Takeaway: Orders for both rail cars and locomotives are well below delivery rates in 3Q, a situation that we do not expect to improve given weak rail volumes. 2016 build rates look at risk to us, as customers may seek stretched deliveries and manufacturers would benefit from steadier production.

Overview

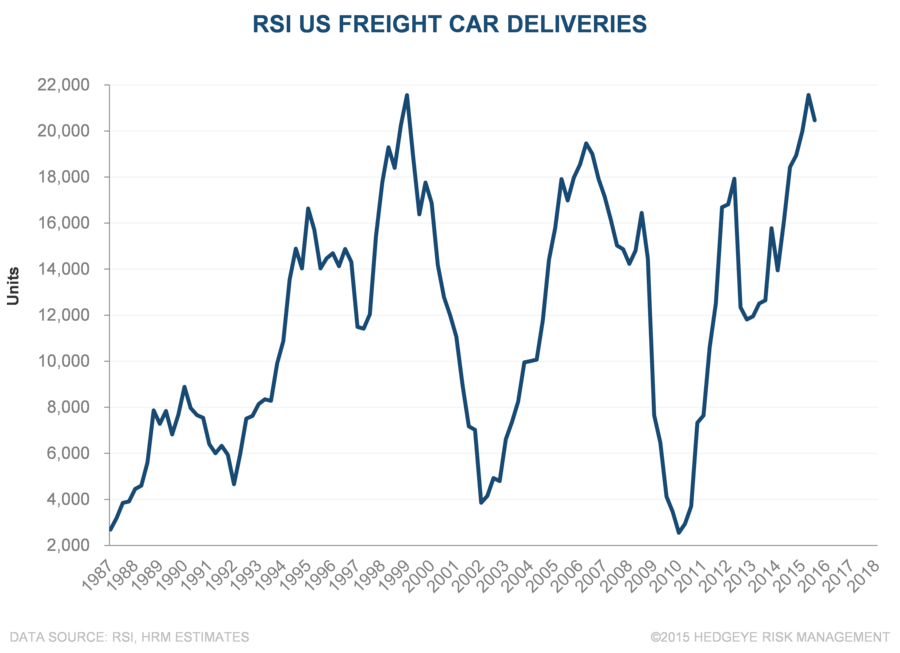

RSI reported rail car order, delivery and backlog data yesterday that provided further support to the view that rolling stock demand has entered a downcycle. GE received only 3 locomotive orders last quarter, and the RSI data points to 7,374 rail car orders vs. a build rate over 20,000. While it might seem reasonable to look at the large backlog and assume the 2016 is in the bag, many of the orders in backlog are scheduled for delivery more than 12 months forward – some into 2020. The rail car backlog itself may be vulnerable to both delivery date push outs and cancellations from captive lessors. Cancellations of third-party orders can be costly for buyers, but can also occur. At current order rates, we would expect a drop down in build rates by mid-2016, a potential negative for WAB shares.

Rail Car Demand Down

Orders…: Both rail volume growth and fleet age demographics point to a sustained period of weak rail car orders, as we see it, with the recent demand spike due to tank car regulations and the boom in fracking.

…Not Deliveries: While deliveries will tend to correspond to 3Q equipment sales for WAB, equity markets should focus on the forward looking order data. Deliveries are peaking out, in our estimation, while orders have likely entered a sustained period of below replacement demand activity.

Backlog Not So Clear: While it might be tempting to see the backlog as 6 quarters of demand, many of the orders are scheduled for delivery more than 12 months out. For example, TRN disclosed that 45% of orders were longer than 12 months out at the start of the year. Given the implementation date of tank car regulations, we would expect the backlog duration to be reasonably far out. We also think that as much as 10% of the backlog may be ‘spec’ orders from lessors owned by rail car manufacturers. We estimate that the current pace of orders and deliveries portend a potential step down in deliveries by mid-2016.

Timing A Bit Clearer: Orders will need to improve, build rates will need to be pushed lower, or 2017 will be very messy, by our estimates.