“For no particular reason I just kept on going. I ran clear to the ocean. And when I got there, I figured, since I’d gone this far, I might as well turn around, just keep on going. When I got to another ocean, I figured, since I’d gone this far, I might as well just turn back, keep right on going.”

–Forrest Gump

Last night, the Democratic contenders for President held their first debate. The conservative-leaning website Drudge Report ran a poll that showed overwhelmingly that Senator Bernie Sanders won the debate, according to 59% of the respondents. Meanwhile, only 7% of respondents indicated they believed the current front-runner for the nomination, former Secretary of State Hillary Clinton, won the debate.

Despite the Drudge poll, by and large, the punditry from the National Journal to the New York Times declared Clinton the winner. Arguably though, there was another winner at least in terms of getting attention during the poll, namely Donald Trump. With his active tweeting during the campaign, Trump seemed to have garnered as much attention as many of the candidates on the stage.

Some of his zingers included:

“Putin is not feeling too nervous or scared. #DemDebate”

“The trade deal is a disaster, she was always for it! #DemDebate”; and

“Notice that illegal immigrants will be given ObamaCare and free college tuition but nothing has been mentioned about our VETERANS #DemDebate”

According to reports, Trump picked up 60,000 new followers (about 4 times as many as Clinton) during the debate. Last night, Trump’s top tweet had nearly 11,000 retweets and 17,000 favorites. Clinton’s biggest tweet? Just 3,300 retweets and 4,800 favorites.

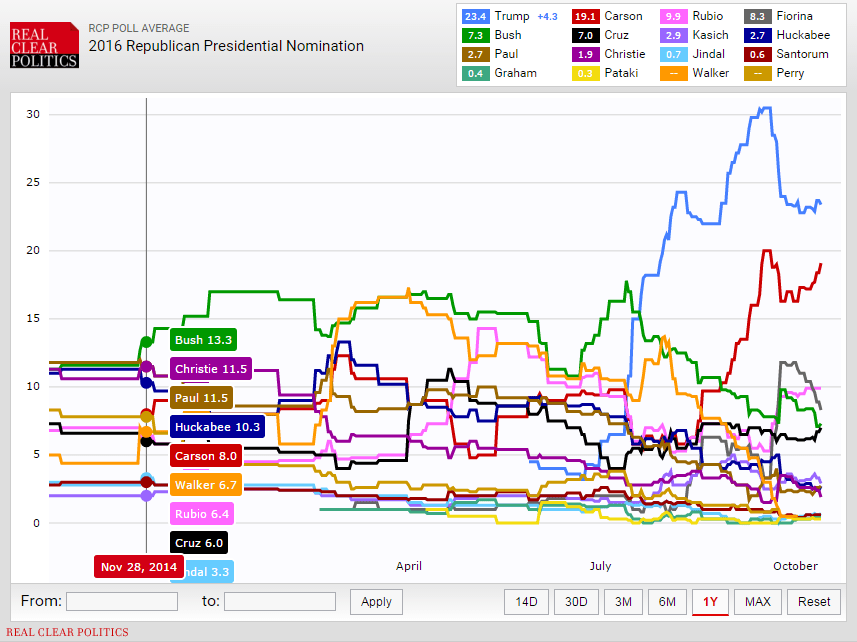

In terms of how he is actually doing, Trump is still leading the Republican nomination race, but as the Chart of the Day highlights, the polling aggregates are clearly showing waning enthusiasm for his nomination in the way of lower highs of support. In particular, Ben Carson is now within 4 points of Trump. In fact, in the most recent poll from Fox, Carson is within 1 point.

So, is the Trump candidacy a bubble? Well, if you look at the Chart of the Day, it certainly bears some comparisons to over enthusiasm we see in the stock markets at times. In recent cycles, the candidates that are leading at this juncture typically have not gone on to win the nomination or Presidency. In particular, in 2004 Clark was up +5, in 2008 Clinton was up +25.6, in 2012 Giuliani was up +10.7; and in 2012 Romney was up +2.4.

So are Trump’s best polling days behind him? It does seem likely (although the same can probably be said for Clinton). But certainly he is adding some color and excitement to the race. So what the heck, we say Run, Donald Run!

Back to the Global Macro Grind...

We uncovered an interesting data point this morning relating to shipments leaving U.S ports. Not to be confused with the "empty suits" we sometimes see in politics, empty containers leaving U.S. ports are surging this year. In fact, the Port of Long Beach, CA handled almost 200,000 empty containers in September, which represented 1/3 of the total shipments that went through the port.

Between Long Beach and Oakland, exports of empty containers have outnumbered those loaded with exports for 8 straight months. While this is growth, it’s not the kind we want to be too excited about. This is obviously indicative of global demand that is anemic at best, especially given the strength in the U.S. dollar. In aggregate, U.S. exports are expected to decline this year for the first time since the financial crisis.

In line with the increasing plethora of global growth slowing data points, the German Economic Ministry came out and cut their 2015 GDP growth estimate from 1.8% to 1.7%. Certainly not a meaningful shift, but also telling since it’s the Germans and it is indicative of a view that growth is slowing in Q4 more than expected. As of now, they are leaving the 2016 GDP growth estimate intact . . .

If the Germans (and J.P. Morgan for that matter!) cutting estimates weren’t enough, European industrial production came in at disappointing 0.9% y-o-y growth for August. This is compared to expectations of 1.8% y-o-y. As well, CPI’s across the continent are coming well below ECB target rates this month (France +0.1%, Spain -1.1%, Italy +0.2%, and Finland -0.6%).

Slow Europe slow!

Speaking of Europe, next week we will be re-introducing Spain as one of our top sovereign short ideas. Hedgeye special contributor Daniel Lacalle will be leading the call. Lacalle is a renowned European economist, who previously worked at PIMCO and was a PM at Ecofin Global Oil & Gas Fund and Citadel. He is the author of Life In The Financial Markets and The Energy World Is Flat and a lecturer for the IE Business School and Master MEMFI at UNED University.

Spain’s equity markets have underperformed many of its European peers in the year-to-date and are currently down -1.77%. But with many Spanish economic data points coming in worse than expected, an election that is looming in mid-December, and a 10-year bond yield that remains priced to perfection at 1.80% (the same yield as the U.K.), we think there is increasing opportunity to generate alpha on the short side of Spain. The call will be help on Wednesday October 21st at 11am eastern. Ping for details.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.98-2.12%

SPX 1

DAX 98

VIX 15.94-24.61

Oil (WTI) 44.34-48.01

Gold 1140-1175

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research