Our Hedgeye Housing Compendium table (below) aspires to present the state of the housing market in a visually-friendly format that takes about 30 seconds to consume.

Today's Focus: MBA Mortgage Applications

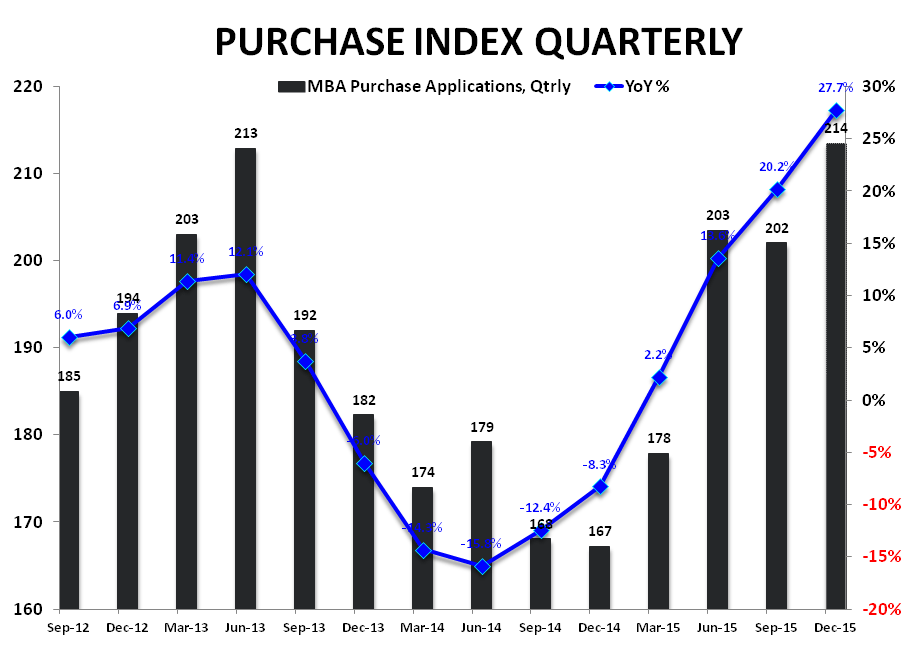

After jumping +27.4% ahead of the impending TRID implementation, post-implementation Purchase activity more than retraced the gain, declining -34% in the latest week. On a year-over-year basis, purchase demand declined -1.2%, marking the first YoY decline since the start of the year.

As we highlighted last week (Purchase Demand is Good, But Not That Good), it’s likely we continue to see excessive chop in the high frequency data over the next few weeks as lenders go live with implementation and purchase agents attempt to risk manage any early bottle-necks. Moreover, the demand pull-forward will likely serve to juice both the New and Pending Home Sales figures for September as the bolus of pre-TRID demand flows through the reported volume figures. However, similar to the party-hangover dynamic observed across the Purchase application data the last two weeks, the illusory gain in September is likely to decrement reported October demand by a similar magnitude (late November releases).

Handicapping the precise impact of the regulatory changes to transaction volume in the nearer-term is a largely quixotic pursuit – we’re content to let the data breath for another few weeks before taking a directional view on the underlying level of demand.

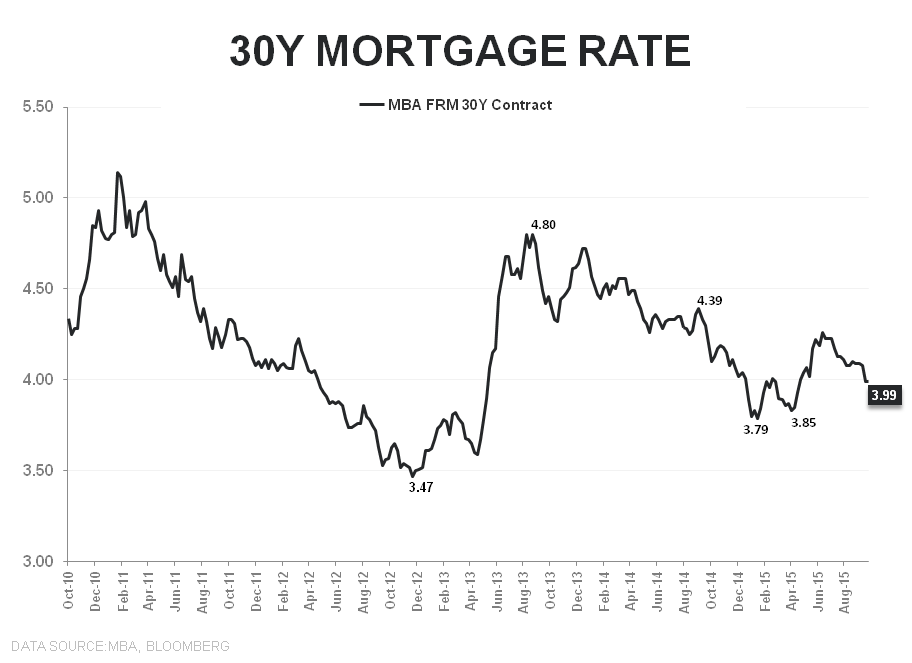

Rates, meanwhile, held below 4% for a second consecutive week as our Macro call for slower-and-lower-for-longer (globally) continues to manifest. At current levels, rates remain a modest tailwind to both HPI and affordability.

About MBA Mortgage Applications:

The Mortgage Bankers’ Association’s mortgage applications index covers more than 75% of mortgage applications originated through retail and consumer direct channels. It does not include loans delivered through wholesale broker and correspondent channels. The MBA mortgage purchase applications index is considered a leading indicator of single-family home sales and construction. Moreover, it is the only housing index that is released on a weekly basis.

Frequency:

The MBA Purchase Apps index is released every Wednesday morning at 7 am EST.

Joshua Steiner, CFA

Christian B. Drake