

- Doug Oberhelman 10/22/15

This management team has consistently been surprised by the extent of the downturn in resources-related capital spending. CAT Financial didn’t exist during the last major cycle in resource-related capital equipment in the early 1980s, so we are not sure what “ups and downs” they mean. After all, management finally referred to the downturn as a “super cycle” today. We don’t think CAT Financial will do well in a super downcycle. Who would?

If we were way off base in our expectation that CAT Financial is likely to become a drag in early 2016 (say, around the 4Q earnings report & 10-K), it probably wouldn’t have been specifically called out in the press release and earnings call. We have detailed the specific exposures previously. In today’s report, we are interested by the odd combination of increased write-offs with a drop in allowance. A bit of year-end assumption updating may well relieve our cognitive dissonance.

The current level of profitability seems to us unsustainable given the likely trend in residual values and the credit prospects of customers in North American Coal/Energy, Mining, and Emerging Markets. We will need to wait for the 10-Q for the specifics.

Shouldn’t this be going the other way?

If you don’t believe us that calling out the CAT Financial “model” (odd specificity) should be a concern, here are some cherry picked quotes. They are well worth a read.

On Mining Downturn: “We've added production capacity around trucks. We are staged to be the mining leader for decades to come. And I know there are lots of headlines out there that said mining is dead, not one more ounce of coal will ever be mined, iron ore will never come back, the world's going to stop spinning, it's over. Well, it's not over….” -Douglas R. Oberhelman 9/24/2012

On Bucyrus: “The Bucyrus acquisition, we need to finish that. We're almost done. It's been almost 3 years since we bought Bucyrus. Bucyrus brought to us greater stability during the downturn, we saw that in 2009 before we bought them, and we're seeing it again in 2013, plus it gives us greater growth opportunities -- more stability, greater growth.” – 3/4/14

On Brazil’s Economy: “I'm also optimistic in Brazil, although there's an election there this weekend, but both candidates, both parties are talking about reflating the economy and Brazil has always used infrastructure as a way to do that” – 10/23/14

On Oil Capital Spending: “…sustained basis certainly will take the really agitated top off of it, but there is still plenty of room for reinvestment.” – 10/23/14

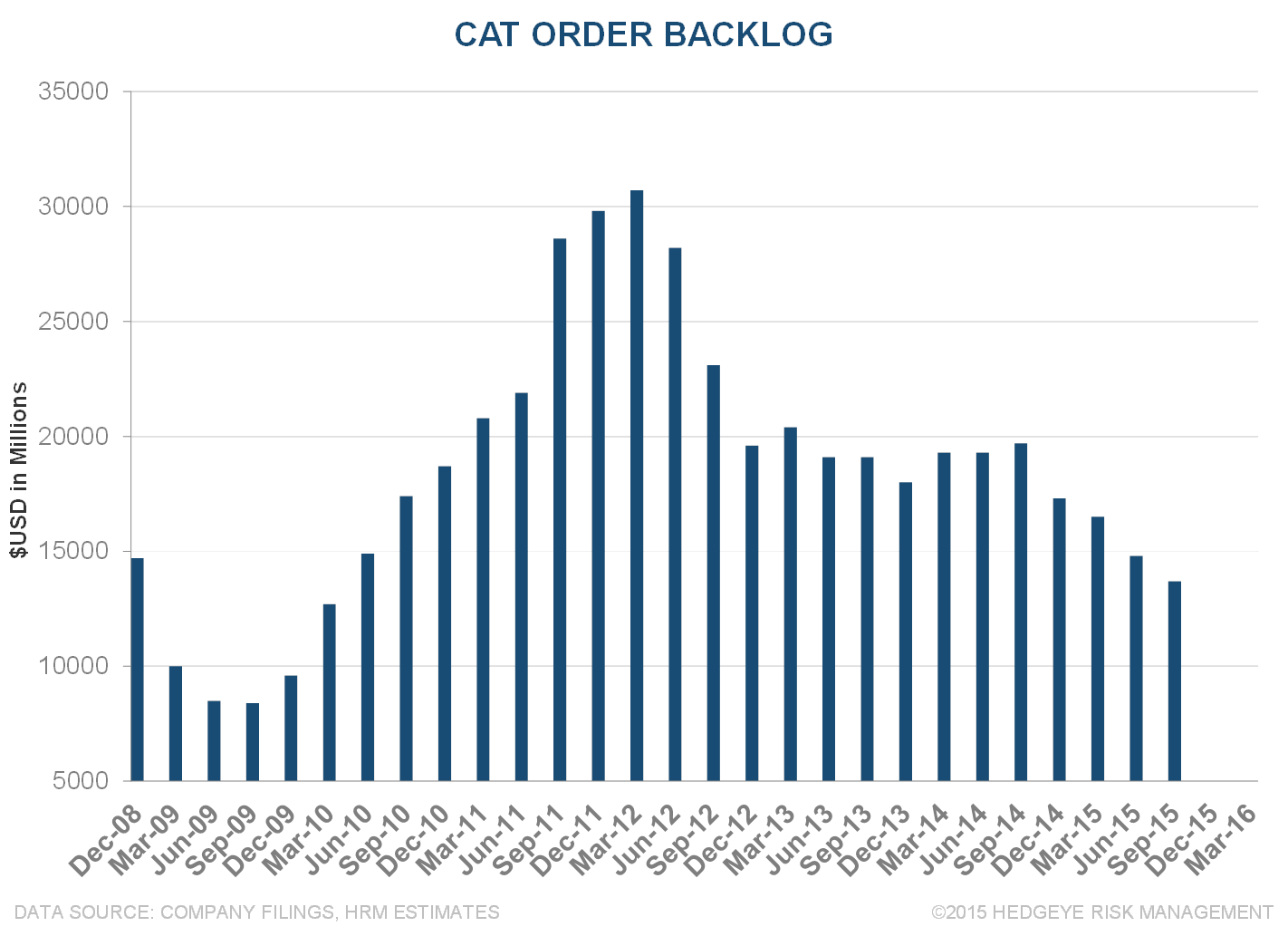

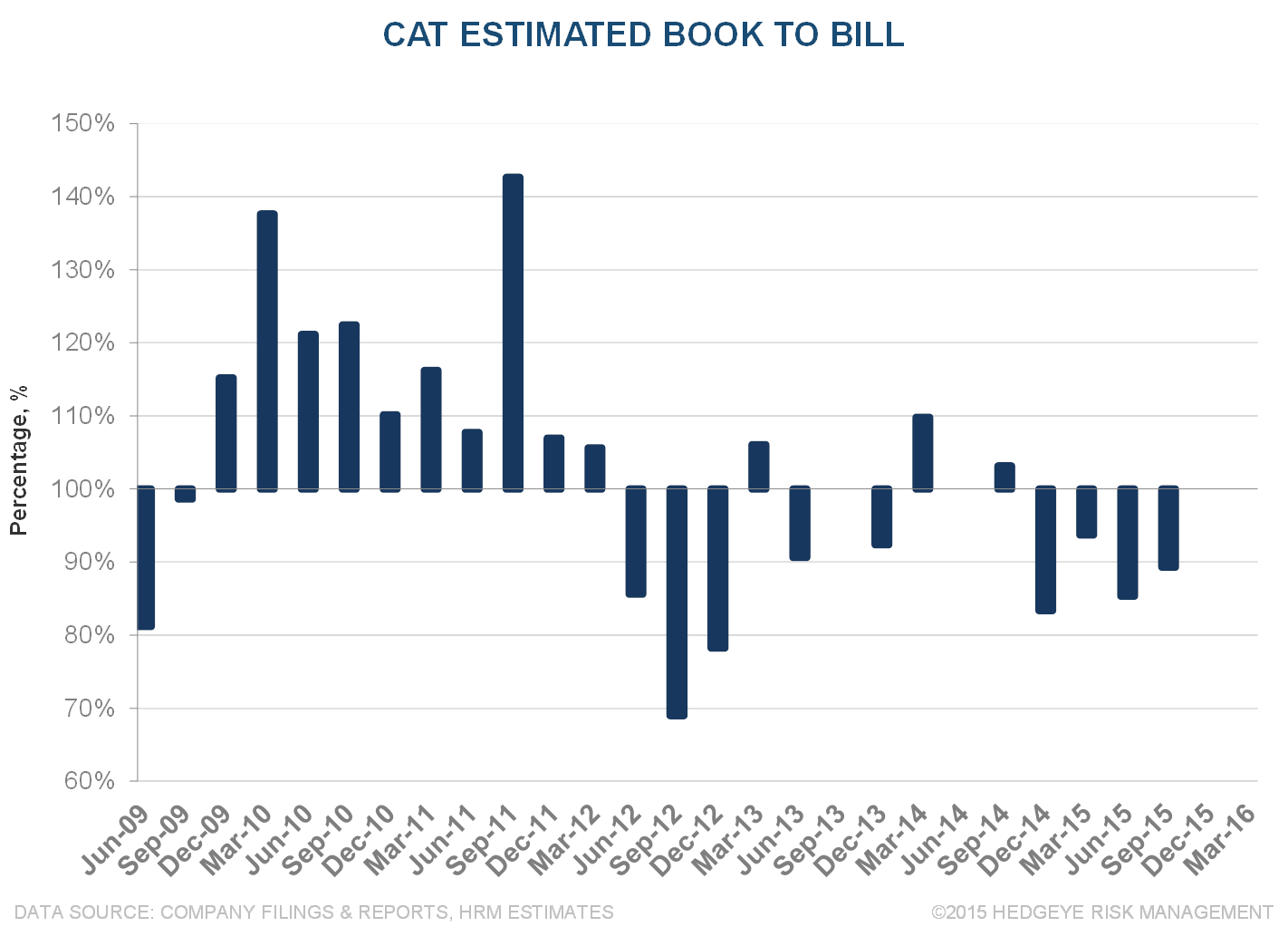

Orders, Adjusted For Dealer Inventory, Still Trending Below 2016 Estimates

While it isn’t perfect, sales rates adjusted for changes in backlog and dealer stocks gives a decent sense of the run-rate top-line. With the backlog dropping and estimated book-to-bill solidly below 1, we think 2016 sales estimates are still vulnerable. Could sales come in closer to $40 billion next year? That appears increasingly plausible. It would be very hard to look at the orders in the quarter and conclude that the bottom is in.

Not Happy With His Shareholders or The Street

In addition to the dig that “you may not as investors appreciate this in terms of dollars and cents” with respect to employee safety, there seemed general desire to avoid questions from the analyst community on the call. The initial presentation cut off Q&A, and the call was not lengthened to accommodate questions. What does a frustrated Oberhelman mean for CAT? Probably nothing good for a leader who is laying-off employees and making tough choices.

Still, CAT management now has a more positive story to tell. They do seem to be executing better on costs, and that matters. The cost view into 2016 has more credibility with the trends below.

Upshot: We see the potential stress at CAT Financial to be a downside catalyst for CAT shares in early 2016. We see commentary to the contrary as a sign that it is a concern in the C-suite. Deteriorating order trends still suggest to us that 2016 sales estimates need to move lower. If those two catalysts play out, there is the potential for CAT shares to overshoot what we would see as a long-term fair value (perhaps around 60). This management team seems frustrated, but after a 2016 reset reflecting a weaker CAT Financial and current order rates, the groundwork is being laid for a new bullish narrative in the form of structural cost reductions.