Lazard (LAZ) is set to report earnings tomorrow in what we expect will be a solid print. With the large $67 billion AT&T/Direct TV transaction having closed in the period and limited proxy disclosure about the associated fee, revenues have upside within the result. Consistent with the rest of the industry, there will also be "constructive" language on the conference call regarding the state of the industry, however we have always ascribed to this guidance only being valuable in the very short run for a couple of quarters.

When zooming out for a broader perspective, the M&A market has chugged along in 2015 but we think expectations of further gains into 2016 are hopeful at best. Looking at merger premiums across cycle, takeout multiples on global transactions are setting new all-time record premiums at 11.9x EBITDA (in 1Q15) and 1.8x sales in the most recent quarter. Historically, the M&A market has been most profitable to investors in the space with low take-out multiples and investing ahead of a jump in merger activity. Simply put, whether M&A participants are strategic or financial, investors are chasing returns with expanding premiums increasing the risk of putting in a high water mark in activity. The prior highs in consideration values were in second half of 2007 with EBITDA premiums of 11.1x in 3Q07 with revenue multiples at 1.7x in 4Q07.

Private equity (PE) participation levels continue to pick up and since we flagged new cyclical highs in PE participation rates last quarter (new highs since the Financial Crisis but not new all-time highs), several blockbuster deals involving financial buyers have been announced. Yesterday, BlackStone purchased Stuy Town/Peter Cooper village from Tishman Speyer for $5.3 billion (in a near mirror valuation of the original '07 sale by Metlife for $5.4 billion) and Dell/Silver Lake is looking to pull in EMC for $67 billion in the biggest technology deal ever. We haven't re-run our PE participation rates for 4Q15 until we get more representative data further into the quarter, but odds at this point call for an even higher percentage of financial buyers of overall activity.

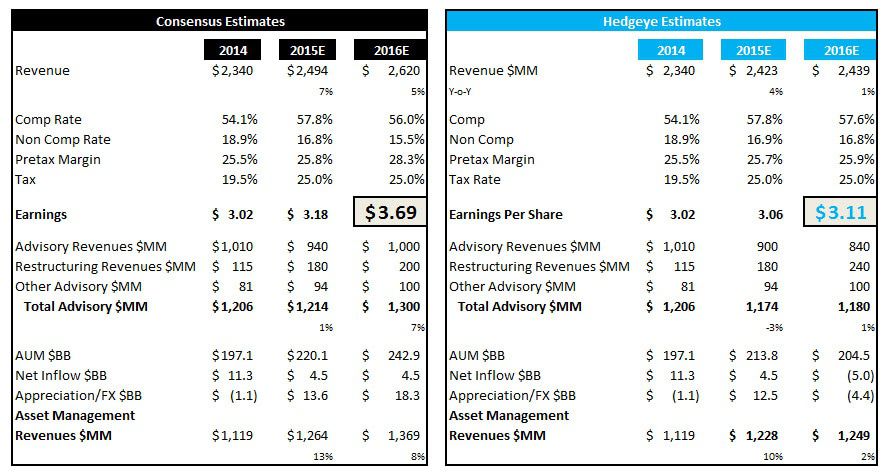

While the top of the market will only truly be available in hindsight, we can comfortably say that expectations for Lazard already reflect a continuation of current trends and that the story is already modeled for growth on growth. Street estimates assume an +8% top line assumption for 2016, which is very healthy considering apparent late stage markers including PE percentages and an all-time high in merger premiums. EPS estimates also sit at an optimistic $3.69 for next year (but have come down from near $4 since the start of the year and our flagging of the asymmetry in the story). Importantly, with the firm's running NOL's from its IPO having now been marked to its balance sheet as of 2Q15, the company's tax regime is moving from 20% to the "high 20's" which imply that the firm will have to increase revenues by +3-9% alone to offset this operating item. Our estimates continue at near ~$3 flat which imply nearly 20% downside to fair value of $36-$39 per share at 12x our estimate. Importantly LAZ shares continue to screen as one of the highest rated in the Financial sector with extremely low short interest and high sell-side ratings/estimates as outlined within our Sentiment Monitor (see Monitor HERE). Thus despite some rationalization of recent out year numbers, shares are still poised for downside in our view.

Deal multiples on EBITDA and Revenue have expanded to new all-time highs including the last cycle peak of 2007. This implies that acquirers are reaching for transactions, a less healthy sign versus moderate, mid cycle valuations:

While a top will only be recognizable in hindsight, 2015 activity has now surpassed 2007 with the recent mega deals in the beverage (Anheuser Busch/SAB Miller) and tech sectors (Dell/EMC):

Cyclical private equity (PE) activity is also being pulled into the market, with PE activity hitting the highest levels since 2007. Over 23% of global M&A announcements involved a PE fund in 3Q15, the highest level since the 30% in 1Q07:

Most recently some of the biggest transactions have been financially driven with private equity participants in the recent Stuy Town/Peter Cooper transaction and also the recent Dell/Silver Lake deal:

Lazard's merger pipeline (all deals "pending" from our data venders) continues to be robust from a dollar value standpoint (however having put in a peak in 2Q14). Currently, we only show 5 absolute deals in Lazard's backlog however the over $100 billion Anhesuer Busch/SAB Miller looms large with $70-$100 million in fees for Lazard and another advisor:

While Street estimates continue to compress we are still close to the $3 per share range flat for 2016 versus Consensus nearly +20% higher. Our fair value at 12x our estimate is $36-39 per share.

LAZ shares continue to screen as some of the highest rated in the financial sector with our Sentiment Monitor applying values to short interest and sell side ratings. The higher the Sentiment number, the lower the short interest and the higher the sell side rating:

Private Equity Historically Marks the Peak

LAZ - As Good As It Gets...Modeled For Perfection

Moelis (MC) Pre-IPO Black Book

GHL - Removing Greenhill From Best Ideas list

GHL - The Best Way to Capitalize on an Improvement in M&A

Hedgeye Black Book - M&A Market to Positively Inflect in 2014

Jonathan Casteleyn, CFA, CMT

Joshua Steiner, CFA