Free Shipping (Now Returns) As Offensive Weapon

(http://www.wsj.com/articles/more-retailers-offering-free-shipping-on-online-orders-1444402553)

49% of retailers are no longer charging for returns and that's a tough price tag to swallow for a lot of companies in this space -- especially those with a small average basket. We think that both sides of the fulfillment of the equation, shipping and returns, for things like apparel/footwear/home décor are headed to 100% free 100% of the time by the end of FY16. That starts this holiday as retailers use 'free shipping' promotions as an offensive weapon. Unfortunately, for almost everybody except the bullet-proof content-owners of the world (i.e. Nike) such a move will be dilutive to margins. Even worse news is that if they don’t play ball, then there’s risk to the top line (i.e. if either KSS or JCP opts-in to the free-shipping game, they both lose).

Here is how the margin math works for 4 retailers at various ends of the department store spectrum. JWN gets up to a 1500bps higher gross margin than KSS on a straight on-line sale, 1300bps in the case of a partial return, and a both sit at a -10% margin on a full return. High end, high ticket, and solid content retailers can play online. Otherwise it's an extremely dilutive channel with even more cost pressure as the free shipping and return threshold move towards $0.

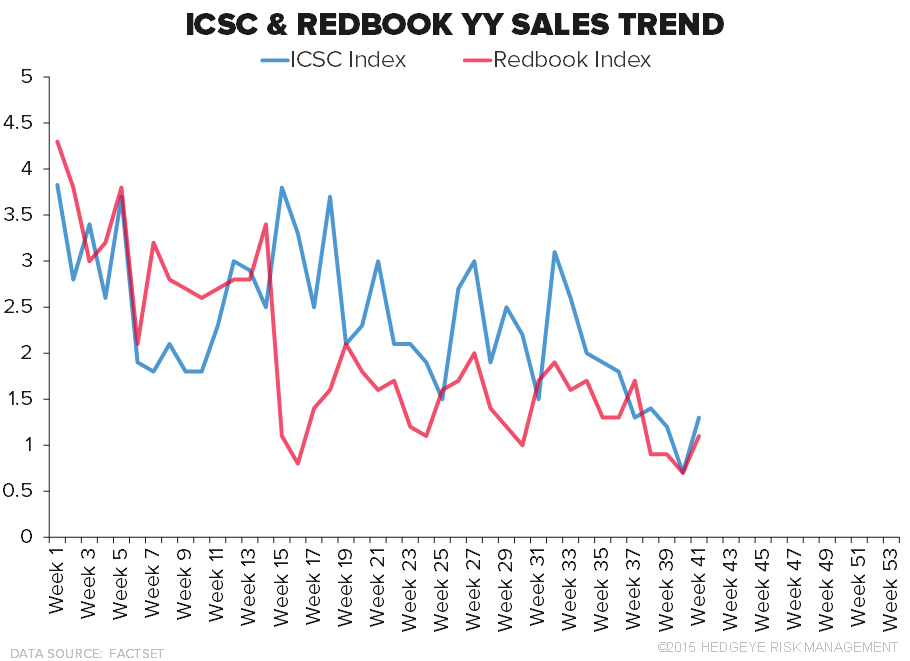

ICSC & Redbook - Small pop in the 1yr for ICSC and Redbook comp numbers and 2yr trend line (ICSC only), but on the 3yr which eliminates all noise -- 6th straight week of decelerating comp numbers.

KATE, KORS, COH, LVMH - LVMH seeing acceleration in business in Japan. Notable for KATE as it laps the sales tax lift from 2014. Japan underperformed company average by 1300bps and 700bps in 1Q and 2Q respectively.

(http://www.lvmh.com/news-documents/press-releases/q3-2015-revenue/)

NKE - Ndamukong Suh says he will be bringing a 'Nike store' to the home town of his alma mater Lincoln, Nebraska. Store planned to be ~18,000 SqFt in place of the old bookstore.

NKE, UA - Kemba Walker is leaving Under Armour to sign with Jordan. This is no surprise as his UA contract had expired, and since Walker plays for the team that Jordan owns.

(http://thesource.com/2015/10/11/kemba-walker-leaves-under-armour-for-jordan-brand/)

DLTR - Dollar Tree announced plan to rebrand 217 of 222 Deals stores as Dollar Tree stores and the other 5 as Family Dollar stores.

(http://www.dollartreeinfo.com/investors/global/releasedetail.cfm?ReleaseID=936211)

KSS - Kohl’s expanding same day delivery service in nine markets, partnering with Deliv.

(http://wwd.com/retail-news/direct-internet-catalogue/kohls-expands-same-day-delivery-10260273/)

DKS - Dicks' Sporting Goods set to open 6 stores this month.

(http://www.sportsonesource.com/news/article_home.asp?Prod=1§ion=9&id=57878)

Facebook Tests A Dedicated Shopping Feed

(http://techcrunch.com/2015/10/12/facebook-commerce-updates/#.2seo6e:gzv7)