I think I’m more bullish than anyone, on bonds – long-term Treasury Bonds, that is.

It’s simple.

#SuperLateCycle is what it is and this morning’s economic data from German ZEW (OCT) slowing to 1.9 from 12.1 to only the second #Deflation (year-over-year negative) print for CPI in the UK since 1960.

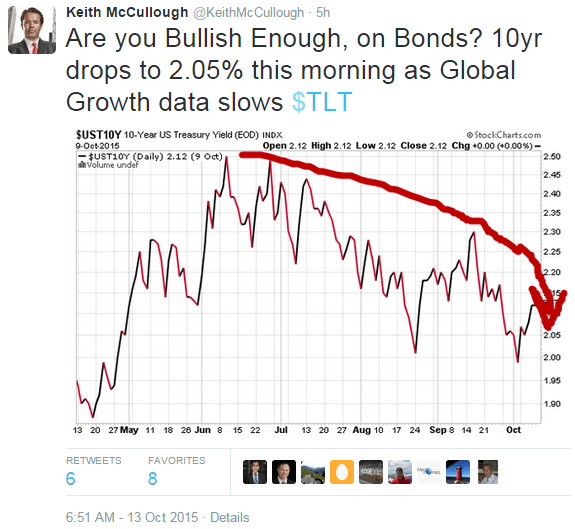

Check out the chart below.

Or (God forbid), we remember the recent (awful) U.S. jobs report. It all adds up to a 2.05% 10-year U.S. Treasury and falling.

* * *

Editor's Note: If you're interested in getting a step or two ahead of the consensus herd, we encourage you to take a closer look at our suite of contrarian investment products.