On The Macro Show earlier this morning, Hedgeye Financials analyst Josh Steiner joined CEO Keith McCullough to discuss key market developments, including a granular look at the weak quarter JPMorgan (JPM) just put up.

* * *

The conversation shifted gears when McCullough responded to a subscriber’s question during the interactive Q&A portion of the show regarding how far along the U.S. is in the current economic cycle.

“[The U.S. expansion] is long-in-the-tooth and slowing,” Keith said. “It’s already showing up in the cyclical and industrial sectors…You don’t have a consumption recession, yet, but the employment and consumption pieces [of the economy] are clearly rolling over as they do at the end of every cycle.”

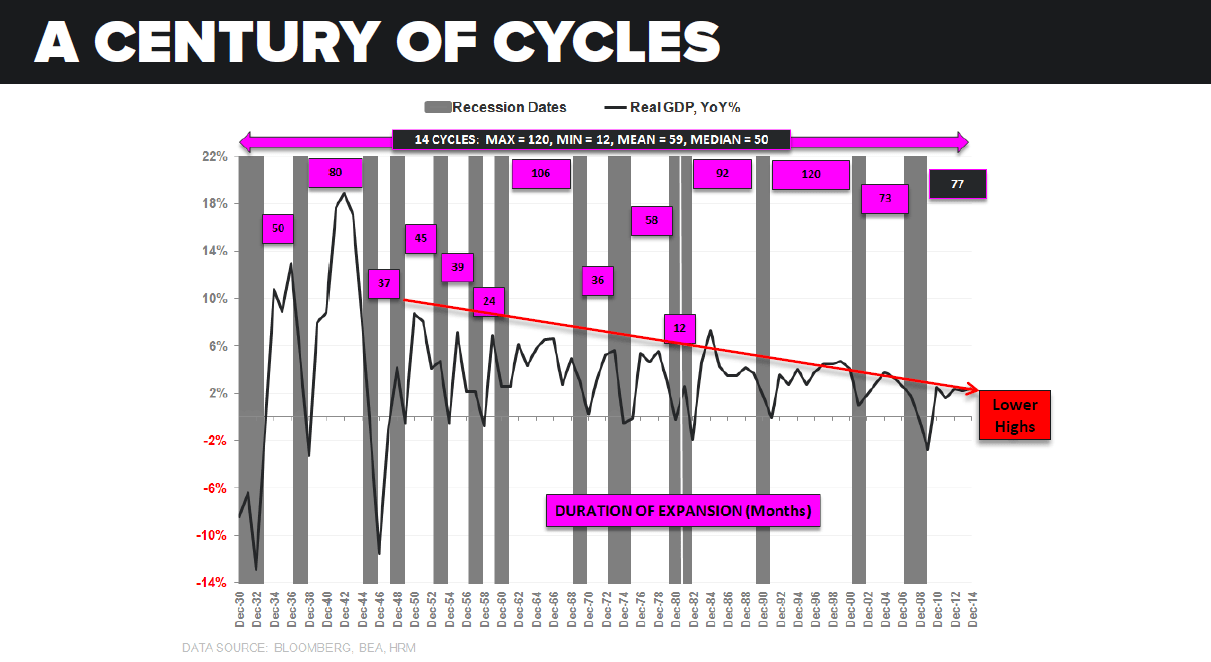

To prove his point, Keith pulled up a thought-provoking slide from our macro team’s recent 73-page presentation of our top 3 Q4 2015 Macro Themes.

As you can see in the slide below, it shows the past 85 years of economic cycles. Our current expansion stands at 77-months. To put that in perspective, the median expansion typically lasts around 50-months.

Click image to enlarge.

In other words, we’re in the twilight of U.S. economic expansion. Hence, our new macro theme #SuperLateCycle. (Please ping sales@hedgeye.com if you’re interested in getting access to our macro presentation.)

“What comes after the SuperLateCycle?” Keith asked rhetorically.

A recession.