We are becoming increasingly concerned about Chipotle (CMG) and the headwinds that it will face in the coming quarters.

We took CMG off the Hedgeye Restaurants Best Ideas list as a LONG and moved it to the LONG bench on 9/30/15 see our note HERE.

In the note we suggested that CMG is getting long in the tooth and that it will experience some growing pains in the near future.

- Quality real estate is getting harder and more expensive to get

- Are the 2015 supply chain issues a one off experience?

- Slowing sales trends might not end in 3Q15

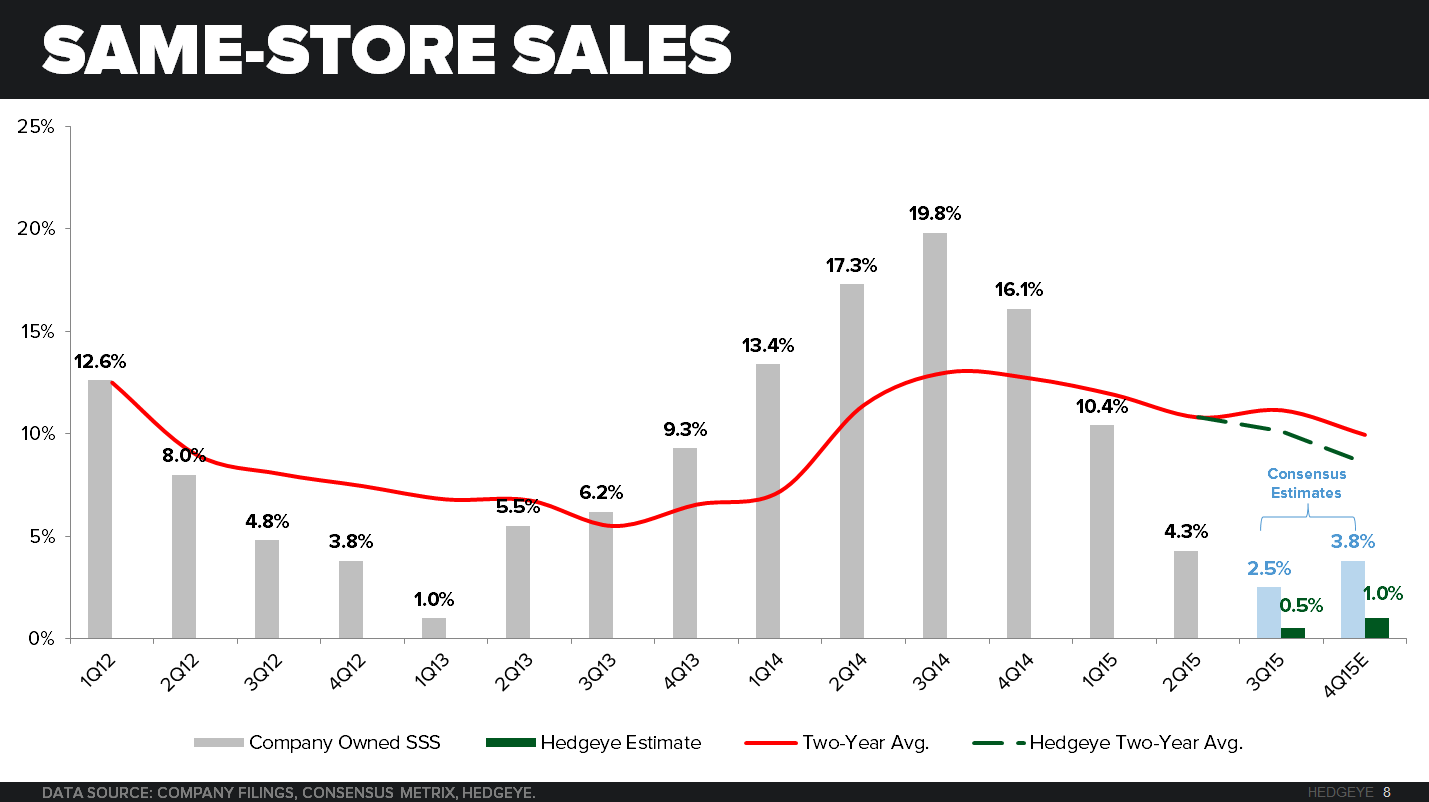

Ahead of the earnings announcement on this Tuesday, October 20th after market close, we are adding it to the short bench. The table below summarizes what the street is looking for:

In addition to our original concerns, we believe the company may post below trend same store sales due to a number of macroeconomic factors.

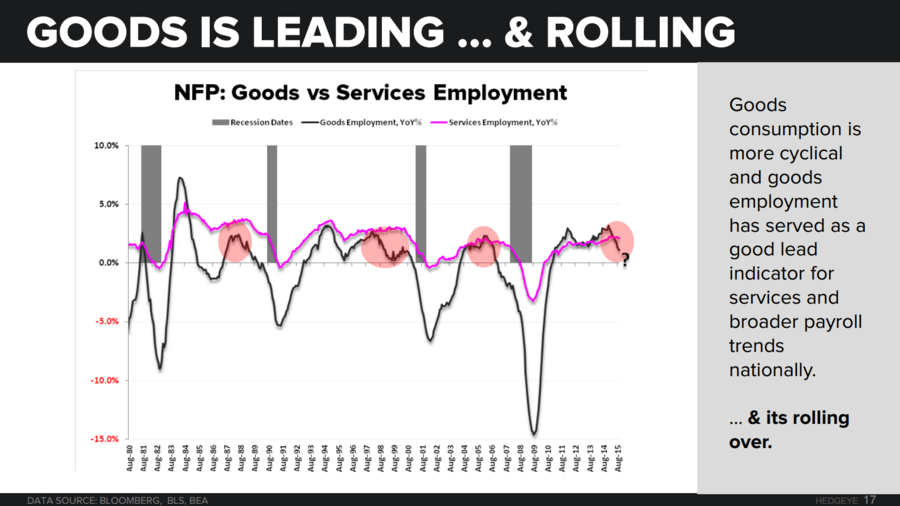

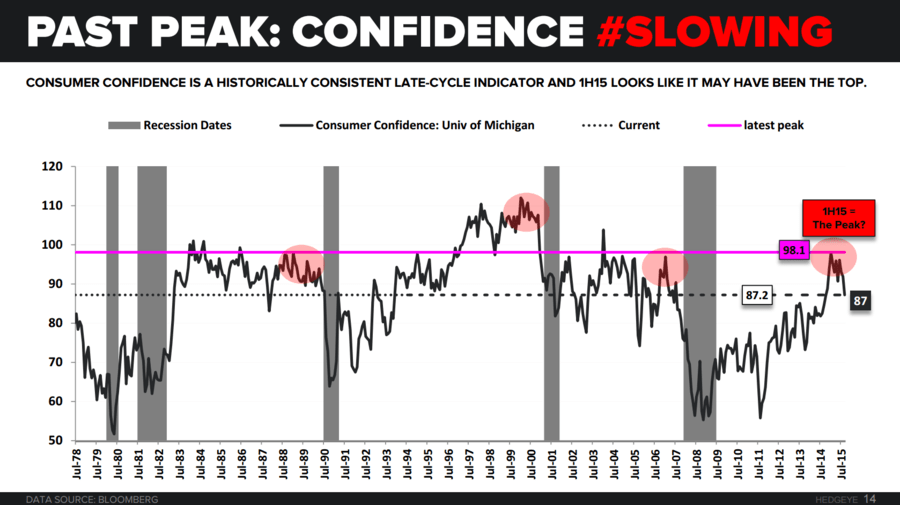

1) The consumer is rolling over

A) Jobs

B) Consumption

C) Consumer Confidence

D) Industry Sales Slowing

2) Deflation is bad for Restaurants in general and CMG is not immune.

A) Beef, Chicken and Pork prices are all trending lower, taking away Chipotle’s ability to price effectively.

B) An added problem is significant labor inflation that we are starting to see in major metropolitan areas. This will begin to trickle through the nation and really begin to affect margins.

C) CMG same-store sales versus CPI Pork YoY % change.

3) Street estimates call for a recovery in sales – this looks to be aggressive. Additionally the company is running up against very difficult YoY comparisons.

Hedgeye estimates are below street estimates

4) CMG needs 3% same-store sales to leverage labor costs. With slowing same-store sales and accelerating labor inflation, current margin estimates look to be aggressive.

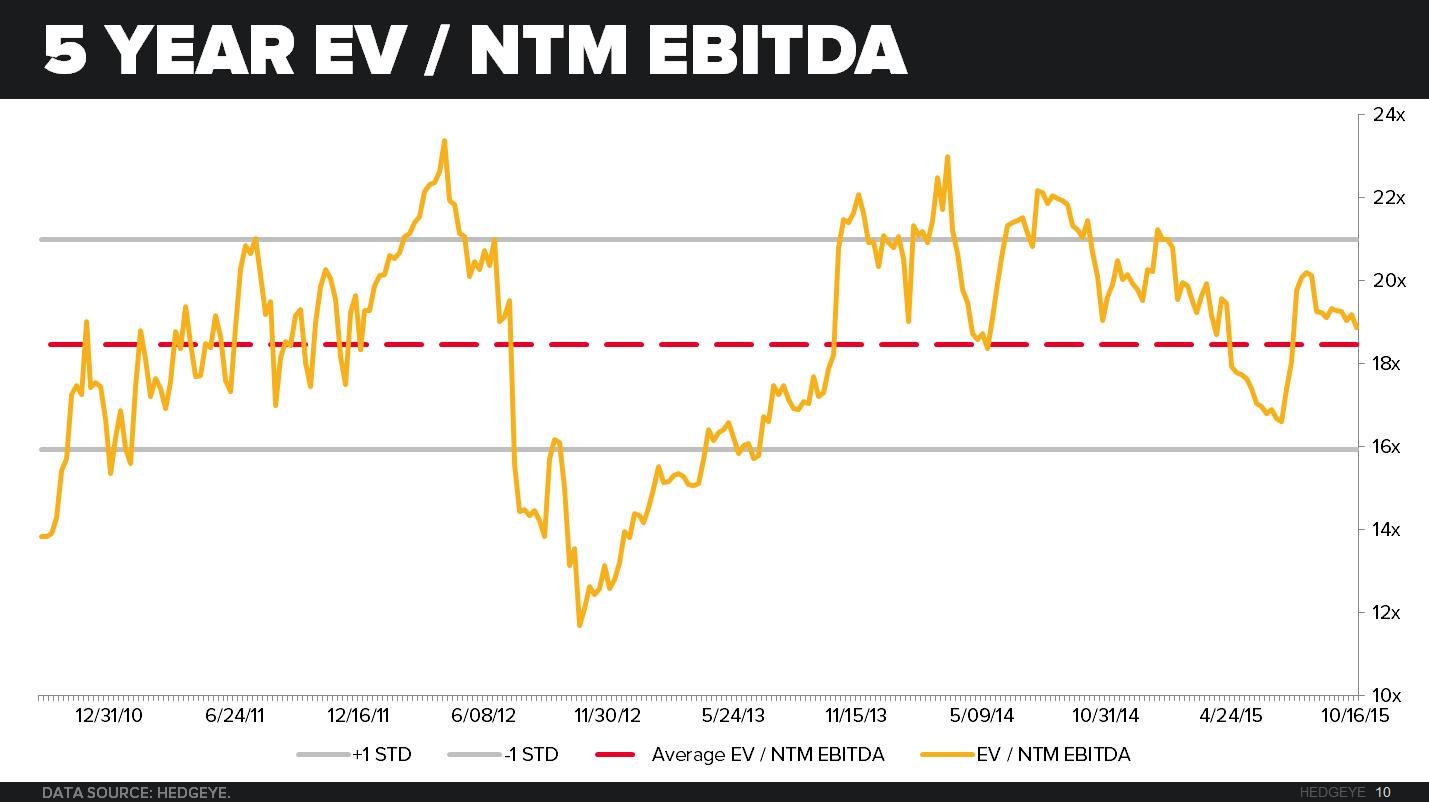

5) A multiple contraction is likely, given the current macro environment. And could get worse if sales miss current expectations.

Hedgeye Restaurants Best Ideas List

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst