Gold is the one commodity we would trade long-side right now against the dollar as we continue to believe growth and inflation expectations drive bigger currency/gold inflections. This trade continues to have legs.

An arrival at realistic expectations might end with QE4, but we have to get there first. Who would have thought QE4 would be in the discussion when “lift-off” was inevitable?

The difference for the upside in that trade between now and pre-August 19th minutes release is that the crowd has come closer to the Hedgeye Macro view.

Below we outline 5 behavioral reasons why any strong USD catalyst could provide short-term pain within a longer-term bullish set-up.

We outlined just how consensus rate hike expectations were in an Early Look on August 14th pre-consensus pivot:

The gist of that note was that within our longer term deflationary view, a snapback reflation trade was a big risk when the world is positioned for deflation. It happened…. Quick.

Can this move be just as vicious into year-end now that policy is more of a baked-in expectation?

Below we give you a few charts to keep you cautious into the ECB meeting which precedes an important week of U.S. economic data next week with Q3 GDP:

1. CONTRACT POSITIONING: What is the actual positioning from the speculative crowd?

At the end of July, net non-commercial futures and options positioning was the shortest of the post-crisis era:

- W/W into this week, net futures in options positioning moved 27% longer on a relative basis

- The net-short positioning in gold is washed out if nothing else. On a z-score basis the market is now +0.5X and +0.3x on a TTM and 3-Year basis

- Longest net contract positioning of 2015 was at the highs in gold with the shortest positioning near the end-of-July lows

- Longest gold futures positioning since late July is right now, after the unexpected catalysts

Contract positioning chases price…

2. OPEN INTEREST: BETS ARE ON

- Futures Aggregate Open Interest +~7% w/w into this week; +4.5% w/w from last Tuesday

- Futures aggregate open interest +10.0% and +10.7% above 3/6 mth averages

- Option open interest is spiking, and the divergence in Call vs. Put open interest is widest in at least 5 years as the market gets longer on a net basis.

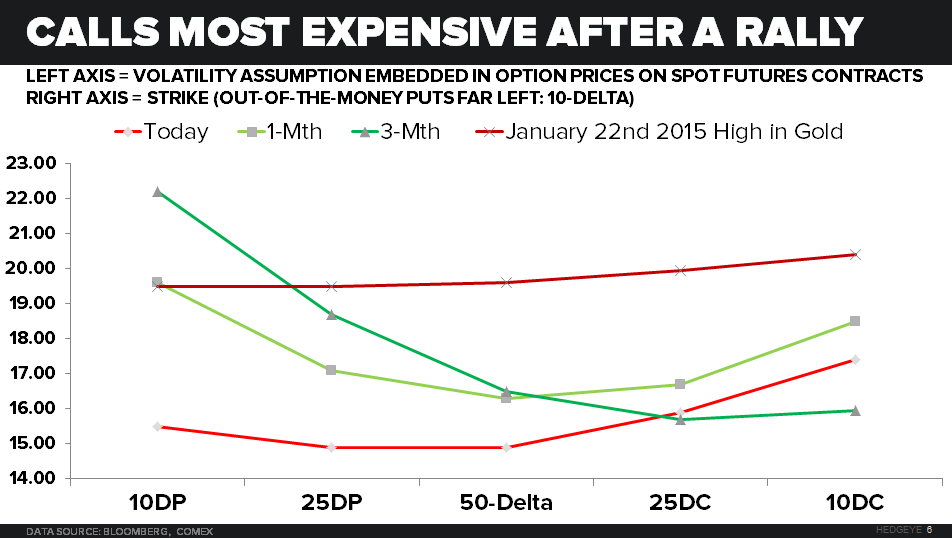

3. VOLATILY SKEW: Like contract positioning, the volatility assumption embedded in options prices also usually chases price and poses as just another indicator of consensus sentiment

- Calls most expensive to puts right now

- Puts most expensive to calls at the 2015 lows in spot gold prices

- Positive skew, like now, at $1,300 gold in January

4. CORRELATIONS: Relative currency correlations in Gold are stronger (more negatively correlated) than they’ve been over the last 3 years vs. energy correlations which remain broken. The direction of the USD is very important here and the market is increasingly in the camp that the USD moves lower.

The positioning in the USD vs. the gold positioning mentioned above is tracking -1.43X on a 1-Yr z-score basis. The USD and EUR/USD remain neutral on a TREND duration in our model, so we’re waiting and watching for direction here with the upcoming catalysts both tomorrow and next week in the U.S.

The chart below shows relative correlations which are broken ex. Just a few:

5. FED FUNDS:

The bid-yield of December Federal Funds Futures is pinned at its lowest point of the year at 17.5bps. While 5 bps above the current mid-point at 12.5bps, there is very little expectation of a December hike embeded in current prices.

Again, gold remains on the long side in our Q4 macro deck as we expect growth slowing to continue to manifest with more dovish Fed expectations, but waiting on the right time to buy is key:

Our immediate-term level of support is down at $1,150

Talk of QE4 was a non-starter back when the whole world was positioned for “lift-off.” Consensus is now coming around to our view, and the behavioral set-up in gold markets posits a short-term capitulation risk within a longer term-Trend: Slower-and-Lower-For-Longer.

Feel free to ping us with comments or questions.

Ben Ryan

Analyst