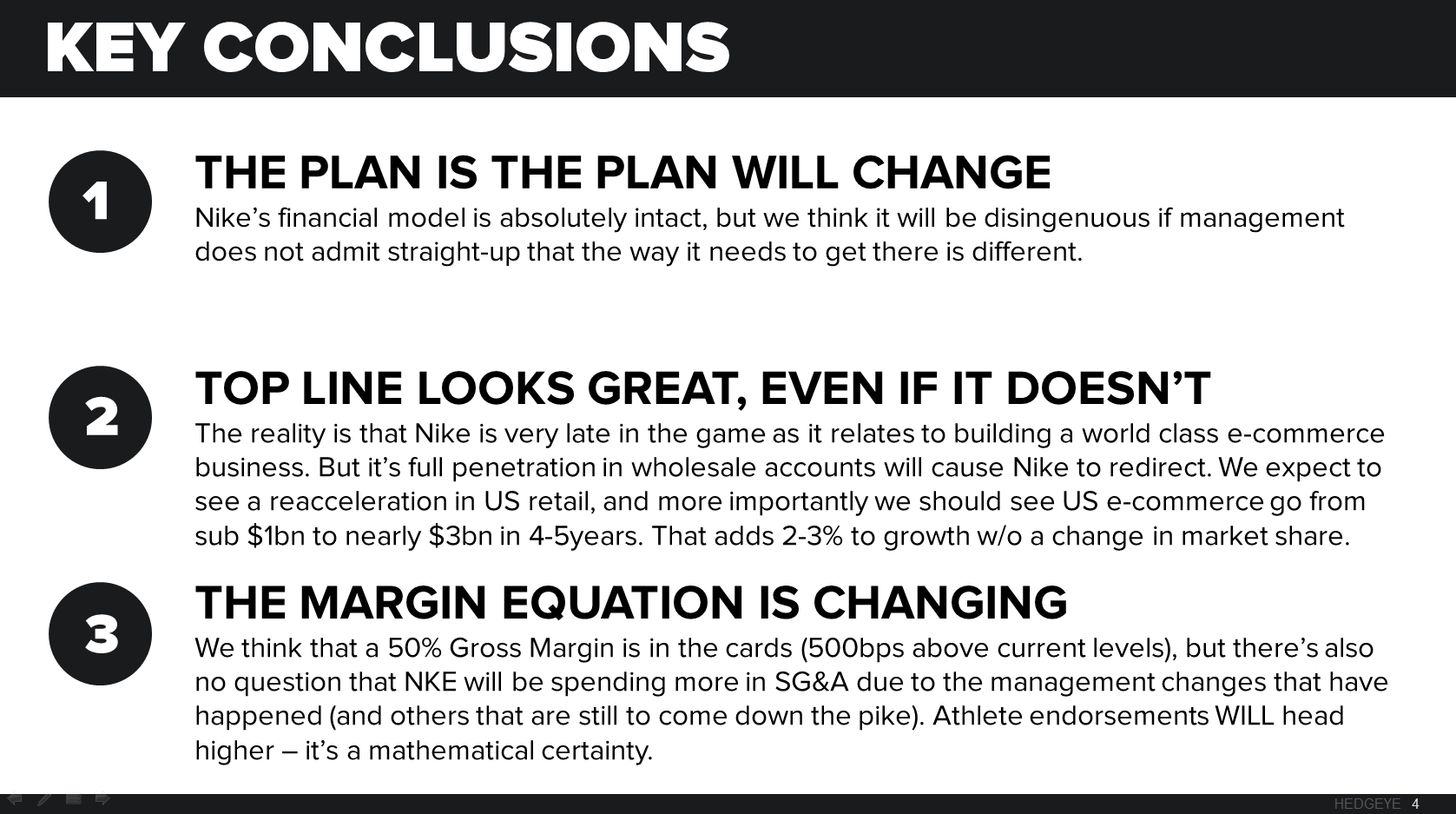

We’ll be back after the dust settles with more detailed thoughts and analysis on Nike’s Investor Day. But in seeing the presentations, we’re pleased to see that so much of it was spot on with what we outlined in our 86-page Black Book on Monday. Here’s the LINK. This is what was most notable to us…

- Revenue: The $50bn target by 2020 was impressive – especially on a day where Wal-Mart told us that it won’t hit 2015 EPS again until 2020. That represents about a 10% CAGR. We think this is a slam dunk for Nike.

- Sounds like bold statement from us that 10% growth annually is a slam dunk. But keep in mind the P&L impact of the shift in mix to DTC/e-comm. This shift in mix alone gives Nike 200-300bps in growth per year. That means Nike needs to grow end-market demand by closer to 7% per year. This category grows globally at 4-6% per year, and Nike is a perpetual net share gainer.

- E-comm targets of $7bn by 2020, 42% CAGR, are not just appropriate, but they are flat-out low. We think they’ll hit that level at least a year early. Why be so conservative? What message do you think it sends to Foot Locker, Finish Line, Dick’s, Hibbett, and the other retailers in the US that have a swoosh on 75% of what they sell? A really bad one. Nike set a big aggregate revenue number, but will get there by way of beating the e-comm number.

- The Financial Model has changed. It was our contention that Nike had to admit that the Model that has served it well for 15 years is changing. While it did not announce that broadly, the model definitely changed. It took up revenue growth, took up GM expansion to 30-50bp/year (which means it thinks it can do nearly twice that), and lowered expectations for SG&A leverage on a better sales number. Why? Aggressive shift to e-commerce (again – this hurts traditional wholesale accounts) is very sales and GM-accretive, but the cost of growth is going up by way of manufacturing innovation and athletic endorsements.

- Manufacturing Innovation? This is something we’ve been talking about for a while now – that Nike will reverse engineer how shoes are made – like what it did with FlyKnit. This will allow the company to accelerate on-site manufacturing (which it still played down today), 3-D printing, and both take capital out of its supply chain while driving ASPs higher to sell through NKE-owned distribution (retail and e-comm). The interesting thing is that Nike announced a partnership with FLEX to accelerate this initiative instead of go solo. What’s funny is that the partnership isn’t really new. Nike has been doing business with FLEX for at least 5 years. But it sounds like they’re doubling down on one another.

A Slide From FLEX Presentation:

- Management: To its credit, while we’re still not thrilled with each individual member of management, this team sounded amazingly confident – more so than we’ve ever heard or seen them in 20 years. This sounded to us very much like a team that will not miss its goals come hell or high water. #respect