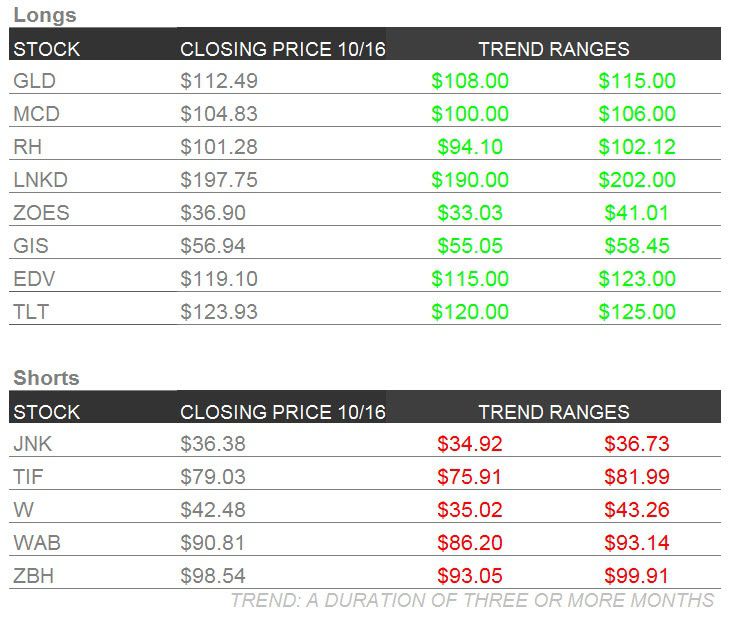

Below are our analysts’ updates on our thirteen current high conviction long and short investing ideas. Please note that we removed Penn National Gaming (PENN) and Financial Engines (FNGN) this week. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this. Hedgeye CEO Keith McCullough’s updated levels for each ticker are below.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

GIS

General Mills is now a couple months into their launch of Gluten Free Cheerios. Besides one minor recall coming out of their Lodi, CA facility, all signs point to the launch being successful. Consumers are responding well on social media, pleased that such a big company is making big changes to improve the quality of their food.

Annie’s continues to perform well in the marketplace as they expand distribution with the help from General Mills’ sales team. Many consumers were lashing out when GIS acquired Annie’s one year ago, saying that GIS would tarnish the great brand. But this simply is not the case. GIS has nourished this company, leaving it to operate in Berkley, CA. Annie’s employees, including former CEO John Foraker have nothing but great things to say about the experience and what GIS has done to allow the team to grow Annie’s their way.

GIS continues to be on our Best Ideas list especially in these volatile markets, where big-cap and low beta reign supreme.

ZOES

Nothing has changed at Zoës Kitchen. We still love the management team and the concept of the restaurant. But due to the macro-driven market, high beta, low-cap names such as ZOES have fallen out of favor.

If you are a "buy and hold" type of investor this is a name you want to be in for the long run, especially at these values. This company has a long runway of growth which we believe is only just in the beginning stages.

WAB

To view our analyst's original note on Wabtec click here.

In case you missed it, GE received orders for 3 locomotives in 3Q 2015. No, that's not a misprint. That's three, down from a high comp of 1,131 in 3Q 2014 and a typical run rate of more like 70-250. Locomotives are going into storage and mines are not expanding, leading to weak demand.

Does that bode well for Wabtec? We'll let you decide. See the chart below.

MCD

To view our original note on McDonald's click here.

McDonald’s (MCD) reports 3Q15 earnings Thursday, October 22nd before the market opens, with a conference call at 11:00am ET. We are expecting strong sequential improvement in performance globally. We look forward to giving you an update on the company’s performance next week, but this week we wanted to focus on the ‘Looming Crash in Beef.'

On Thursday, October 15th, we held a thought-leader call regarding the declining price of beef and how long it will continue. Prices have sky rocketed in recent years and are now standing at more than two standard deviations above the 30 year average. If you look at the chart below, with the information we gained from James Robb, a Director at the Livestock Marketing Information Center (LMIC), we believe a 50% decline down to historical averages is well within the realm of possibilities.

The cattle cycle is in its early stages and inventory is projected to rise over the next few years. Rising inventory means that as the cattle ages more heifers will be up for slaughter, adding to the supply in the market.

Declining beef prices will be a major tailwind for McDonald’s as they navigate their turnaround.

W

To view our analyst's original report on Wayfair click here.

Right now, coverage of Wayfair is split about 50/50 between Retail and Internet analysts. The right approach is simply to use both, Internet and "old school" brick and mortar retail.

But you can rest assured that Internet analysts did not hear the following remarks Gary Friedman delivered during the RH 2Q15 earnings presentation. Take a look below. We think his argument sheds some light on our bearish Wayfair thesis.

"How many online only retailers have reached $1 billion in revenues and have positive net income? For the 2014 fiscal year the answer would be two, and just barely.

Many investors and analysts are seduced by the notion of a capital light retail strategy, and completely overlook the fact that the ongoing advertising expense to market an invisible online store is an unproven and, we believe, unsustainable model.

Also interesting is when investors or companies tout their online growth rates, believing it to be the more profitable channel. First, it's obvious that growth rates in a new undeveloped channel will grow faster than a mature one. It's also somewhat irrelevant. A big percentage of a small number is still a small number. Shifting transactions from one channel to another does not change the economics.

We know of no store-based retailer that has significantly increased their operating margins by growing online faster than retail. The important question is, Why would anyone conclude that online is more profitable than retail?

As we've said before, it's not about Physical versus Digital, as A.T. Kearny eloquently puts it, it's about Physical with Digital.

Where the transaction takes place is a lot less important than where the decision to purchase is derived. Unless you're positioning to be the low price leader, or you're selling replenishable commodity products, like laundry detergent, paper towels, groceries and the thousands of things we don't sell.

That's why we believe when the dust settles, our strategy of undertaking what is arguably the most significant retail store transformation in history, will prove to be the right one. That the physical manifestation of an aspirational brand in an inspiring three dimensional environment, will prove to be more important than an invisible one dimensional online store.

Retailers who demonstrate true product leadership with an inspiring physical presence and a fully integrated, channel agnostic strategy will win."

TIF

To view our analyst's original report on Tiffany click here.

Sentiment for Tiffany is sitting at all-time highs. Our Hedgeye Sentiment Monitor (Below) triangulates Buy Side Short Interest, Sell Side Ratings, and Insider Activity to give a graphical representation of sentiment around the stock. A low score indicates negative sentiment and is a bullish signal. A high score indicates positive sentiment and is a bearish signal.

Bottom line right now: Back half and 2016 estimates are too high, the stock is trading near a peak multiple (18.5x), on peak margins (21%); peak earnings ($4.20E TTM and NTM) that aren't growing; and peak returns (18%). There is still room to run for this short idea.

RH

To view our analyst's original report on Restoration Hardware click here.

Restoration Hardware opened its new Full Line Design Gallery at the Cherry Creek Shopping Center in Denver this week. This is another anchor property -- using 53,000 feet of the 90,000 left vacant by Saks at Cherry Creek.

RH is taking up the size of its stores from an average of 8,000 square feet to about 40,000+ for its new stores – and productivity rates on these new assets are headed higher. In the old stores, RH could only show 10% of its assortment, while in the newer format stores, the company is showcasing better than 75%. Consumers can’t (and don’t) buy what they don’t see.

RH Cherry Creek

Image source: CBS Denver

LNKD

To view our analyst's original report on LinkedIn click here.

Our tracker suggests an improving selling environment into 3Q15, reinforcing our view that management was crying wolf with its organic guide down. Our LinkedIn JOLTS tracker is accelerating through the first two months of 3Q15, suggesting an improving selling environment.

As mentioned here before, we remain long LNKD into its next earnings release on October 29th. We expect a clean beat and raise. We expect this will be a positive catalyst for the stock.

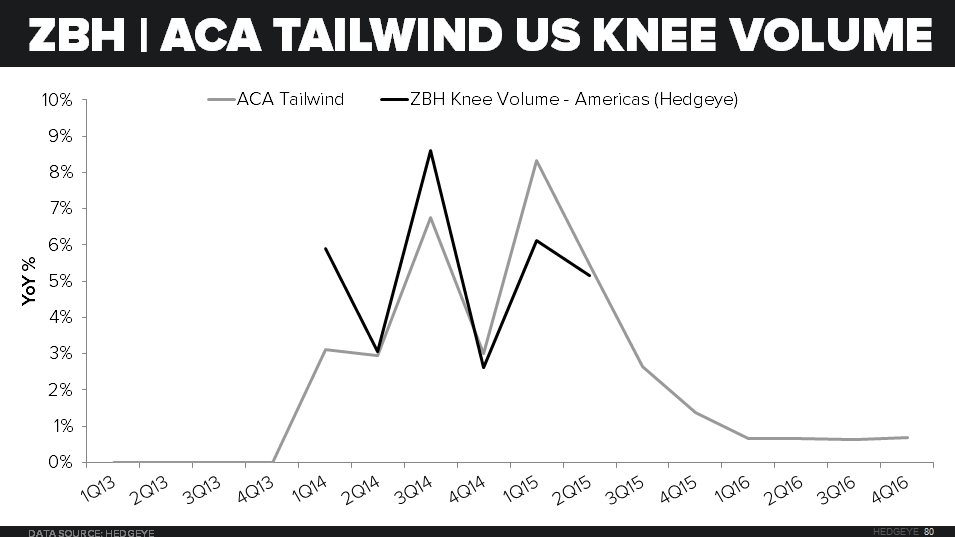

ZBH

To view our analyst's original report on Zimmer Biomet click here.

In case you missed it, check out this short clip of Healthcare analyst Tom Tobin on The Macro Show this week, in "Short Healthcare with Impunity?"

We got the first glimpse of U.S. knee market growth for 3Q15 this week, with JNJ reporting U.S. knee market growth of +2% YoY. This is a deceleration from +5% in 2Q15 and consistent with commentary we hear around weak volume from Orthopedic Surgeons.

We believe ACA was a meaningful tailwind to U.S. knee volumes, with pent-up demand among newly insured driving +10% incremental volume growth.

This tailwind will prove to be a meaningful headwind in coming quarters as the #ACATaper takes full effect, which will also weigh on Zimmer Biomet. We are already seeing the impact with HCA reporting disappointing volume and the Healthcare JOLTS series falling to ~12% YoY in August, after averaging 25% YoY for the first 7 months of the year.

TLT | EDV | GLD | jnk

To view our analyst's original report on Junk Bonds click here.

If you needed any further proof, Friday’s industrial production report reminded us of the slowdown in cyclicals. As Keith McCullough emphasized in a short note to clients Friday:

“The rate of change in US Industrial Production just slowed to its slowest rate of change of the year (-0.2% sequentially to 0.4% y/y) and is about to go negative. The comps only get tougher from here (underlined in green – that was the peak of the cycle).”

The #SlowerForLonger theme from Hedgeye Macro has been consistent and straightforward. Our pivot in advance of the most recent jobs report to get long of gold and stay out of the way short-side on commodities turned out to be a good position.

We removed the U.S. dollar (UUP) from the Investing Ideas long side on August 28th, and since then UUP has gotten tagged for -2%. By comparison, GLD is +4.2% since it was added to the long-side on September 2nd. Stick with this trade. There’s nothing gold likes more than down dollar, down rates.

Again, what causes down dollar, down rates? Well, more confirmation that growth is slowing. The Q3 GDP number will be reported on October 29th and we expect this number to slow on both a Y/Y and Q/Q SAAR.

Growth expectations have been correctly revised, but there’s still a good amount of room between Hedgeye estimates and consensus. We are expecting GDP in a range of 0.1%-1.5% for Q3 and another 1-handle in Q4. If that proves accurate, flatter goes the Treasury curve (TLT, EDV), wider goes high yield spreads (bad for JNK), and down goes the USD (GLD).

Stick with us closely regarding the relative central bank policy moves from abroad, as we expect Mario Draghi to counter growth slowing data in Europe with more QE. That would be dollar bullish and likely a headwind for Gold in the short-term.