Hedgeye Retail Idea List

This Week's Changes

DLTR: Graduated to the top spot on our Long Bench. Seemingly not the kind of name we'd like at this point of the economic cycle. But we think there's an asymmetric setup here in the wake of the Family Dollar acquisition that works even in a slowing economy. Stay tuned for more on this as our vetting continues.

PIR: We turned the TRADE indicator from negative to positive -- now positive on all three durations. We had been concerned heading into the latest quarter, but think that expectations for the next quarter and FY are very much in check.

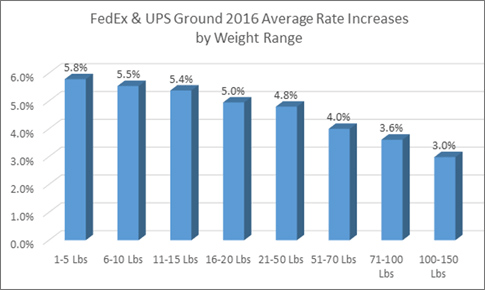

UPS raising shipping rates again -- And retail margin expectations are STILL too high.

(http://www.wsj.com/articles/ups-targets-discount-sharing-with-new-fee-on-retailers-1445035798)

There is a lot going on with UPS and Fed Ex pricing with fuel surcharges (going into effect in Nov), ground rate hikes (December), and 3rd party fulfillment surcharges -- the squeeze is on for retailers as free shipping thresholds come down to $0. Both UPS, FedEx, and even USPS have been vocal about the dilutive impact from growing e-commerce sales which are more expensive to fulfill because of neighborhood deliveries. But unlike retailers who we think will more and more use free shipping (and returns) as an offensive weapon to try to hold onto market share, the shipping duopoly has the clout to pass on increasing costs to its retail partners.

If this were a different part of the economic cycle, we wouldn't make much noise about this. But the fact of the matter is that without higher freight costs, retail EPS growth is decelerating from a mid-teens rate earlier this year to zero in 4Q/1Q. The problem is that the consensus has EPS growth reaccelerating from a lsd rate to 10%. The consensus is wrong.

Image Source: E-commerce Bytes

WMT - Federal probe into Wal-Mart operations in Mexico has found minimal offenses. The case and fines are likely to be much smaller than initially expected.

(http://www.wsj.com/articles/wal-mart-bribery-probe-finds-little-misconduct-in-mexico-1445215737)

TFM - The Fresh Market is working with Apollo Global Management to explore a buyout.

KATE - EJ Victor to launch Kate Spade New York furniture collection

(http://www.furnituretoday.com/article/524851-ej-victor-launch-kate-spade-new-york-collection)

RetailNext forecasts Holiday sales at +2.8%

(http://www.retailingtoday.com/article/retailnext-holiday-sales-expected-climb-only-)

AMZN - Amazon looking to buy stake in India on demand home services company Housejoy

H&M Opens First Store in South Africa

(http://wwd.com/retail-news/mass-off-price/hm-opens-first-store-in-south-africa-10264590/)