Chipotle (CMG) is on the Hedgeye Restaurants Best Ideas SHORT bench.

Did things for CMG change overnight? I think so!

SUMMARY OF THE QUARTER

Chipotle’s 3Q15 earnings results came in relatively close to expectations. Reported revenue was $1.22bn, which was in line with consensus expectations. Same-store sales (SSS) were 2.6% versus consensus estimates of 2.4%. Management spoke on the call about how July saw uncharacteristically high performance due to the BOGO coupon provided after participating in the Friend or Faux game (which ran for 6 weeks and accounted for 2mm transactions). Following that event August and September were slower in comparison, “…we’re kind of just holding our own. I don’t think we’re accelerating, but we’re not decelerating,” said CFO John Hartung during the call. CMG saw relief within its food costs, which were 33.0% in the quarter, down 134bps YoY, as they experienced deflation in avocados and dairy. Labor continues to affect the P&L, restaurant level margins decreased 49bps in the quarter to 28.3%, due to higher labor, marketing and promotion costs. Earnings per share is where CMG faltered this quarter, posting EPS of $4.59 versus consensus estimates of $4.62, missing by $0.03.

Going into this quarter we had some concerns about the business going forward, which we outlined in a note HERE.

- Quality real estate is getting harder and more expensive to get

- Are the 2015 supply chain issues a one off experience?

- Slowing sales trends might not end in 3Q15

The company essentially confirmed two of our three concerns.

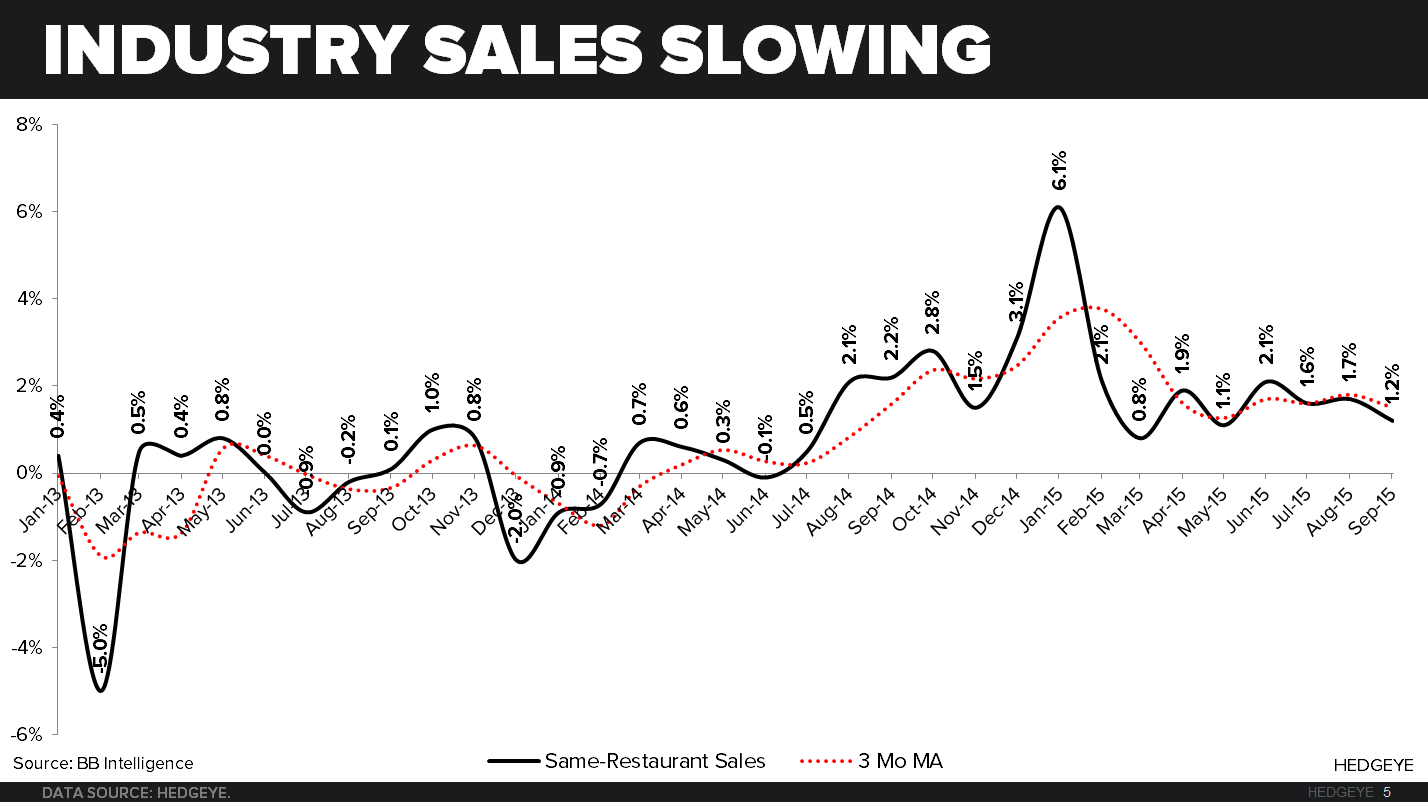

SALES TRENDS

John Hartung, Chief Financial Officer, Chipotle Mexican Grill, Inc. – “Our sales comps were highest in July when our Friend or Faux campaign was in full force, but were lower in August and September. We were happy with the customer response and engagement with Friend or Faux during July as our customers who played the game learned about our simple wholesome ingredients and were treated to a BOGO for playing.”

HEDGEYE – The use of BOGO’s is a sign of maturity and not a good one. It's a favorable that consumers responded positively, but there was no follow through.

Mark Crumpacker, Chief Creative and Development Officer, Chipotle Mexican Grill, Inc. – “Our mobile and online sales continued to grow for the seventh consecutive quarter and currently represent more than 5% of topline sales, up more than 40% over last year.”

HEDGEYE – Getting mobile technology right is part of the bull case, but CMG appears to be behind the curve. We will be waiting and watching to see how this develops.

John Hartung, Chief Financial Officer, Chipotle Mexican Grill, Inc. – “we just finished a three-year trend, and I've talked about this on some earlier calls. If you go back and look to 2013, we started a new trend where we started in low single-digit comps, and we kind of built our comps for the next several quarters. We had a price increase in 2014. But if you combine the last three years – and this is kind of the end of that trend – our three-year comps are up in the high 27%-28% range. We now need to start a new trend because we started that momentum. And if you look quarter to quarter, you can see that the momentum builds for several quarters, then it levels off. It peaked last year at 19.8%, and then as you are comparing through multiple years, up double digit comps.”

HEDGEYE – We believe it to be unrealistic to anchor a bullish call on CMG based on 3 year cycles. We don’t believe that phenomena truly exist. The only three year pattern we see in the company, is price increases every three years. The increase in traffic is more cyclical or luck than it is reality. At the end of 2012 and the beginning of the last "3-year cycle", CMG announced that it was going GMO-free. Around this announcement, the company generated a significant amount of incremental new customers. It’s unlikely that the company will be able to replicate this type of brand hype ever again.

We suspect that CMG will be experiencing low-single digit same-store sales for the next few years.

REAL ESTATE

We suggest that Chipotle has increased its guidance for the full year 2015 and 2016 new unit openings to a range of 215 to 225 new Chipotle restaurants in reaction to slowing same-store sales trends. The accelerated unit growth rate will only increase costs and lower margins in a slowing sales environment. In addition, as new unit growth becomes a bigger percentage of total growth it lowers the overall returns of the company.

HEDGEYE – We keep hearing from our sources that finding quality real estate sites is becoming a bigger issue for a number of restaurant companies. Part of the problem is the significant growth of the fast casual segment and the recent restaurant IPO boom that has put pressure on A rated locations.

CHIPOTLE – Monty Moran - “what's even more encouraging is that we're able to complete these restaurants in what is arguably one of the most competitive real estate markets we've seen in recent years. Our teams have given us feedback that the competition for new site locations remains high and the demand for talented contractors, subcontractors, and crews is intense as many developers are taking advantage of the current low interest rate environment”

HEDGEYE – On the margins, ROI for CMG new stores are headed lower. Yes they are coming down from industry leading returns.

CHIPOTLE - Monty Moran - “our real estate, design, and construction teams are finding favorable new restaurant sites and negotiating some of our best lease terms”

HEDGEYE – Yet the 10Q filed yesterday says “occupancy costs as a percentage of revenue increased for the three months ended September 30, 2015 primarily due to increased costs for leases entered into during 2015. They may be some of the “best lease terms” but they are getting more expensive in an increasingly competitive environment.

VALUATION

In a slowing sales environment CMG will experience a lower multiple on future profitability. Add to that, accelerating expenses associated with new unit growth, international expansion, increased labor and the company will likely also experience margin pressure.

HEDGEYE OPINION

CMG is not immune to macroeconomic pressures; in fact, they are more susceptible as consumer’s trade down to lower cost alternatives as their confidence wains. As we wrote in our CMG note this Monday adding it to our SHORT bench (NOTE HERE), jobs, consumption and consumer confidence are all slowing, coupled with industry sales slowing.

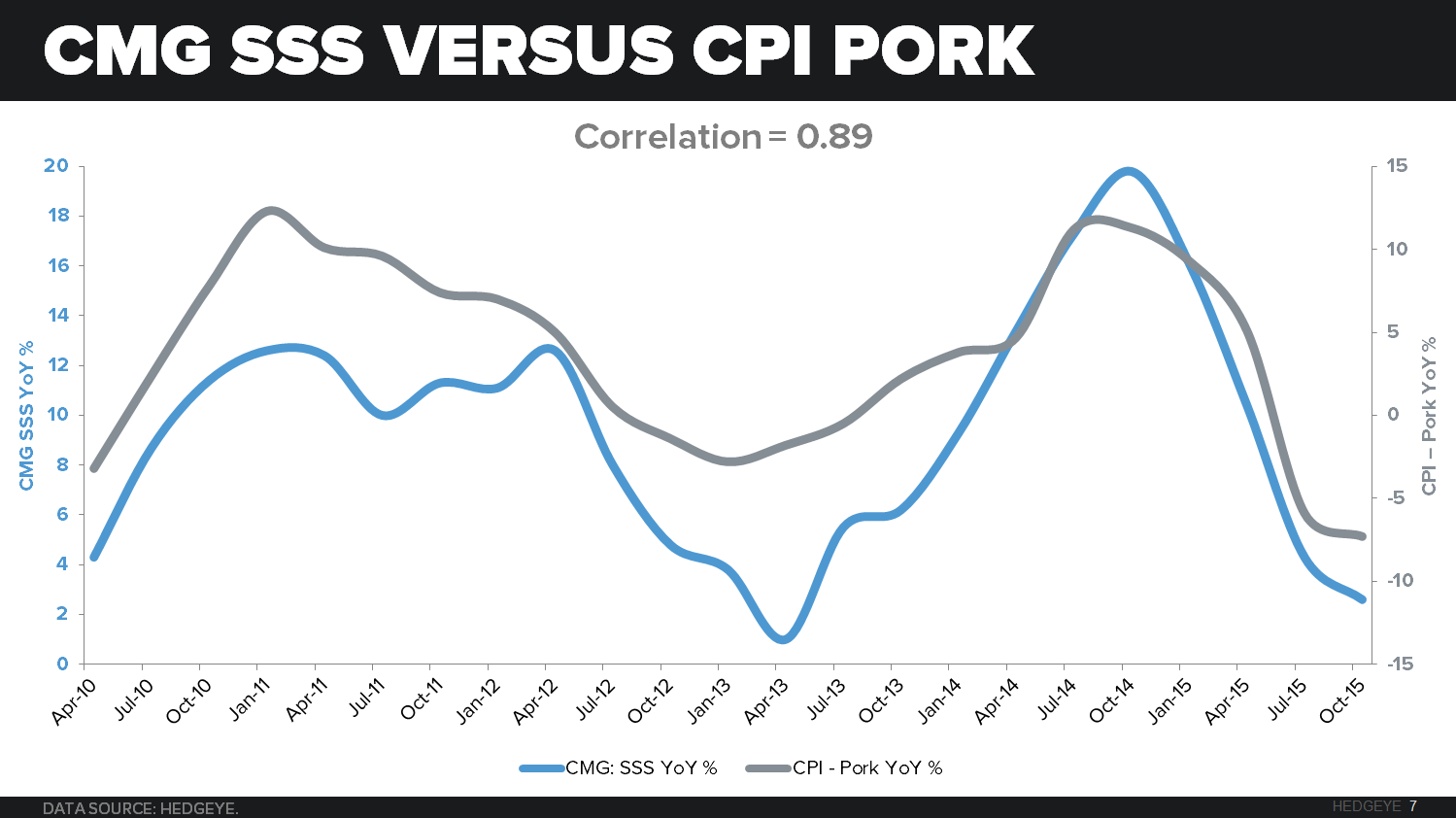

Management said nothing during their conference call to increase our confidence in their performance over the near term. On the heels of a “choppy” October, management is pegging its hopes on a recovery in sales on the return of carnitas (which is now in 90% of stores, expected to be in 100% by the end of November). We don’t see this as a prime traffic driver; it’s hard to believe that many people stopped going to Chipotle flat out because there were no carnitas. The chart below shows the correlation between CPI for Pork YoY % change versus CMG SSS YoY %. CMG SSS continued this quarter to correlate very closely with this metric, which provides us a good intra-quarter barometer for performance, and was a contributor to our conviction on the SHORT.

MANAGEMENT OUTLOOK

For 2015, management increased their guidance to 215-225 new restaurant openings, up from the previously announced range of 190-205.

- Low-to-mid single digit comparable restaurant sales increases

- Effective full year tax rate of 38.7%

For 2016, management is expecting to open 220-235 new restaurants.

- Low-single digit comparable restaurant sales increases

- Effective full year tax rate of approximately 38.7%

Low-single digit SSS in 2016 is a concerning point and is a sign of management becoming increasingly concerned about the macro environment that we went through above.

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst