Our Hedgeye Housing Compendium table (below) aspires to present the state of the housing market in a visually-friendly format that takes about 30 seconds to consume.

Today's Focus: MBA Mortgage Applications

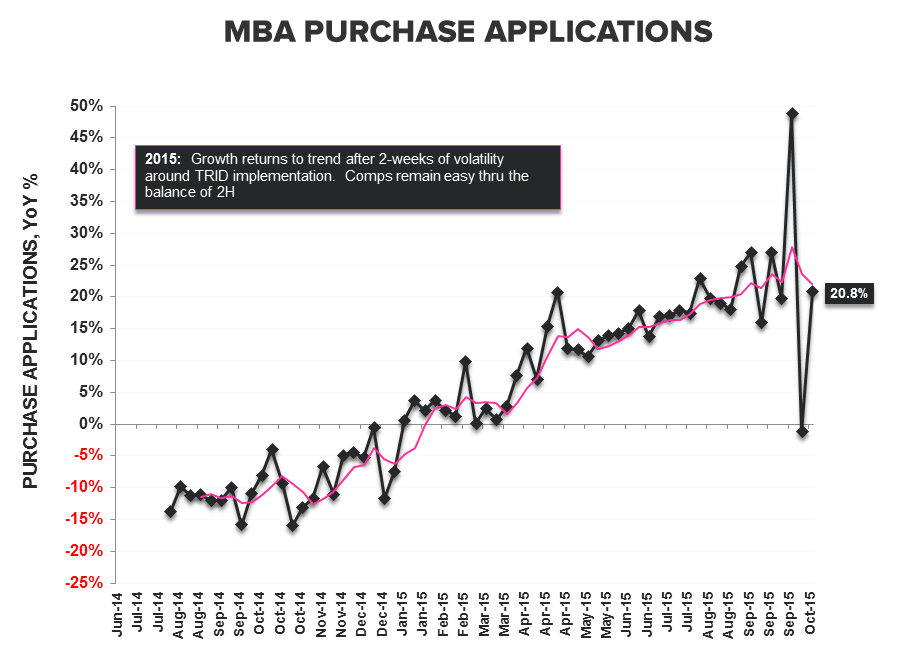

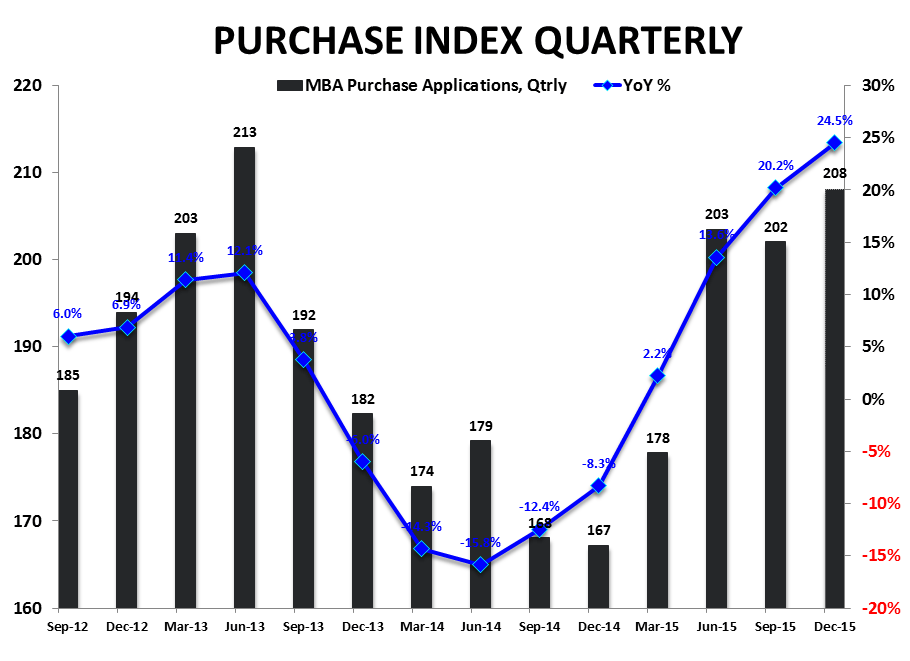

The three-week, TRID catalyzed volatility ride is ebbing and the data is back to looking much like it did for most of 3Q. Purchase Demand rose +16.4% WoW (after falling -34% prior and gaining +27% two weeks ago), taking the index back up to 197.4 – for reference, the Index average in 3Q was 201. On a year-over-year basis growth also re-accelerated back to trend at +20% and, given the continued easy comps dynamics, static activity levels from here imply a similar pace of growth over the balance of the year.

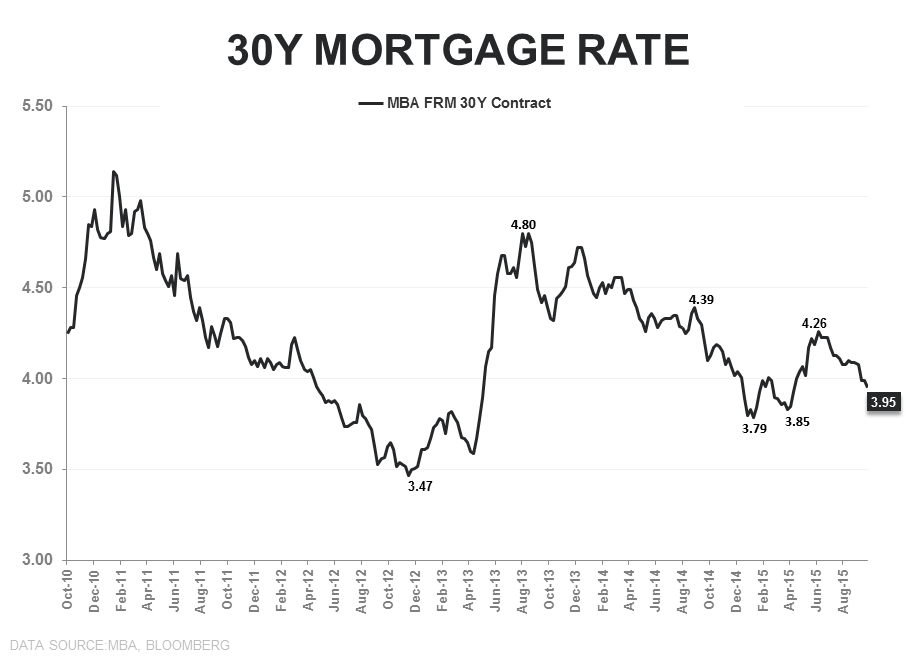

Rates on the 30Y FRM contract, meanwhile, held below 4% for a third consecutive week, declining -4bps to 3.95% and marking the lowest level since the first week of May. At current levels, and ceteris paribus, rates remain a modest tailwind to both HPI and affordability.

So, takeaway = the ongoing march toward housing market normalization (↑ conventional/mortgaged purchases, ↓ cash/investor/distressed sales) and the stable demand environment that has characterized 2015 YTD remains ongoing. We do expect TRID related issues to drive some further chop in the data over the nearer term. Specifically, we expect the Pending Home Sales and New Home Sales numbers for September - both will be reported next week - to benefit from TRID pullforward. The reverse will hold in late November when we get the post-TRID hangover in those series.

About MBA Mortgage Applications:

The Mortgage Bankers’ Association’s mortgage applications index covers more than 75% of mortgage applications originated through retail and consumer direct channels. It does not include loans delivered through wholesale broker and correspondent channels. The MBA mortgage purchase applications index is considered a leading indicator of single-family home sales and construction. Moreover, it is the only housing index that is released on a weekly basis.

Frequency:

The MBA Purchase Apps index is released every Wednesday morning at 7 am EST.

Joshua Steiner, CFA

Christian B. Drake