OVERVIEW

The title of our short presentation on VRX back in July 2014 was "Something New Under The Sun?". It seems like a good title in retrospect.

Click Here for the original deck

its hard to see a way out from here...

- Claim edits likely go to "deny all" for anything come out of a pharmacy named in the media or associate with VRX

- Extreme RX price inflation practices put a fast halt to prescription growth

- Regulatory scrutiny does not end quickly

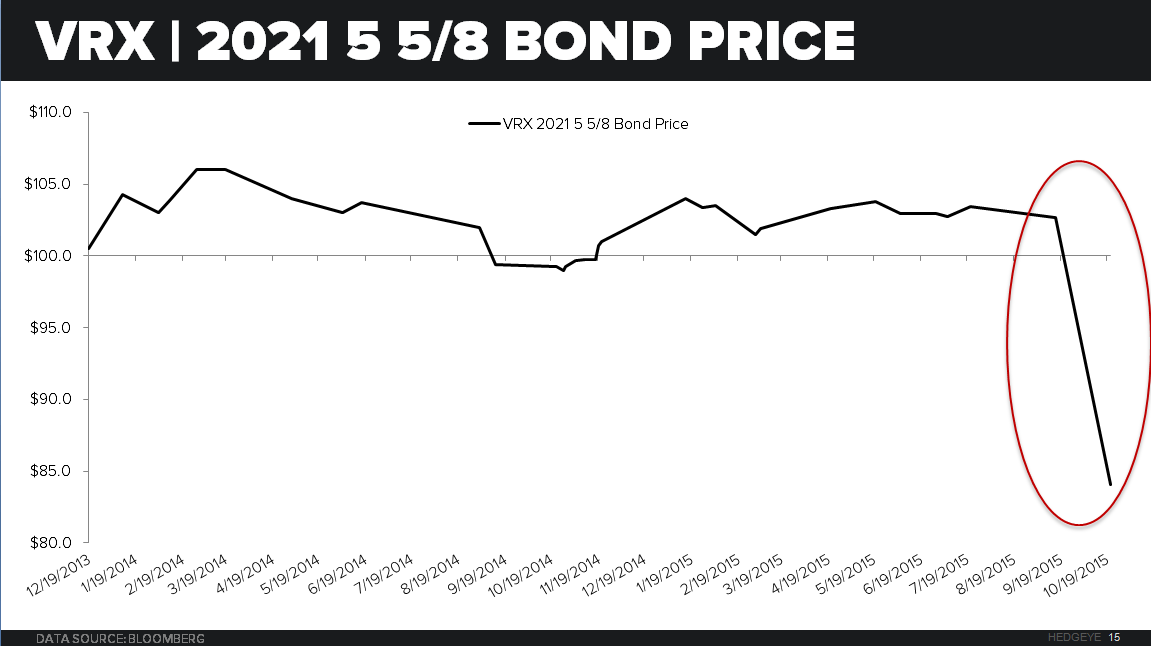

- Yields are blowing out, debt and equity capital raises look out of reach, limiting buy-back potential and end to a debt-fueled acquisition binge and the "new pharmaceutical" model.

- How quickly does anyone really think VRX can restart the R&D engines?

Please call or e-mail with any questions.

Thomas Tobin

Managing Director

@HedgeyeHC

Andrew Freedman

Analyst

@HedgeyeHIT